If you’d like to subscribe to Crossroads Capital Insights, please enter your email

Insights

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Special Commentary

Bloom Energy, Inc. (BE — NYSE) | Situational Awareness Collides with Physical Awareness—Exposing a Supply Wall and Hidden China Risks

July 9, 2026

We are short Bloom Energy (BE) and related derivatives. In the full report linked below we outline the reasons why we think the stock is not properly pricing in certain risks. We may at any time and for any reason exit or reverse those positions.

The AI build-out has been booming for nearly everything that touches a data center, and for much of it the enthusiasm is deserved: compute must be powered, cooled, and connected, and the firms selling those picks and shovels have watched their earnings prospects and valuations soar. But as adoption accelerates, undercapitalized sub-sectors—memory, substrates, physical power—are having trouble absorbing what amounts to a demand shock, and thus are attracting supernormal investor expectations and outsized share price moves. Solutions to alleviate these critical constraints that otherwise would never have seen the light of day are now not only being evaluated, but are being purchased at volumes that exceed their own capacity to deliver.

The investors swept up in this are best described as “Bottleneck Investors”: chasing constraints in the AI supply chain in the belief that there is multi-year visibility or an evolving moat in the new regime, with little understanding of the technology they are underwriting or the real limitations of what they are buying. While some bottlenecks may have an elongated upcycle and thus have further to go, a demand shock doesn’t typically lend itself to smooth sailing after it is alleviated.

There is one company whose bottleneck-induced upcycle is running straight into a supply wall, one that caps the revenue growth and earnings generation the market is pricing in, and when that becomes visible, the repricing should be severe.

Bloom Energy (BE) has been swept up as one of the bottleneck winners in the power sector. It makes on-site power that does not produce emissions thanks to its solid-oxide fuel cell (SOFC) technology, previously viewed as a science experiment. Now, given AI-driven demand and grid permitting bureaucracy, fuel cells look like an appealing solution despite sitting at the top end of the power-cost curve, with names like Oracle and Nebius booking gigawatts of capacity. The stock has run with additional fuel from retail following the “brand name” investors of this cycle who have what we call “Situational Awareness.” Click the button below to read our full 30-page writeup. SEE IMPORTANT DISCLAIMERS AT THE END OF THE REPORT.

As Crossroads hits a decade of searching for value in public markets, we thought it worthwhile to continue the conversation we began last summer when we discussed our understanding of value (linked here). In brief, our view is that value is dynamic, perhaps better described as organic, and is continuously developing inside the evolving complex markets that remain our hunting ground. In that earlier note, we focused on the directional orientation of valuation. There is backward-looking valuation, driven by metrics and Fama-French categories that characterize the stereotypical “value” investor, and then there is forward-looking valuation, in which businesses are evaluated relative to their normalized earnings power a few years out. Typically the latter is where the real money is made, because the gap between what a business looks like today and what it will look like at a normalized run rate is precisely where the market’s pricing machinery breaks down.

On that note, we’ve often placed our positions into one of two categories: emerging compounders and special situations. But ultimately, value is found in market mispricings, not in the categorical groupings themselves. Recall that the goal of fundamental investing is to pay a price for a stake in a business that is less than its true value in the expectation that price and value will converge, earning an excess return as the gap closes. For that reason, understanding why mispricings emerge and when they can be taken advantage of is the foundation of our ongoing search for value.

There are three general types of mispricings, and in each one human psychology does most of the heavy lifting. Below, we look at each type in turn.

The Three Types of Mispricing

Duration Mispricing

The first type is what we'll call duration mispricing. It’s created by the short-term incentive structures that govern institutional capital: Performance is measured in months, fees are paid against benchmarks reset annually, and careers are made and lost on the next print. The result is a profession whose participants cannot afford to be early even when they’re right. Blaise Pascal wrote in 1670 that “all of humanity's problems stem from man's inability to sit quietly in a room alone.” That line describes the modern institutional investor with uncomfortable precision: all portfolio managers’ miseries derive from their being unable to leave their best positions alone. The asset management profession is structurally designed to prevent exactly the behavior most likely to produce strong returns.

Warren Buffett described the flip side of Pascal’s idea at the 1998 Berkshire annual meeting: “We don't get paid for activity, just for being right. As to how long we’ll wait, we’ll wait indefinitely.” Clearly, Buffett had no problem sitting quietly and letting his investment theses play out. Indeed, Buffett noted in a 1999 BusinessWeek interview that investing success does not correlate with raw intelligence above a modest baseline; instead, it correlates to temperament, specifically the capacity to resist the urges that get other people into trouble.

Buffett’s distinction reframes the entire investing skill set. The binding constraint on returns is not analytical horsepower, but behavioral discipline under conditions that punish that very same discipline in the short run. The investors who blow up are very rarely the dumb ones. Instead, they’re often the bright ones who could not “sit quietly in a room alone” and felt compelled to “improve” a system that did not need improving. Long-Term Capital Management later that decade provide two well-documented case studies of exactly that pathology: extraordinary intellectual firepower, working machines that produced spectacular risk-adjusted returns on autopilot, and then a fatal urge to extract more by fiddling with the very mechanisms that were already working.

In the fight between waiting and wanting, wanting almost always prevails. Incentives form desires, and short-term reward structures hijack the nervous system, producing the stress, anxiety, and emotional irritability that drive bad decisions. Our perception of time also stretches when our wants are forced to wait, and in a culture engineered for instant gratification, the willingness to wait is continuously diminishing. Patience, in our experience, is less an absence of action than what one surgeon described as “staying focused on what matters, even when it takes time.” It can be incredibly difficult to follow the advice of the famous old quip, “Don't just do something—stand there!”

That is duration mispricing in one sentence. Pod shops and benchmark-tethered allocators cannot stand there, so they trade. We can stand there, so we upgrade while we wait. Our patience has been well rewarded since we started Crossroads in 2016, and we believe it will continue to be.

