A Unique Technology Company Wrapped in a Bank

“I assume our whole payment systems will be stablecoins in 10 or 15 years” – Stanley Druckenmiller

I) Introduction

The bank currently prepared to profit from Druckenmillers’ prophecy is currently either underappreciated or ignored.

But what if you could pair the growth potential of a highly scalable tech company with a heavily regulated moat, add in significant optionality in a nascent market, all while trading at 1x 2026 book value and 9x earnings? The founder-led VersaBank (VBNK) is just that, and in our view, one of the rarest setups we come across: a compounding business with second compounding emerging business attached, both available for roughly the liquidation price of the first.

We've been building our position at an average cost basis of roughly $14.97 per share for the U.S. equity (~C$20.70 for VBNK.TO), a price we believe is fair-to-cheap for a specialty lender with a virtually spotless 30-year credit record. And for effectively no incremental cost, we’ve been gifted access to U.S. market entry, where the core flywheel is spinning inside a structurally larger and higher-margin market, with attached optionality on Real Bank Tokenized Deposits, which we believe could be one of the more consequential emerging franchises in fintech this decade.

VersaBank sits squarely inside the framework that has defined our best work at Crossroads: long-duration transformation paired with emerging secular growth, where the market has mistaken a previous chapter for the whole book.

On the surface, VersaBank is priced as a niche Canadian B2B bank, gathering deposits and extending financing digitally through third-party intermediaries. We believe VersaBank will soon be understood for what it is: a high-moat financial-technology business leveraging its proprietary platform to create uniquely profitable outcomes for financial partners. With not one but two imminent growth drivers leading to a rapid inflection in earnings power, we see plausible scenarios where VersaBank equity appreciates 3x, 5x, or 10x over the next 2–3 years.

From its beginnings as a tiny trust company in 1993 with just C$20 million in assets, founder-CEO David Taylor transformed VersaBank into a branchless, technology-driven bank that now boasts over C$6 billion in assets and considerable market share in its Canadian niche. Most of its business comes from its Receivable Purchase Program (RPP), in which the company buys the cash flows of point-of-sale loans while its customer, the lender, keeps the loan on its balance sheet. Impressively, in the 30 years of operations, the bank has incurred virtually zero loan losses due to its unique funding model.

Although timing is never precise in this kind of work, the clock on VersaBank is less ambiguous than most. The U.S. transition is ending after a year of elevated one-time costs and the natural learning curve of entering a new market. The regulation-mandated sale of the non-core cybersecurity business should conclude within the next few months. The RBTD initiative is moving from pilots to production at exactly the moment the GENIUS/CLARITY Acts and the current OCC interpretive letters are clearing a runway for real-bank tokenized deposits. Each of these is the kind of friction that causes investors to ignore a name until the fog lifts, but each area of concern is resolving in the next several quarters. Given the nature of the true business, that fog will benefit investors willing to take a long–term orientation.

The first key catalyst occurred in the late summer of 2024, when VersaBank began its transformation into a U.S. entity with the acquisition of Stearns Bank Holdingford, securing a rare U.S. national bank charter. This move gave VersaBank a permanent platform to expand its unique model into the unpenetrated U.S. market, a market 30x larger than Canada. Not only is the U.S. opportunity vastly larger in scale, but funding costs are structurally lower, enabling VersaBank to capture higher margins than in Canada.

The marriage of larger TAM and higher margins sets up VersaBank's U.S. expansion as one of the most important growth vectors in the company's history, with the potential to multiply assets and earnings far beyond what the Canadian franchise could achieve.

As the U.S. business begins to demonstrate its high-growth potential, patient investors have the chance to enter a franchise that we believe can conservatively generate 5x returns over the next five years.

The core-business story is persuasive on its own but embedded within VersaBank is a far larger catalyst: a potential 50x-plus return opportunity in Real Bank Tokenized Deposits (RBTDs). VersaBank's RBTD initiative offers a tokenized bank deposit platform that could capture tens of billions in low-cost deposits even if the CLARITY Act does not pass and current OCC rules are implemented. The market hasn't recognized it, and for those who think they have, the true opportunity is orders of magnitude larger than they realize.

II) Investment Thesis

Our report will discuss the company in Canadian dollars as it currently reports as such, though has a NASDAQ listing where we have invested given the domicile transition that is to occur in a few months. At today’s price of ~C$20 per share, VersaBank trades around book value given expected earnings and proceeds from the sale of its cybersecurity business in the next few months. Clearly, the market is effectively assigning minimal credit to U.S. growth or RBTD optionality.

There are several reasons for this current mispricing:

- Liquidity constraints created a forced exclusion of mandate–driven investors: Ownership is unusually concentrated with three key players, including Taylor, holding over 40% of the float. With only C$500M+ in market cap and C$500K+ in average daily volume, institutions simply cannot build a position of meaningful size, if at all. Corporate structural change in April coupled with likely inclusion in the Russell 2000 index later this year, means that investors positioning ahead of these catalysts can capture the multiple expansion that follows as a broader investor base closes the illiquidity discount currently embedded in the stock.

- Investor base in limbo as VersaBank transitions into a U.S. entity: Caught between two worlds as Versa enters the U.S. market, U.S. investors offhandedly associate it with the Canadian bank cohort and its perceived structural inferiorities. Canadian investors, on the other hand, adopt the “elbows up” approach towards anything American. Investors with a longer time horizon can take advantage of this shift in ownership before the transformation is apparent at all.