With that in mind, we have continued to see a duration mispricing play out with Nintendo, as pod shops, representing the bulk of institutional capital in the market today, have been unable to look through the perceived near-term headwinds surrounding rising memory input prices, despite it being negligible to both COGS and margins. We think the ongoing structural change in the memory complex is actually a tailwind to Nintendo’s business. We’ll leave the details for a standalone piece, but with Switch 2 competitors substantially more exposed and large quantities of inventory already on hand at Nintendo, these investors simply don’t have the luxury of time to wait for this incorrect view to reverse course. Given that we first invested in the company in 2018, we remain patiently waiting for the market to recognize Nintendo as an economic juggernaut that continues to upgrade its revenue base and increase its incremental margins. And even better, it gives us a high degree of optionality and downside protection while we wait.

Diagnosing a duration mispricing is the easy part. Exploiting one requires a deliberate operating architecture, because the same human wiring that leads other market participants to produce the mispricing also tempts us to accept it as legitimate. Buffett and Munger spent six decades engineering around this problem, and three habits from their record stand out. We’ve tried to implement versions of all three at Crossroads:

The first is timing the search to the cycle. Buffett did not run his idea-screening process continuously at the same intensity. He ran it cold during expensive markets and hot during cheap ones. He terminated his partnership in 1970 and made effectively no public-market investments until 1974, by which point the S&P 500 P/E had compressed from 20 to 7 and he was selling stocks bought recently at three times earnings to buy stocks selling at two times earnings. He repeated the pattern from 1984 to 1987: not a single new equity position added to the Berkshire portfolio across that stretch, sitting on a mountain of cash, doing nothing. Then in the second half of 1987 he deployed over a billion dollars (roughly 25% of Berkshire's book value) into a single non-controlled position in Coca-Cola. The biggest bets came out of the longest waits. The pairing is not coincidental. Waiting is what made the size of the eventual bet defensible.

The second is redirecting intellectual energy into channels where the activity cannot damage the main book. Buffett did not suppress his analytical hunger during the dry stretches. Instead, he transferred that focus and energy into a variety of separate but adjacent interests: Smaller special situations in his personal account that were too small to matter at Berkshire scale. Buying distressed corporate bonds when equities ran rich (over a billion dollars of Finova bonds at deep discounts in 2001). Dabbling in REITs, silver, or asset classes entirely outside the space in which impatience could hurt his partners. Combined with hobbies that absorb intellectual energy outside of markets entirely (bridge for Buffett, omnivorous cross-disciplinary reading for Munger), this architecture is one of deliberately constructed sandboxes for the restlessness that investors can’t will away. The right question is not how to be less curious, but rather where can curiosity be expressed without compromising the discipline that matters?

The third is building an adversarial second filter into the process. Buffett would screen an idea, get past his own evaluation, and then run it past Munger, whose job was specifically to find the flaw and shoot the idea down. Most ideas died there. The ones that survived both filters were, by construction, the no-brainers: what Buffett called “waiting for the phone to ring.” The architecture is adversarial on purpose. It’s much easier for two independent thinkers operating in sequence to kill a bad idea than for one thinker to talk himself out of an idea he’s already partway sold on. We’ve worked to build the same internal dynamic at Crossroads in a way that matches our scale, because the alternative (a single decision-maker increasingly persuaded by his own analysis) is the most expensive failure mode in this business. As PM, the buck stops with yours truly, but letting a devil’s advocate put up roadblocks to prevent mistakes is always a good way of preventing poor judgment in a business where judgment is everything.

Taken together, those three habits point to something beyond Pascal’s maxim: Sitting quietly in a room alone is not a passive state. It’s an actively maintained one, supported by deliberate structure. The investors who succeed at doing nothing for years at a time are not the ones with the least intellectual energy, but rather the ones who have engineered the most disciplined places for its use.

Framework Mispricing

The second type of mispricing is framework mispricing. Market participants are trained to process new information; they are not trained to question whether the framework through which they’re processing it is appropriate. The result is that genuinely new business architectures get evaluated against templates that don’t fit them, and the gap between what the business has become and what the market is willing to call it can persist for years.

While Nintendo fits this category in its own way, our investment in AST SpaceMobile very much remains a framework mispricing in our view: Investors continue to project an outdated and generic mental model onto the space sector, considering it to be an uninvestable wasteland. Layer on the SPAC element, the direct competition with Elon, and the fact that ASTS has been pre-revenue with active ATM programs for much of its public history, and you have ample ingredients for a setup where investors will take years to overcome their cognitive biases. Underneath that framework is a business and management team we believe will ultimately prove the company to be worth many multiples of where it is valued today. In other words, we see ample evidence that AST will emerge as a business of unquestionable quality, backed by numerous moats and a visionary management team, and that it remains grotesquely mispriced by any reasonable measure of its future earnings capacity. In short, the mispricing is due to the framework, not the facts.

Business Transformation Mispricing

A third form of mispricing comes from business transformations. These are situations in which value-unlocking change, driven by structural factors, is overlooked by the market. Markets are pricing engines built for continuity. They extrapolate what a business is worth today into what it will be worth tomorrow. Naturally, when a company transforms internally or its industry restructures around it, the financial data lag reality: earnings reflect the old model, analyst frameworks anchor to historical relationships, and the shareholder base was selected for a company that no longer exists. The bigger the change, the wider the gap—and the longer the gap persists, because the investors who own the stock are often the last ones to recognize what the company is becoming. Crossroads targets this window explicitly, whether the discontinuity originates inside the company or is imposed from outside, and uses the change itself as the resolution mechanism.

Our investment in FTAI aims to exploit that company’s ongoing business transformation: FTAI originally spun out from a conglomerate of industrial transportation assets before evolving into a pure-play aviation platform in 2022. Having started as a conventional jet engine lessor, it continues to advance its vertically integrated economic model with an overlooked pricing engine (bad pun intended), which allowed it to create a novel, nimble, and flexible approach to creating value in an industry predisposed to inertia. More recently, FTAI has begun to replace its invested capital with third-party partners, advancing the business into an asset-light, fee-bearing model. For its next act, FTAI plans to leverage its existing competitive advantages to convert end-of-life engines into 25MW turbines, a material opportunity not reflected in present financial performance. The structural change is real, and the financial disclosures have begun to reflect it—but the market is still processing the company through the template that fit it five years ago.