- Reduced near–term earnings and ROE reaching their inflection points: VersaBank has spent the past two years preparing to operate at scale in the United States. The transition has temporarily reduced near-term earnings by over 20%, reflecting the one-time costs required under Federal Reserve oversight. We expect earnings growth to accelerate meaningfully in 2026, with the U.S. division surpassing the Canadian one within roughly a year or two.

- Sell side’s misplaced concern with delays in U.S. RPP rollout: The company’s U.S. RPP rollout has drawn skepticism from investors due to a slower-than-expected start, reinforcing the sell side’s perception that the CEO sometimes “overpromises.” The slow start was really a product of expectations on timing, not RPP viability, as adaption to U.S. processes required four to five months of detailed work to align credit boxes, cash flow mechanics, and servicing protocols. With those hurdles now behind them, asset growth is accelerating.

- Real Bank Tokenized Deposits’ true upside completely ignored or misunderstood: VersaBank’s Real Bank Tokenized Deposits (RBTDs) are the first true open-network bank-issued stablecoin alternative, making it deposit-insured, interest-bearing, and blockchain-native, backed by U.S. treasuries. If adopted, they could attract tens of billions in near-zero-cost deposits, fundamentally transforming VersaBank’s funding base.

- Sale of DRT Cyber division increases earnings, hones in on core business lines, and adds to margin of safety: The company is in the process of selling its DRT Cyber subsidiary in a mandated sale, expected to close within the next few months as per U.S. banking rules. Since DRTC was run profit neutral, the divestiture of VersaBank’s subsidiary DRT Cyber should improve earnings two-fold via “addition by subtraction” and provide more capital to deploy to core business lines.

We’d be remiss if we didn’t highlight the potential risks embedded in the company which include: execution missteps in the U.S. RPP growth (e.g., slower onboarding of new partners), regulatory delays of RBTDs due to the CLARITY Act legislative fight, and potential credibility concerns around the CEO’s ambitious targets. At the macro level, VersaBank remains moderately exposed to changes in interest rates, broader credit market stress affecting consumer spending, and PoS loan demand, as well as regulatory or policy shifts in either Canada or the U.S. that could alter the economics of specialty finance or digital banking.

In the following piece, we will break down both these core business lines and each catalyst in greater detail.

III) Business Analysis

VersaBank operates through two main segments (once DRTC is sold): its core Digital Banking operations, driven primarily by the RPP for point-of-sale financing, and its nascent Digital Meteor division, which offers Real Bank Tokenized Deposits (RBTDs), a form of tokenized bank deposits. Let’s analyze each segment’s customers, value proposition, and competitive landscape:

i) Digital Banking Division

VersaBank’s Digital Banking division is a federally regulated platform operating as an infrastructure provider to specialty lends and financial institutions. The division utilizes proprietary technology to monitor partner cash flows and credit performance, enabling efficient balance sheet deployment with minimal operating overhead. By leaning heavily on technology, the Digital Banking business has impressive operating leverage. At scale the business can generate a sub-25% efficiency ratio, compared to most U.S. banks’ efficiency ratios of 50–60%.

The company has a very sticky deposit base, with over 200 customers comprised of deposit brokers (80%) and licensed insolvency trustee firms (20%). All deposits are term deposits, removing the risk of capital flight. Additionally, depositors have no direct access to their deposits.

Receivable Purchase Program (RPP) – A Point-of-Sale Financing Engine

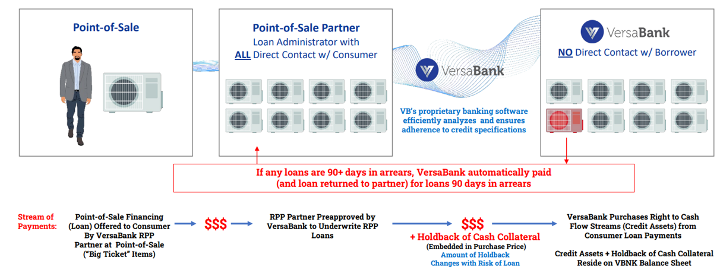

VersaBank’s RPP funding model creates a rare win–win–win ecosystem for consumers, finance partners, and, of course, VersaBank itself. Rather than competing directly for retail customers, VersaBank’s RPP provides funding to finance companies (partners) who extend point-of-sale (PoS) loans and leases to consumers for items like home HVAC systems, pools, appliances, etc. Importantly, VersaBank purchases the cash flow streams from these consumer loans at par (versus ~75% from conventional sources) by supplying the PoS partner with upfront capital. The PoS partner, the loan administrator, keeps the loans on its balance sheet, continues to service the loans, and maintains the customer relationship, while VersaBank earns the interest payments with minimal administrative overhead.

In exchange for providing immediate funding on a PoS loan, VersaBank structures the RPP so that if a borrower defaults, the PoS partner is required to immediately repay the remaining balance to VersaBank, thereby eliminating credit risk. Below is the company’s presentation of RPP.

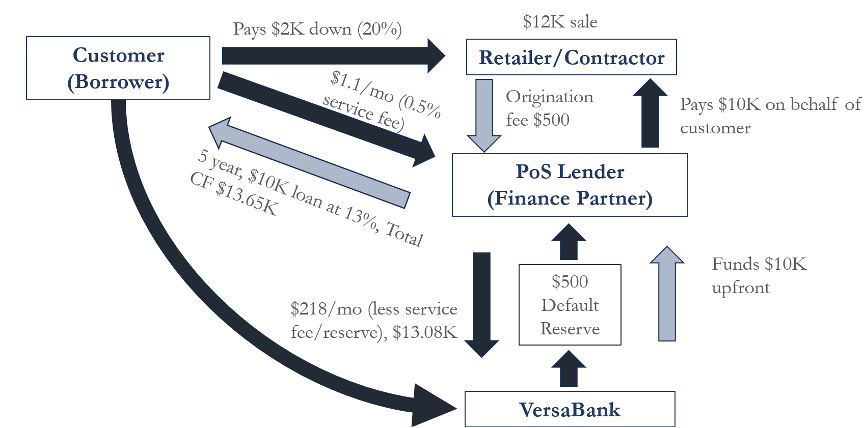

Consumers and retailers have access to easier sales processes and more affordable financing options. Consumers can finance “big ticket” purchases on installment plans (e.g. a $12K item financed 20% down at ~13% interest, paid in ~$227 monthly installments) at lower rates than credit cards offer, and with less paperwork than a HELOC. This process then gives the retailer an easier path to sales.

Finance partners are transformed into originators or servicers, with a greater ROE than they’d experience using internal capital. The retailer’s finance partner gets paid immediately (at par or better) for the loans it originated, thereby generating cash flow from origination and servicing the loan. The finance partner can massively amplify its ROE by originating more loans with the freed-up capital. Since the loan stays on the balance sheet, PoS partners’ increased scale gives them access to cheaper funding from other sources, as well as improved data advantages and commercial credibility.

VersaBank is then left with a high–yield loan portfolio with remarkably low credit risk. Importantly, since VersaBank is not customer-facing, it avoids the patchwork of state-level consumer finance regulations that typically slow down specialty finance firms, enabling faster and more scalable growth.

Default Risk: Transferring Loan Responsibility to PoS Partners

VersaBank’s unique RPP structure and its near–total avoidance of default risk are worth further explanation. PoS partners must post 5% cash reserves, ~2x historical default rates, and repurchase or cover any loans that reach 90+ days delinquent, ensuring VersaBank is made whole on the remaining balance. Additionally, VersaBank deliberately concentrates its exposure in large home improvement transactions where loans typically require 20%+ down payments and are often value-accretive for the consumer, with the home itself serving as implicit collateral.

By restricting relationships to established partners serving prime and super-prime borrowers, VersaBank has never recorded a material loan loss, even amidst economic downturns. The necessary environment to produce a loss for VersaBank, after successfully navigating the GFC and COVID, would have to be near apocalyptic. Should specialty lenders default en masse, the loans get put back and VersaBank avoids any loss to book value.

An Illustrative RPP Transaction and its Economics

Below is an illustrative example of an RPP loan for a $12K HVAC purchase, at 20% down on a 5-year term, with a 13% interest rate and a 5% origination fee that is paid by the retailer/contractor.

A customer purchases a product or service from a retailer or contractor, who in turn relies on a specialty finance firm to provide financing that supports the sale. VersaBank funds these specialty finance partners by advancing the full loan amount upfront, while requiring the partner to retain only ~5% of the loan’s value (recall this is >2x the lending verticals historical credit losses) on its balance sheet. In return, VersaBank receives the cash flows from the loan, net of servicing fees paid to the finance firm.

The sources and uses for the loan are detailed below.

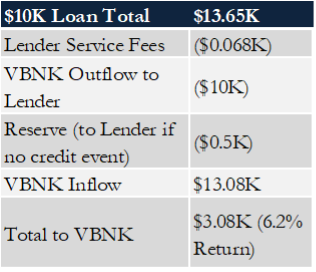

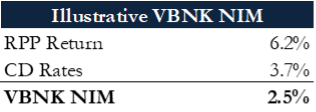

Interest rates on loans vary from 9% to 17% depending on the terms, but typically VersaBank targets a 6% return. For cost of funds, VersaBank only issues CDs or GICs to banks and security dealers, ranging from 1 year to 5 years (to match the duration of its RPP portfolio). Recent data shows GICs with 3.7% interest rates (1-3 years), equating to VersaBank’s NIM of 2.5%, consistent with guidance.

In the U.S, management expects to earn higher yields on RPP, which, when accompanied by lower U.S. CD rates, should enable expansion of its historical ~2.5% NIM.

Another avenue for VersaBank is securitization of these loans. Securitization yields a lower margin (~1% fee income), but it frees up capital and allows VersaBank to scale volume beyond its balance sheet. The bank reported adding its first RPP securitization partner in 2025, and plans to expand this channel.