Why Mispricings Happen

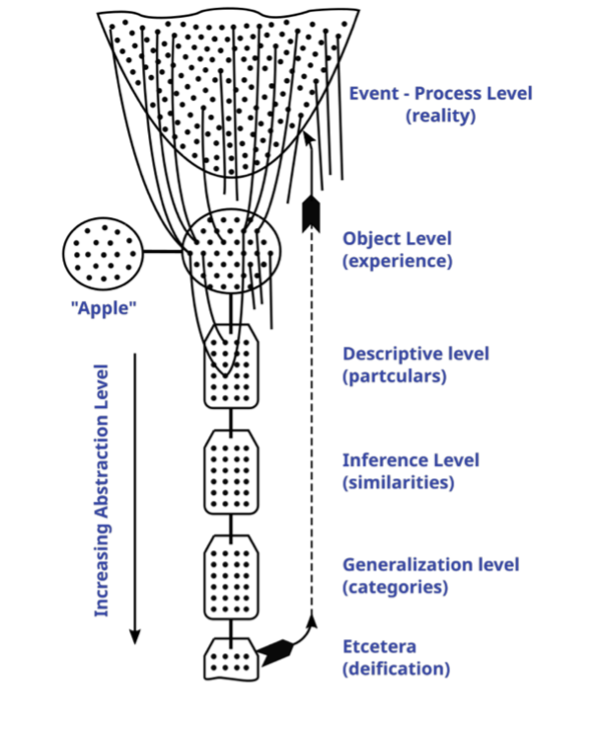

The phenomenon of persistent mispricings across public markets can be linked to the essential nature of the human brain and how we understand reality. We perceive reality through our senses, and we immediately attempt to categorize, name, and assign descriptors to it. The closer, more frequent, and more complete experience we have with an object, the more likely we are to comprehend it. Thomas Aquinas described this concept as the agreement of thought and thing, meaning we are right when the idea we have of something corresponds to the thing itself. A helpful visual for the way in which we come to know things comes from Alfred Korzybski, a philosopher in the realm of semantics. In 1925, he created a training device called the Structural Differential, a model and tool for understanding human knowledge:

As reality presents us with, say, an apple, we experience that reality through our senses and immediately abstract the experience to higher and higher levels of categories, applying tags or labels such as color, shape, form, species, flavor, and so on. Given this process of moving from the particular to the universal, the categories and values we assign to an object are more likely to be correct when we’ve had frequent complete views of, and encounters with, that object. Conversely the farther we are from an object, and the less exposure we have to it, the less likely we are to properly comprehend it. At its core (no apple pun intended), this is a concept everyone intuitively understands. When we tell two people, “Get to know each other”, we obviously don’t mean they should think about the other person, abstracting generalizations about each other from across the room. No, of course we mean they should spend time together, speak to each other, observe each other, and so forth. In short, knowledge is tied to experience.

This is all well and good, but what does it have to do with investing? The willingness to “get to know” a business determines the accuracy of our understanding of that business. Mispricings are really instances in which the market’s “thought” about a business does not match the “thing” itself, as investors attempt to categorize and understand something they have not taken the time to truly experience. A business undergoing a transformation, or whose thesis takes longer to play out than institutional capital is willing to wait, is like a speck on the desert horizon. That speck could be an oasis or a mirage. The heat haze obscures your vision. Ultimately, we don’t know what it is until we get close enough to see it clearly. But markets move fast. They see the speck of dust, and given incentive structures, timelines, and capacity for patience, categorize it. They’ve seen specks of dust like it before and apply that same thinking to this new spot on the horizon. By working to truly know the true nature of that spot on the horizon, by trudging along until we can get close enough to see it clearly, we are, on occasion, rewarded with an oasis—an investment opportunity that rewards our effort even though (or arguably precisely because) the market overlooked it.

Indeed, a willingness to pay close attention can yield surprisingly powerful results. Vincent Van Gogh was an almost obsessive observer of nature, spending much of his time outdoors. It might seem odd, then that his famous work "Starry Night" (shown below) is quite abstract. It doesn’t seem to be the work of someone who paid close attention to the details of the night sky.

In fact, critics initially deemed “Starry Night” too stylized, abstract, and unrealistic. However, it has since been commended by physicists and fluid dynamicists who found that it accurately depicts the mathematical theory of turbulence (the dynamism of energy through air in patterns that resemble eddies or waves) with near-perfect precision in at least fourteen different instances.

Coincidence? Perhaps. But Van Gogh’s willingness to stop and stare, to “get to know” his subject matter, may have helped him to create something almost miraculous. His painting may be quite abstract, but his abstractions are rooted in a deep, intimate understanding of his subject. "Starry Night” demonstrates the revelations that close attention to a subject matter can produce. At Crossroads, we take the time to immerse ourselves in the details of the companies we research, with the goal of being able to see things others can’t, like the swirls Van Gogh saw in an empty night sky.

To summarize, humans have a better chance of correctly understanding reality when they experience it directly and closely, instead of perceiving it through abstractions made at a distance. Fortunately for us, markets are constantly moving, with many investors glancing at events and announcements made by businesses and quickly assigning categories and values to them. These investors therefore often misunderstand or completely fail to recognize the true nature of these events. Mr. Market looks at reality from thirty thousand feet (or, if you prefer, a corner office on the fiftieth floor), so mispricings inevitably occur. Those who get as close as possible to the facts, and who can recognize patterns the abstracting machine has skipped over, are the ones best positioned to exploit value gaps before they close.

Our Edge

We believe our durable edge is thanks to the wealth of information we obtain through deep, close study of our companies and their industries. We try to get as close to events as possible, increasing the likelihood that we’ll understand the reality of the situation. As the spy novelist John le Carré said, “a desk is a dangerous place from which to view the world.”

That proximity is only half of our edge. The other half is the operating architecture described above, and the two halves are inseparable. Close study without behavioral discipline produces conviction at the wrong moments. Behavioral discipline without close study produces patience without a reason to act on it. The combination of deep, detailed work on a small number of businesses, and an operating structure that allows us to wait as long as the gap takes to close, is the edge we believe we possess.

In practice, that means three things. First, we calibrate the intensity of our search to the opportunity set rather than to the calendar. When public equities are richly priced and the obvious work has already been done by everyone else, we slow our equity position decision-making and broaden our aperture to adjacent corners of the capital structure and to special situations where size is not an advantage. We don’t feel the need to fill our portfolio for the sake of filling it, and our partners should not expect us to. Second, we route our analytical restlessness into channels that do not contaminate the core book. The personal-account special situations, the deep dives into industries we do not yet have positions in, the eclectic reading habits that run across disciplines are not hobbies but sandboxes we can play in while sitting still on the names that matter. Third, we have built an internal process in which ideas are stress-tested adversarially before they become positions. Once an analyst has invested time in a thesis, his natural tendency is to find reasons why it’s right. That’s why we construct an environment in which the reasons it might be wrong are surfaced by someone whose job in that conversation is specifically to look for them.

Of course, we still get things wrong. But with a willingness to go one step further than the herd, the patience to wait for a gap to close on a timeline dictated by the business itself (and not by the calendar), and an operating structure that converts intellectual energy into discipline rather than into trades, we believe we can continue to find great businesses at attractive prices. That is the work. That is what we are paid for.

“I assume our whole payment systems will be stablecoins in 10 or 15 years” – Stanley Druckenmiller

I) Introduction

The bank currently prepared to profit from Druckenmillers’ prophecy is currently either underappreciated or ignored.

But what if you could pair the growth potential of a highly scalable tech company with a heavily regulated moat, add in significant optionality in a nascent market, all while trading at 1x 2026 book value and 9x earnings? The founder-led VersaBank (VBNK) is just that, and in our view, one of the rarest setups we come across: a compounding business with second compounding emerging business attached, both available for roughly the liquidation price of the first.

We've been building our position at an average cost basis of roughly $14.97 per share for the U.S. equity (~C$20.70 for VBNK.TO), a price we believe is fair-to-cheap for a specialty lender with a virtually spotless 30-year credit record. And for effectively no incremental cost, we’ve been gifted access to U.S. market entry, where the core flywheel is spinning inside a structurally larger and higher-margin market, with attached optionality on Real Bank Tokenized Deposits, which we believe could be one of the more consequential emerging franchises in fintech this decade.

VersaBank sits squarely inside the framework that has defined our best work at Crossroads: long-duration transformation paired with emerging secular growth, where the market has mistaken a previous chapter for the whole book.

On the surface, VersaBank is priced as a niche Canadian B2B bank, gathering deposits and extending financing digitally through third-party intermediaries. We believe VersaBank will soon be understood for what it is: a high-moat financial-technology business leveraging its proprietary platform to create uniquely profitable outcomes for financial partners. With not one but two imminent growth drivers leading to a rapid inflection in earnings power, we see plausible scenarios where VersaBank equity appreciates 3x, 5x, or 10x over the next 2–3 years.

From its beginnings as a tiny trust company in 1993 with just C$20 million in assets, founder-CEO David Taylor transformed VersaBank into a branchless, technology-driven bank that now boasts over C$6 billion in assets and considerable market share in its Canadian niche. Most of its business comes from its Receivable Purchase Program (RPP), in which the company buys the cash flows of point-of-sale loans while its customer, the lender, keeps the loan on its balance sheet. Impressively, in the 30 years of operations, the bank has incurred virtually zero loan losses due to its unique funding model.

Although timing is never precise in this kind of work, the clock on VersaBank is less ambiguous than most. The U.S. transition is ending after a year of elevated one-time costs and the natural learning curve of entering a new market. The regulation-mandated sale of the non-core cybersecurity business should conclude within the next few months. The RBTD initiative is moving from pilots to production at exactly the moment the GENIUS/CLARITY Acts and the current OCC interpretive letters are clearing a runway for real-bank tokenized deposits. Each of these is the kind of friction that causes investors to ignore a name until the fog lifts, but each area of concern is resolving in the next several quarters. Given the nature of the true business, that fog will benefit investors willing to take a long–term orientation.

The first key catalyst occurred in the late summer of 2024, when VersaBank began its transformation into a U.S. entity with the acquisition of Stearns Bank Holdingford, securing a rare U.S. national bank charter. This move gave VersaBank a permanent platform to expand its unique model into the unpenetrated U.S. market, a market 30x larger than Canada. Not only is the U.S. opportunity vastly larger in scale, but funding costs are structurally lower, enabling VersaBank to capture higher margins than in Canada.

The marriage of larger TAM and higher margins sets up VersaBank's U.S. expansion as one of the most important growth vectors in the company's history, with the potential to multiply assets and earnings far beyond what the Canadian franchise could achieve.

As the U.S. business begins to demonstrate its high-growth potential, patient investors have the chance to enter a franchise that we believe can conservatively generate 5x returns over the next five years.

The core-business story is persuasive on its own but embedded within VersaBank is a far larger catalyst: a potential 50x-plus return opportunity in Real Bank Tokenized Deposits (RBTDs). VersaBank's RBTD initiative offers a tokenized bank deposit platform that could capture tens of billions in low-cost deposits even if the CLARITY Act does not pass and current OCC rules are implemented. The market hasn't recognized it, and for those who think they have, the true opportunity is orders of magnitude larger than they realize.

II) Investment Thesis

Our report will discuss the company in Canadian dollars as it currently reports as such, though has a NASDAQ listing where we have invested given the domicile transition that is to occur in a few months. At today’s price of ~C$20 per share, VersaBank trades around book value given expected earnings and proceeds from the sale of its cybersecurity business in the next few months. Clearly, the market is effectively assigning minimal credit to U.S. growth or RBTD optionality.