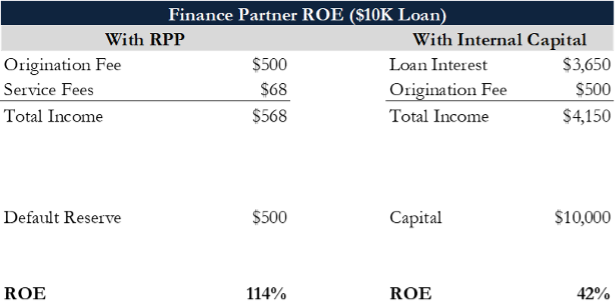

Partner Dynamics: VersaBank Improves ROE, Confers Data Advantages

Partnering with VersaBank’s RPP enables faster growth, stronger cash flow generation, and lower unit costs. Real-time, 100% advance funding positions partners as larger, more competitive players in OEM and retailer RFPs, which in turn compresses spreads across the rest of their capital stack (ABS, bank loans).

VersaBank leverages its proprietary cloud-based Asset Management System (AMS) to onboard partners and automate loan purchases, with minimal incremental operating cost. The platform, which includes API-based funding, real-time reconciliation, and loan-level analytics, enhances underwriting and collections, reducing losses and accelerating decision-making. The result is higher win rates, preservation of lender-of-record status, and more efficient recycling of first-loss equity, which in turn yield greater operating leverage and higher ROE for partners.

The remarkable economics VersaBank’s partners receive by way of ROE improvement are worth breaking down. Notably, the following is ex cost–of–funds for simplicity. With originated loans effectively carried only against a ~5% default reserve, the RPP structure frees significant capital for partners, allowing them to scale more rapidly and shift their economics from yield management toward capital-light origination and servicing.

Discussions with multiple partners indicate that VersaBank’s RPP is so accretive to ROE that it now accounts for nearly 50% of their funding mix.

Competitive Dynamics: Unique Product Protected by Focus and Low-Cost Ops

VersaBank’s RPP stands apart as a purpose-built funding alternative for point-of-sale lenders. Unlike traditional warehouse lines or securitizations, the program delivers real-time, 100% advance funding without competing for the end customer relationship. This creates a “banking-as-a-service” niche, where partners can scale origination rapidly, market themselves as larger counterparties in OEM and retailer RFPs, and tighten execution costs across the rest of their capital stack. Conversations with VersaBank partners highlight their strong focus and service-oriented approach, making them highly collaborative and noticeably more attentive than competitors.

An additional advantage stems from the company’s development of an AI module to ingest real-time loan data from partners, accelerating the time to assess and purchase a loan from days/weeks to minutes/hours. Traditional options such as bank credit lines, securitizations, or retained equity, are slower, more restrictive, or scale-dependent, leaving a gap that RPP squarely fills. With a 15-year operating history, proprietary API-based infrastructure, and loan-level analytics, VersaBank has engineered a system that improves underwriting discipline, accelerates collections, and materially enhances ROE for its partners.

Even if peers attempt to replicate the product with less efficient infrastructure, VersaBank’s digital-first operating model should ensure that its cost and speed advantages remain intact. It’s worth reiterating that RPP converts specialty finance firms from balance-sheet-intensive lenders into capital-light originators and servicers. In our view, it’s rare to find a business whose core product is as transformative and scalable as VersaBank’s RPP solutions. Should others enter the space, we would expect an industry-wide shift from ABS to RPP financing, rather than a displacement of VersaBank.

Market Trends: Larger Markets and Structurally Higher NIM

In Canada, VersaBank has 30 finance partners and holds an estimated 50% share of the Canadian PoS market (~C$65B market, ~10% financed). Home improvement financing makes up almost half of the Canadian PoS market. From industry conversations in Canada, the financing share of this market is expected to expand to 75% financed over time, growing to ~$C50 billion, ~20% per annum over the next ten years. In total, the financing market applicable to Canadian RPP should grow 15%-20% per annum.

The U.S. home improvement market is ~$400B and has no competing solution to RPP, as many U.S. firms use ABS or bank lending. VersaBank’s differentiated offering fits naturally between the two. A flagship example in the U.S. is Watercress Financial, a fast-growing originator of home improvement loans via a contractor network that became VersaBank’s inaugural U.S. RPP partner in 2025. VersaBank has added 4 more RPP customers this year and we believe it has a line of sight to 10 new logos this year.

The total U.S. PoS market is enormous, estimated to be almost $2 trillion. Another vertical in the U.S. utilizing a similar form of financing is the heavy equipment industry (farming, mining, construction), estimated at ~$500 billion.

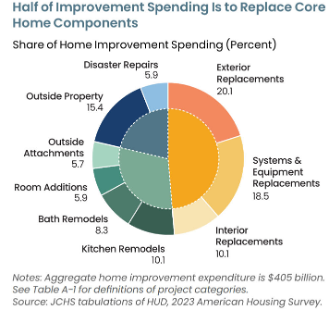

The U.S. housing market is defined by aging stock, with the average home nearly 44 years old. This drives ongoing demand for big-ticket replacements. Together these items represent roughly 50% of a $400 billion market, as shown below.

In the home improvement market, roughly 80% of purchases are funded with cash or home equity loans, ~5% with credit cards, and only ~2% through VersaBank’s specialty: contractor-arranged financing. Comparatively, mature markets for large-ticket items, such as autos, typically normalize at ~80% financed, suggesting home improvement financing is still in the early stages of penetration and has substantial room to grow.

Our discussions with large originators, such as GreenSky, point to this market expansion which has accelerated in the last few years as cost pressures on consumers increased in parallel with housing stock needs.