There are several reasons for this current mispricing:

Liquidity constraints created a forced exclusion of mandate–driven investors: Ownership is unusually concentrated with three key players, including Taylor, holding over 40% of the float. With only C$500M+ in market cap and C$500K+ in average daily volume, institutions simply cannot build a position of meaningful size, if at all. Corporate structural change in April coupled with likely inclusion in the Russell 2000 index later this year, means that investors positioning ahead of these catalysts can capture the multiple expansion that follows as a broader investor base closes the illiquidity discount currently embedded in the stock.

Investor base in limbo as VersaBank transitions into a U.S. entity: Caught between two worlds as Versa enters the U.S. market, U.S. investors offhandedly associate it with the Canadian bank cohort and its perceived structural inferiorities. Canadian investors, on the other hand, adopt the “elbows up” approach towards anything American. Investors with a longer time horizon can take advantage of this shift in ownership before the transformation is apparent at all.

Reduced near–term earnings and ROE reaching their inflection points: VersaBank has spent the past two years preparing to operate at scale in the United States. The transition has temporarily reduced near-term earnings by over 20%, reflecting the one-time costs required under Federal Reserve oversight. We expect earnings growth to accelerate meaningfully in 2026, with the U.S. division surpassing the Canadian one within roughly a year or two.

Sell side’s misplaced concern with delays in U.S. RPP rollout: The company’s U.S. RPP rollout has drawn skepticism from investors due to a slower-than-expected start, reinforcing the sell side’s perception that the CEO sometimes “overpromises.” The slow start was really a product of expectations on timing, not RPP viability, as adaption to U.S. processes required four to five months of detailed work to align credit boxes, cash flow mechanics, and servicing protocols. With those hurdles now behind them, asset growth is accelerating.

Real Bank Tokenized Deposits’ true upside completely ignored or misunderstood: VersaBank’s Real Bank Tokenized Deposits (RBTDs) are the first true open-network bank-issued stablecoin alternative, making it deposit-insured, interest-bearing, and blockchain-native, backed by U.S. treasuries. If adopted, they could attract tens of billions in near-zero-cost deposits, fundamentally transforming VersaBank’s funding base.

Sale of DRT Cyber division increases earnings, hones in on core business lines, and adds to margin of safety: The company is in the process of selling its DRT Cyber subsidiary in a mandated sale, expected to close within the next few months as per U.S. banking rules. Since DRTC was run profit neutral, the divestiture of VersaBank’s subsidiary DRT Cyber should improve earnings two-fold via “addition by subtraction” and provide more capital to deploy to core business lines.

We’d be remiss if we didn’t highlight the potential risks embedded in the company which include: execution missteps in the U.S. RPP growth (e.g., slower onboarding of new partners), regulatory delays of RBTDs due to the CLARITY Act legislative fight, and potential credibility concerns around the CEO’s ambitious targets. At the macro level, VersaBank remains moderately exposed to changes in interest rates, broader credit market stress affecting consumer spending, and PoS loan demand, as well as regulatory or policy shifts in either Canada or the U.S. that could alter the economics of specialty finance or digital banking.

In the following piece, we will break down both these core business lines and each catalyst in greater detail.

III) Business Analysis

VersaBank operates through two main segments (once DRTC is sold): its core Digital Banking operations, driven primarily by the RPP for point-of-sale financing, and its nascent Digital Meteor division, which offers Real Bank Tokenized Deposits (RBTDs), a form of tokenized bank deposits. Let’s analyze each segment’s customers, value proposition, and competitive landscape:

i) Digital Banking Division

VersaBank’s Digital Banking division is a federally regulated platform operating as an infrastructure provider to specialty lends and financial institutions. The division utilizes proprietary technology to monitor partner cash flows and credit performance, enabling efficient balance sheet deployment with minimal operating overhead. By leaning heavily on technology, the Digital Banking business has impressive operating leverage. At scale the business can generate a sub-25% efficiency ratio, compared to most U.S. banks’ efficiency ratios of 50–60%.

The company has a very sticky deposit base, with over 200 customers comprised of deposit brokers (80%) and licensed insolvency trustee firms (20%). All deposits are term deposits, removing the risk of capital flight. Additionally, depositors have no direct access to their deposits.

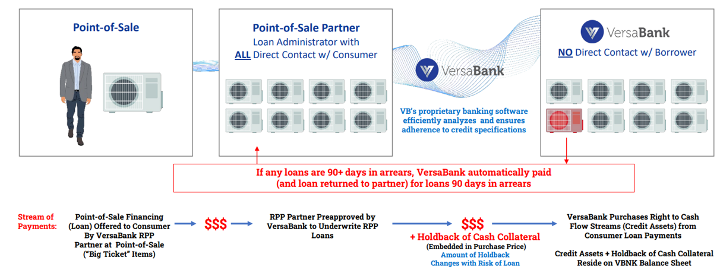

Receivable Purchase Program (RPP) – A Point-of-Sale Financing Engine

VersaBank’s RPP funding model creates a rare win–win–win ecosystem for consumers, finance partners, and, of course, VersaBank itself. Rather than competing directly for retail customers, VersaBank’s RPP provides funding to finance companies (partners) who extend point-of-sale (PoS) loans and leases to consumers for items like home HVAC systems, pools, appliances, etc. Importantly, VersaBank purchases the cash flow streams from these consumer loans at par (versus ~75% from conventional sources) by supplying the PoS partner with upfront capital. The PoS partner, the loan administrator, keeps the loans on its balance sheet, continues to service the loans, and maintains the customer relationship, while VersaBank earns the interest payments with minimal administrative overhead.

In exchange for providing immediate funding on a PoS loan, VersaBank structures the RPP so that if a borrower defaults, the PoS partner is required to immediately repay the remaining balance to VersaBank, thereby eliminating credit risk. Below is the company’s presentation of RPP.

Consumers and retailers have access to easier sales processes and more affordable financing options. Consumers can finance “big ticket” purchases on installment plans (e.g. a $12K item financed 20% down at ~13% interest, paid in ~$227 monthly installments) at lower rates than credit cards offer, and with less paperwork than a HELOC. This process then gives the retailer an easier path to sales.

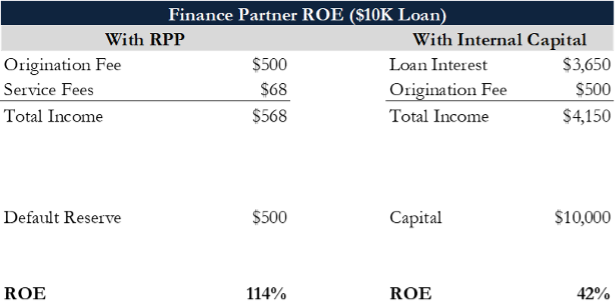

Finance partners are transformed into originators or servicers, with a greater ROE than they’d experience using internal capital. The retailer’s finance partner gets paid immediately (at par or better) for the loans it originated, thereby generating cash flow from origination and servicing the loan. The finance partner can massively amplify its ROE by originating more loans with the freed-up capital. Since the loan stays on the balance sheet, PoS partners’ increased scale gives them access to cheaper funding from other sources, as well as improved data advantages and commercial credibility.

VersaBank is then left with a high–yield loan portfolio with remarkably low credit risk. Importantly, since VersaBank is not customer-facing, it avoids the patchwork of state-level consumer finance regulations that typically slow down specialty finance firms, enabling faster and more scalable growth.

Default Risk: Transferring Loan Responsibility to PoS Partners

VersaBank’s unique RPP structure and its near–total avoidance of default risk are worth further explanation. PoS partners must post 5% cash reserves, ~2x historical default rates, and repurchase or cover any loans that reach 90+ days delinquent, ensuring VersaBank is made whole on the remaining balance. Additionally, VersaBank deliberately concentrates its exposure in large home improvement transactions where loans typically require 20%+ down payments and are often value-accretive for the consumer, with the home itself serving as implicit collateral.

By restricting relationships to established partners serving prime and super-prime borrowers, VersaBank has never recorded a material loan loss, even amidst economic downturns. The necessary environment to produce a loss for VersaBank, after successfully navigating the GFC and COVID, would have to be near apocalyptic. Should specialty lenders default en masse, the loans get put back and VersaBank avoids any loss to book value.

An Illustrative RPP Transaction and its Economics

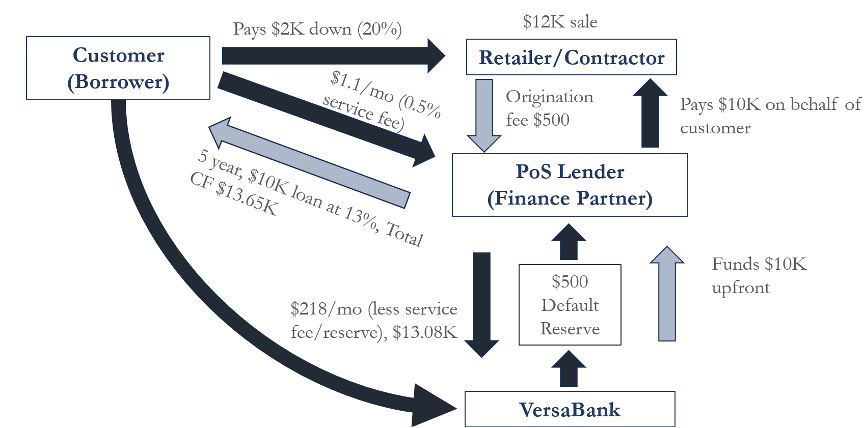

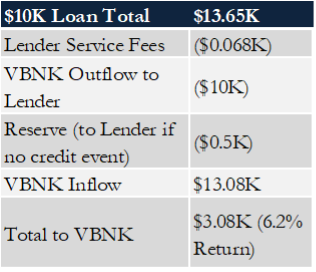

Below is an illustrative example of an RPP loan for a $12K HVAC purchase, at 20% down on a 5-year term, with a 13% interest rate and a 5% origination fee that is paid by the retailer/contractor.

A customer purchases a product or service from a retailer or contractor, who in turn relies on a specialty finance firm to provide financing that supports the sale. VersaBank funds these specialty finance partners by advancing the full loan amount upfront, while requiring the partner to retain only ~5% of the loan’s value (recall this is >2x the lending verticals historical credit losses) on its balance sheet. In return, VersaBank receives the cash flows from the loan, net of servicing fees paid to the finance firm.

The sources and uses for the loan are detailed below.

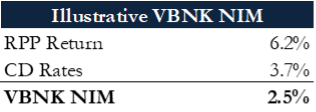

Interest rates on loans vary from 9% to 17% depending on the terms, but typically VersaBank targets a 6% return. For cost of funds, VersaBank only issues CDs or GICs to banks and security dealers, ranging from 1 year to 5 years (to match the duration of its RPP portfolio). Recent data shows GICs with 3.7% interest rates (1-3 years), equating to VersaBank’s NIM of 2.5%, consistent with guidance.

In the U.S, management expects to earn higher yields on RPP, which, when accompanied by lower U.S. CD rates, should enable expansion of its historical ~2.5% NIM.

Another avenue for VersaBank is securitization of these loans. Securitization yields a lower margin (~1% fee income), but it frees up capital and allows VersaBank to scale volume beyond its balance sheet. The bank reported adding its first RPP securitization partner in 2025, and plans to expand this channel.

Partner Dynamics: VersaBank Improves ROE, Confers Data Advantages

Partnering with VersaBank’s RPP enables faster growth, stronger cash flow generation, and lower unit costs. Real-time, 100% advance funding positions partners as larger, more competitive players in OEM and retailer RFPs, which in turn compresses spreads across the rest of their capital stack (ABS, bank loans).

VersaBank leverages its proprietary cloud-based Asset Management System (AMS) to onboard partners and automate loan purchases, with minimal incremental operating cost. The platform, which includes API-based funding, real-time reconciliation, and loan-level analytics, enhances underwriting and collections, reducing losses and accelerating decision-making. The result is higher win rates, preservation of lender-of-record status, and more efficient recycling of first-loss equity, which in turn yield greater operating leverage and higher ROE for partners.