To reiterate, U.S. banking market has structurally higher NIMs than in Canada, by roughly 150 bps at ~3.5%. As VersaBank scales its U.S. operations, we expect its consolidated NIM to expand accordingly. Given the size of the market, its low financing penetration, and the lack of an existing RPP presence, VersaBank does not need dominant share to scale materially. Even a handful of strong partnerships can drive significant asset growth in this under-served segment, with returns exceeding those historically generated.

ii) Digital Meteor Division: Real Bank Tokenized Deposits (RBTDs) or “Stablecoin-as-a-Service”

VersaBank’s Digital Meteor division has developed a bank-issued stablecoin or tokenized deposit, branded as Real Bank Tokenized Deposits (RBTDs). The initial technology was developed in 2018, and the first pilot, titled VCAD, launched in Canada in 2021 before regulators blocked any potential use cases. Today, the company is piloting the USDV RBTD, which should be active in 2026 with regulatory tailwinds from the GENIUS Act's implementing rules and anticipated passage of the CLARITY Act. Additionally, Canada has become more receptive to the technology as its adoption gains momentum in the United States.

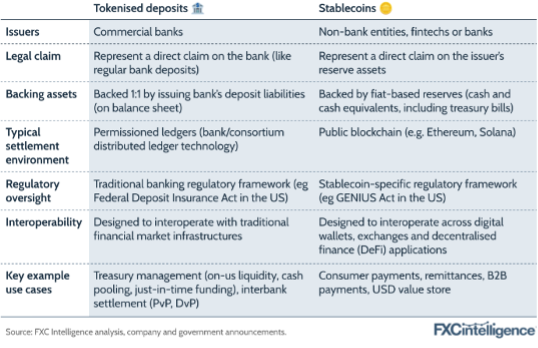

Each RBTD represents a one-for-one claim on cash held at the bank and is fully collateralized by actual deposits at VersaBank. Unlike conventional stablecoins such as USDC or Tether, RBTDs are like any other deposit — issued by a federally regulated institution, carrying deposit insurance, and are interest–bearing—advantages that crypto-native issuers cannot legally match.

In practice, RBTDs move across blockchain networks (currently Algorand, Ethereum, and Stellar), enabling 24/7 settlement and near-instant payments. At the customer level, VersaBank’s RBTD interface (VersaView) is designed to be familiar, a digital wallet that operates no differently than a standard bank account.

Issuance and redemption are managed through the bank’s proprietary VersaVault infrastructure and VersaView e-wallet, both SOC2-audited systems with layered encryption and compliance controls.

VersaBank has two options: 1) hold third-party stablecoins for thin NIMs, or 2) issue its own RBTDs and capture the full float, fee, and licensing economics. The first is an extension of existing services; the second is the order-of-magnitude opportunity which we will describe in further detail below.

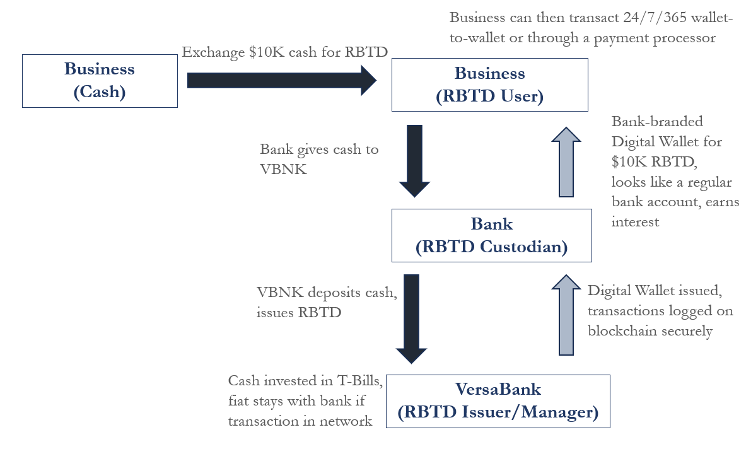

Illustrative RBTD Conversion Process

The process of converting fiat into RBTDs is quite simple. The key point is that all transaction capital in the RBTD system resides at VersaBank as low-cost funding. That capital stays parked so long as activity remains on-network, with VersaBank sharing issuance and servicing economics with partners, while customers gain 24/7 payments, lower transaction costs, and interest on their balances.

RBTD balances would sit on VersaBank books as ultra-low-cost deposits, which can be recycled into interest-earning assets. At the very least, fiat is placed into Treasuries for a risk-free spread. Management, however, has indicated possible regulatory clearance to allow channeling the cash into high-yield RPP loans. Either way, RBTDs function as a scalable, cheap, deposit base with considerable earnings potential at high margins.

Presented below are two possible NIMs for RBTDs assuming 1% interest rate (though most deposit accounts are ~0.1%), on $10 billion in total deposits.

With just $10B in RBTD deposits and no incremental costs, VersaBank could generate 5-10x of its current net income on just the float. Recent early RBTD clients, at 0.5% NIM, are not representative of future earnings potential, as the company tests monetization by offering initial partners a larger split of the earnings as an incentive. Either way, any margin would be plenty of upside.