The remarkable economics VersaBank’s partners receive by way of ROE improvement are worth breaking down. Notably, the following is ex cost–of–funds for simplicity. With originated loans effectively carried only against a ~5% default reserve, the RPP structure frees significant capital for partners, allowing them to scale more rapidly and shift their economics from yield management toward capital-light origination and servicing.

Discussions with multiple partners indicate that VersaBank’s RPP is so accretive to ROE that it now accounts for nearly 50% of their funding mix.

Competitive Dynamics: Unique Product Protected by Focus and Low-Cost Ops

VersaBank’s RPP stands apart as a purpose-built funding alternative for point-of-sale lenders. Unlike traditional warehouse lines or securitizations, the program delivers real-time, 100% advance funding without competing for the end customer relationship. This creates a “banking-as-a-service” niche, where partners can scale origination rapidly, market themselves as larger counterparties in OEM and retailer RFPs, and tighten execution costs across the rest of their capital stack. Conversations with VersaBank partners highlight their strong focus and service-oriented approach, making them highly collaborative and noticeably more attentive than competitors.

An additional advantage stems from the company’s development of an AI module to ingest real-time loan data from partners, accelerating the time to assess and purchase a loan from days/weeks to minutes/hours. Traditional options such as bank credit lines, securitizations, or retained equity, are slower, more restrictive, or scale-dependent, leaving a gap that RPP squarely fills. With a 15-year operating history, proprietary API-based infrastructure, and loan-level analytics, VersaBank has engineered a system that improves underwriting discipline, accelerates collections, and materially enhances ROE for its partners.

Even if peers attempt to replicate the product with less efficient infrastructure, VersaBank’s digital-first operating model should ensure that its cost and speed advantages remain intact. It’s worth reiterating that RPP converts specialty finance firms from balance-sheet-intensive lenders into capital-light originators and servicers. In our view, it’s rare to find a business whose core product is as transformative and scalable as VersaBank’s RPP solutions. Should others enter the space, we would expect an industry-wide shift from ABS to RPP financing, rather than a displacement of VersaBank.

Market Trends: Larger Markets and Structurally Higher NIM

In Canada, VersaBank has 30 finance partners and holds an estimated 50% share of the Canadian PoS market (~C$65B market, ~10% financed). Home improvement financing makes up almost half of the Canadian PoS market. From industry conversations in Canada, the financing share of this market is expected to expand to 75% financed over time, growing to ~$C50 billion, ~20% per annum over the next ten years. In total, the financing market applicable to Canadian RPP should grow 15%-20% per annum.

The U.S. home improvement market is ~$400B and has no competing solution to RPP, as many U.S. firms use ABS or bank lending. VersaBank’s differentiated offering fits naturally between the two. A flagship example in the U.S. is Watercress Financial, a fast-growing originator of home improvement loans via a contractor network that became VersaBank’s inaugural U.S. RPP partner in 2025. VersaBank has added 4 more RPP customers this year and we believe it has a line of sight to 10 new logos this year.

The total U.S. PoS market is enormous, estimated to be almost $2 trillion. Another vertical in the U.S. utilizing a similar form of financing is the heavy equipment industry (farming, mining, construction), estimated at ~$500 billion.

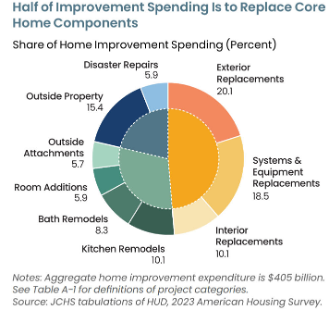

The U.S. housing market is defined by aging stock, with the average home nearly 44 years old. This drives ongoing demand for big-ticket replacements. Together these items represent roughly 50% of a $400 billion market, as shown below.

Source: Harvard Housing Study 2023.

In the home improvement market, roughly 80% of purchases are funded with cash or home equity loans, ~5% with credit cards, and only ~2% through VersaBank’s specialty: contractor-arranged financing. Comparatively, mature markets for large-ticket items, such as autos, typically normalize at ~80% financed, suggesting home improvement financing is still in the early stages of penetration and has substantial room to grow.

Our discussions with large originators, such as GreenSky, point to this market expansion which has accelerated in the last few years as cost pressures on consumers increased in parallel with housing stock needs.

To reiterate, U.S. banking market has structurally higher NIMs than in Canada, by roughly 150 bps at ~3.5%. As VersaBank scales its U.S. operations, we expect its consolidated NIM to expand accordingly. Given the size of the market, its low financing penetration, and the lack of an existing RPP presence, VersaBank does not need dominant share to scale materially. Even a handful of strong partnerships can drive significant asset growth in this under-served segment, with returns exceeding those historically generated.

ii) Digital Meteor Division: Real Bank Tokenized Deposits (RBTDs) or “Stablecoin-as-a-Service”

VersaBank’s Digital Meteor division has developed a bank-issued stablecoin or tokenized deposit, branded as Real Bank Tokenized Deposits (RBTDs). The initial technology was developed in 2018, and the first pilot, titled VCAD, launched in Canada in 2021 before regulators blocked any potential use cases. Today, the company is piloting the USDV RBTD, which should be active in 2026 with regulatory tailwinds from the GENIUS Act's implementing rules and anticipated passage of the CLARITY Act. Additionally, Canada has become more receptive to the technology as its adoption gains momentum in the United States.

Each RBTD represents a one-for-one claim on cash held at the bank and is fully collateralized by actual deposits at VersaBank. Unlike conventional stablecoins such as USDC or Tether, RBTDs are like any other deposit — issued by a federally regulated institution, carrying deposit insurance, and are interest–bearing—advantages that crypto-native issuers cannot legally match.

In practice, RBTDs move across blockchain networks (currently Algorand, Ethereum, and Stellar), enabling 24/7 settlement and near-instant payments. At the customer level, VersaBank’s RBTD interface (VersaView) is designed to be familiar, a digital wallet that operates no differently than a standard bank account.