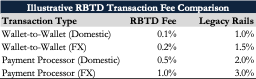

Should VersaBank sit at the center of a RBTD network as the issuer and settlement anchor, it can also generate considerable earnings by managing the capital flows in the system. Even with lower fees than competing payment rails, and sharing 50% of the fees with partners, these earnings amount to billions in transaction volume. A generalized RBTD fee schedule is detailed below.

If the illustrative $10 billionin transactions turns over about six times per year, the resulting fees couldresemble the figures in this table.

VersaBank’s fees alone in this conservative example could equal 2-3x VersaBank’s current net income.

While $10 billion sounds like a large number, the amount of capital in just CAD/USD FX is in the trillions, and we believe VersaBank has a line of sight to capture $100 billion in potential RBTDs.

Customer Dynamics: Ease of Digital Payments with the Benefits of a FDIC-Insured Bank

VersaBank is positioning RBTDs as a “deposit-as-a-service” solution for other institutions and fintechs, white-labeling its technology so that banks, payment providers, large retailers, and other fintech companies can easily launch their own branded digital tokens with the deposits at VersaBank.

Outside of the few largest banks, most institutions should see access to VersaBank’s RBTD platform as logically attractive. Using VersaBank’s platform allows them to bypass regulatory processes and any significant investment to build their own blockchain infrastructure, while defending deposits from fintechs and megabanks, monetizing transaction flow, and positioning themselves in digital finance.

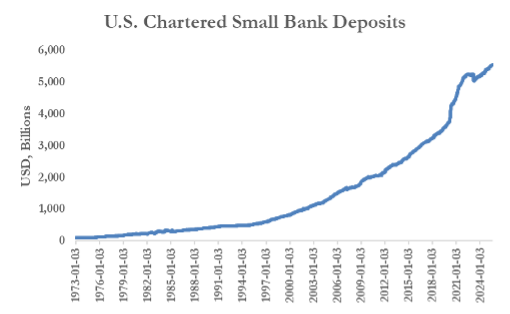

U.S. small banks hold nearly $6 trillion in deposits. Within that pool, corporate treasury and FX accounts, VersaBank’s initial RBTD target market, represent an estimated 5-10% of deposits, or $275-$550 billion. Capturing just 1–2% of that market would translate to $50-$100 billion.

When a U.S. bank’s customer purchases RBTD tokens (representing U.S. dollar deposits), the underlying funds are placed with VersaBank to back those tokens.

Partner banks don’t view this as a capital loss. RBTD-funded dollars might otherwise leave the bank entirely if customers moved funds to alternatives. The tradeoff for partner banks is as follows: forego marginal funding income in exchange for reduced regulatory burden and a competitive digital product, without materially altering the bank’s own balance sheet.

How does this benefit Versa, since its model of holding and managing partner RBTD reserves increases its own asset base, potentially diluting its regulatory ratios? Versa views this as a revenue opportunity to maximally monetize its existing balance sheet by capturing the full effect of fees and interest, with the potential to deploy that money into higher-yielding vehicles.

And let’s not forget about payment processors. Firms like Fiserv and Jack Henry could license VersaBank’s RBTD platform to embed a regulated, interest-bearing digital money layer directly into their core banking and payments infrastructure. While these firms already power account processing, ACH, wires, and card acquiring, they currently lack a compliant mechanism for tokenized real-time deposits that can move across blockchain rails. VersaBank’s infrastructure would let it offer bank-grade digital receipts (CADV/USDV) to thousands of mid-tier banks, enabling instant B2B payments, FX, and programmable treasury tools. This expands its platform defensibility and opens new revenue streams via transaction fees, API access, and yield-sharing on deposit float.

Competitive Dynamics: The Only Institutionally Ready Multi-Party Solution

The concept of tokenized bank deposits is new, but interest is growing in the financial industry. A few large banks have experimented internally (JPMorgan’s JPM Coin for institutional clients), and consortia have discussed interoperable deposit tokens.

However, VersaBank is one of the first to publicly pilot a retail/business-facing deposit token on public blockchains, and importantly, to offer it as a service to other firms. We believe numerous FX trading firms and North American corporations have already signaled their interest in VersaBank’s solution for FX and day-to-day treasury management.

Major stablecoin issuers like Circle (USDC) and Tether could be seen as indirect competitors, but if regulations require stablecoins to be bank-issued, those companies might instead become partners or clients (by partnering with banks for issuance). The GENIUS Act already prohibits stablecoin issuers from paying interest directly, and the OCC's February 2026 proposed rules go further by targeting third-party workarounds like the Circle-Coinbase arrangement. RBTDs, as bank deposits, face no such restriction, and therefore can legally pay interest under existing banking law.

A comparison of tokenized deposits versus stablecoins is shown below.

Along the lines of the comparison above, Visa and Stripe are piloting stablecoins largely aimed at consumer-facing use cases such as retail checkouts, gig economy payouts, and card-like settlement flows where ease of acceptance matters more than yield or balance sheet treatment. In contrast, tokenized deposits like RBTDs are built for institutional money movement: interbank transfers, corporate treasury, and cross-border FX where settlement risk, deposit insurance, and the ability to earn interest on idle balances matter. It may be that stablecoins dominate where commerce meets the consumer, while RBTDs are better suited to the plumbing of wholesale payments and liquidity management.

For now, VersaBank’s first-mover advantage and proprietary IP should give it a head start. Even if that head start translates into only a few percentage points of total market share, the sheer scale of trillions in capital flows could grow the RBTD business exponentially, leading to earnings potential up to 100x its current RPP franchise.

Market Trends: Huge Transaction Volume and Regulatory Tailwinds

The total addressable market for RBTDs is vast, especially when you consider opportunities outside of FX. Extension into interbank treasury liquidity ($500+ billion), institutional cash management ($100+ billion), merchant settlement rails ($10+ billion), and programmable payouts for embedded finance systems ($10+ billion) for Versa’s RBTDs should be considered live options. The stablecoin market itself provides a useful proxy: issuance has already more than doubled to ~$300 billion, and forecasts suggest it could reach $2 trillion by 2028 as tokenized cash becomes a backbone of payment infrastructure, and a possible demand source for U.S. treasuries.

The regulatory background includes two pieces of legislation which both benefit RBTD adoption. The GENIUS and Clarity Act, besides acting as a tailwind for VersaBank’s RBTD offering, indicate that the banking lobby has made sure that the playing field tilts its way. If the rules come out as expected (benefitting FDIC-insured issuers and restricting non-bank stablecoins), VersaBank will have a green light to commercialize RBTDs with far less uncertainty. That could spur rapid growth in deposits and trigger partnerships with fintechs or even bigger banks that prefer not to build their own tech.

Our conversations with regulators suggest there is little concern about the rapid growth of this type of deposit base, given that it is expected to be backed by Treasuries.

iii) DRT Cyber (~C$10M in Revenue, Regulatory Sale by mid-2026)

VersaBank also owns a small U.S.-based cybersecurity consulting subsidiary (DRT Cyber), which performs services like penetration testing for financial institutions and police departments. While a solid business with ~400 clients, it’s non-core. Under U.S. bank regulations, VersaBank is required to divest DRT Cyber by 2026, and as discussed earlier, the likely sale of this unit is a catalyst to simplify the story and return focus to the high-margin banking segments. DRT Cyber is expected to be sold for C$30-$50 million later this year.

iv) Management: “Outsider” Founder-CEO with Impressive 30-Year Track Record

VersaBank is led by David Taylor, a career banker and technologist who has built the institution from the ground up. In 1993, he acquired a small trust company with just C$20 million in assets and used proprietary software to transform it into one of the world’s first fully digital, branchless banks, today exceeding C$6 billion in assets.

Over three decades, his model has delivered virtually zero loan losses, even through multiple credit cycles, underscoring a disciplined approach to risk management. Taylor is known for being ahead of the regulatory curve—sometimes to the bank’s short-term detriment, but consistently validating his vision over time. Taylor retains a ~5% ownership stake, ensuring alignment with shareholders, and his reputation and credibility with regulators have greatly aided VersaBank’s ongoing transformation. Going forward, we believe he has effectively created a regulatory moat, positioning the bank to scale faster and with fewer compliance hurdles than peers.

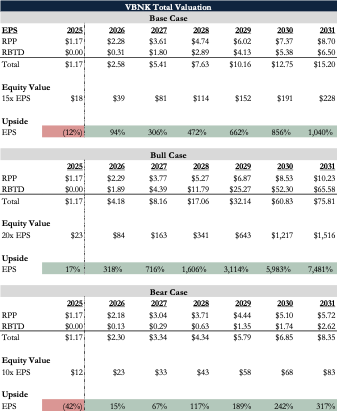

III) Valuation Analysis

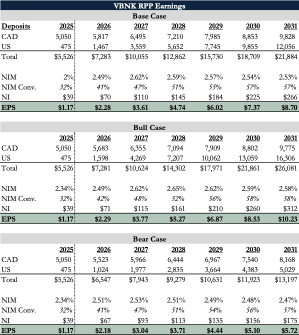

VersaBank is rapidly scaling its RPP product in the U.S. while continuing to grow strongly in Canada. We assume RPP assets expand into the tens of billions, maintaining historical economics, even though early signs suggest the U.S. rollout could prove more profitable.

To frame the opportunity, we present three scenarios in which RPP earning assets reach approximately C$13 billion, C$20 billion, and C$25 billion by 2031. In each case, we adjust net interest margins accordingly, while keeping NIM conversion fixed, as the model’s operating leverage should materialize with any level of asset growth. All figures are shown in Canadian dollars.

At a share price of C$20/share, our RPP scenario above implies an earnings yield ranging from 30% to 60%. With future growth, VersaBank trades at 2x to 3.5x P/E depending on the scenario. Through a cycle, considering the bank is highly unlikely to take credit losses and therefore incur book value impairments, we see the bull forecast as an “when, not if” scenario.

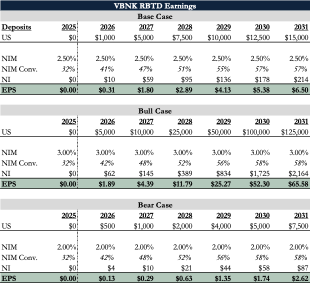

Turning to RBTDs, we model three scenarios where treasury-backed earning assets scale to C$7.5 billion, C$15 billion, and C$100+ billion by 2031. We assume a net interest margin of 2% to 3%, though the spread could be higher if RBTDs pay under 1% interest while treasuries yield around 4%.

With earnings yield scenarios ranging from a 15% increase to our bull scenario where EPS is three times the current share price, these projections remain surprisingly conservative on total amount, NIM, and NIM conversion.

As stated before, we believe that the existing customers in discussion with VersaBank already amount to $100 billion in possible RBTD assets set to come on stream in the next few years.

In the case of NIM, this analysis assumes that VersaBank cannot apply some of the capital deposited for RBTDs towards RPP. And with NIM conversion, while we apply VersaBank’s strong operating leverage from RPP to the RBTD analysis, most scaling costs for the RBTD business are already in the past. This means the assumed NIM conversion understates the true profitability since these assets convert nearly 99% of earnings directly to the bottom line, with taxes as the main expense (NIM conversion should be 75%).

Lastly, we don’t include potential earnings from transaction fees, as the upside here is already impressive, though we described them in the RBTD section above.

Bringing everything together, below is our combined valuation of RPP and RBTD for each of the scenarios.

The upside distribution here is uniquely asymmetric, and in the case of RBTD, mostly “free”. Even in the worst case, there’s a 15% gain in 2026 (with 2025 behind us, though shown for completeness). But if RBTD assets scale to $100+ billion in earning assets, the return generated explodes to an astonishing 75x by 2031. This rare risk-reward profile highlights the transformative potential in RBTDs.

Again, we haven’t included license fees that could come from the likes of Fiserv and others. The opportunity set presented above is plenty bullish for now.

IV) Why Now?

VersaBank has spent the last two years laying the groundwork for its U.S. expansion, and that heavy lifting is finally behind it. The upfront costs associated with the acquisition of a U.S. bank charter, and the one-time costs tied to regulatory approvals and operational systems are near completion. The sale of DRT Cyber should free up capital to fund new RPP assets. Against this backdrop, the business is poised to begin scaling RPP in the U.S. at structurally higher margins. And as we hope we’ve made clear, the Real Bank Tokenized Deposits (RBTD) business is primed for a zero-to-one inflection in the next 6-12 months, an option completely free to investors today.

V) Downside Protection

VersaBank is trading around book value and has unique downside protection as a bank that has reported nearly zero credit losses over 30 years. Its RPP contract structure forces partners to repurchase loans that go 90 days delinquent, shielding it from consumer credit risk. Additionally, the sale of DRT Cyber for C$1-$1.60 per share (~10%) further protects VBNK investors’ downside.

VI) Conclusion

Mispriced as a sleepy Canadian bank, VersaBank is a founder-led technology platform with proven credit discipline, downside protection, and a clear runway for asymmetric growth. With U.S. RPPs now scaling, one-time costs rolling off, and index inclusion likely, the stock offers investors a rare chance to buy a compounding bank franchise at around book value. Even with simple improvement in the base business, we believe VBNK can conservatively return 5x over the next five years, a 35%+ IRR per annum.

If RBTDs scale as our research suggests, VersaBank could evolve from a niche bank valued near book into a core infrastructure provider for the next generation of digital payments, commanding fintech-style multiples. Even a modest $10 billion in RBTD deposits could drive an almost 10x return, while $100 billion, already within line of sight from our exhaustive research, could imply over 50x upside.

Disclaimers

+ No guarantee of investment performance

Past performance of the financial instruments mentioned in this report should not be taken as an indication or guarantee of future results. The price, value of, and income from, any of the financial instruments mentioned in this report can rise as well as fall and may be affected by changes in economic, financial and political factors. Any projections, market outlooks or estimates in this presentation are forward looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect their returns or performance. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. Future returns are not guaranteed. If a financial instrument is denominated in a currency other than the investor's home currency, a change in exchange rates may adversely affect the price of, value of, or income derived from that financial instrument. In addition, investors in securities such as ADRs, whose values are affected by the currency of the underlying security, effectively assume currency risk.

+ No guarantee of accuracy

While the information prepared in this document is believed to be accurate, Crossroads Capital, LLC (the “Investment Manager”) makes no representation or warranty as to the completeness, accuracy or timeliness of such information. The Fund and the Investment Manager expressly disclaim all liability for errors or omissions in, or the misuse or misinterpretation of, any information contained herein.

+ No obligation to update or act on information

The Investment Manager has no obligation to update any information contained herein and may make investment decisions that are inconsistent with the views expressed herein. Any holdings of securities discussed herein are under periodic review and are subject to change at any time, without notice.

+ Not a recommendation to buy or sell any security

This report does not provide investment recommendations specific to individual investors. As such, the financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisions based upon their specific objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider this report as only a single factor in making an investment decision. All information provided is for informational purposes only and should not be deemed as investment or other professional advice or a recommendation to purchase or sell any specific security.

+ Not an offer to invest in our Fund

This report, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy limited partnership interests of Crossroads Capital Investment Partners, LP (the “Fund”) which may only be made at the time a qualified offeree receives a confidential private offering memorandum (“CPOM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the CPOM, the CPOM shall control. The interests shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution.

+ Other disclaimers

All trade names, trademarks, and service marks herein are the property of their respective owners, who retain all proprietary rights over their use. This document is confidential and may not be disseminated or reproduced without the prior written consent of the Investment Manager.