Issuance and redemption are managed through the bank’s proprietary VersaVault infrastructure and VersaView e-wallet, both SOC2-audited systems with layered encryption and compliance controls.

VersaBank has two options: 1) hold third-party stablecoins for thin NIMs, or 2) issue its own RBTDs and capture the full float, fee, and licensing economics. The first is an extension of existing services; the second is the order-of-magnitude opportunity which we will describe in further detail below.

Illustrative RBTD Conversion Process

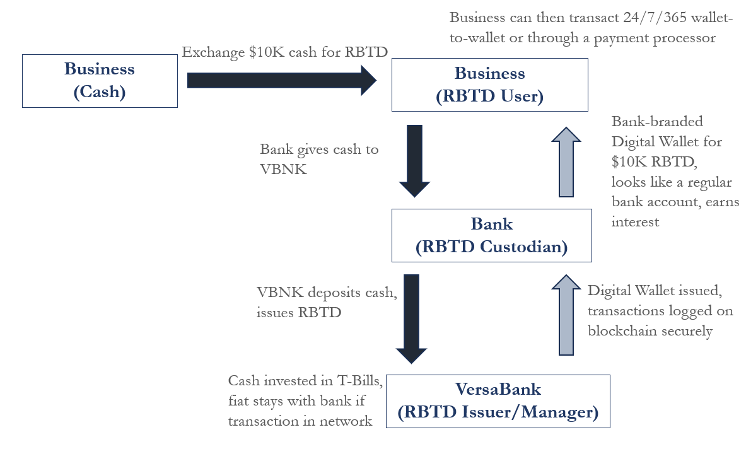

The process of converting fiat into RBTDs is quite simple. The key point is that all transaction capital in the RBTD system resides at VersaBank as low-cost funding. That capital stays parked so long as activity remains on-network, with VersaBank sharing issuance and servicing economics with partners, while customers gain 24/7 payments, lower transaction costs, and interest on their balances.

RBTD balances would sit on VersaBank books as ultra-low-cost deposits, which can be recycled into interest-earning assets. At the very least, fiat is placed into Treasuries for a risk-free spread. Management, however, has indicated possible regulatory clearance to allow channeling the cash into high-yield RPP loans. Either way, RBTDs function as a scalable, cheap, deposit base with considerable earnings potential at high margins.

Presented below are two possible NIMs for RBTDs assuming 1% interest rate (though most deposit accounts are ~0.1%), on $10 billion in total deposits.

With just $10B in RBTD deposits and no incremental costs, VersaBank could generate 5-10x of its current net income on just the float. Recent early RBTD clients, at 0.5% NIM, are not representative of future earnings potential, as the company tests monetization by offering initial partners a larger split of the earnings as an incentive. Either way, any margin would be plenty of upside.

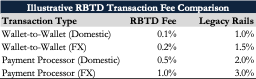

Should VersaBank sit at the center of a RBTD network as the issuer and settlement anchor, it can also generate considerable earnings by managing the capital flows in the system. Even with lower fees than competing payment rails, and sharing 50% of the fees with partners, these earnings amount to billions in transaction volume. A generalized RBTD fee schedule is detailed below.

If the illustrative $10 billionin transactions turns over about six times per year, the resulting fees couldresemble the figures in this table.

VersaBank’s fees alone in this conservative example could equal 2-3x VersaBank’s current net income.

While $10 billion sounds like a large number, the amount of capital in just CAD/USD FX is in the trillions, and we believe VersaBank has a line of sight to capture $100 billion in potential RBTDs.

Customer Dynamics: Ease of Digital Payments with the Benefits of a FDIC-Insured Bank

VersaBank is positioning RBTDs as a “deposit-as-a-service” solution for other institutions and fintechs, white-labeling its technology so that banks, payment providers, large retailers, and other fintech companies can easily launch their own branded digital tokens with the deposits at VersaBank.

Outside of the few largest banks, most institutions should see access to VersaBank’s RBTD platform as logically attractive. Using VersaBank’s platform allows them to bypass regulatory processes and any significant investment to build their own blockchain infrastructure, while defending deposits from fintechs and megabanks, monetizing transaction flow, and positioning themselves in digital finance.

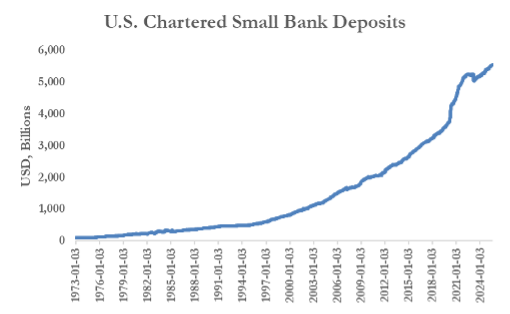

U.S. small banks hold nearly $6 trillion in deposits. Within that pool, corporate treasury and FX accounts, VersaBank’s initial RBTD target market, represent an estimated 5-10% of deposits, or $275-$550 billion. Capturing just 1–2% of that market would translate to $50-$100 billion.

Source: FDIC.

When a U.S. bank’s customer purchases RBTD tokens (representing U.S. dollar deposits), the underlying funds are placed with VersaBank to back those tokens.

Partner banks don’t view this as a capital loss. RBTD-funded dollars might otherwise leave the bank entirely if customers moved funds to alternatives. The tradeoff for partner banks is as follows: forego marginal funding income in exchange for reduced regulatory burden and a competitive digital product, without materially altering the bank’s own balance sheet.

How does this benefit Versa, since its model of holding and managing partner RBTD reserves increases its own asset base, potentially diluting its regulatory ratios? Versa views this as a revenue opportunity to maximally monetize its existing balance sheet by capturing the full effect of fees and interest, with the potential to deploy that money into higher-yielding vehicles.

And let’s not forget about payment processors. Firms like Fiserv and Jack Henry could license VersaBank’s RBTD platform to embed a regulated, interest-bearing digital money layer directly into their core banking and payments infrastructure. While these firms already power account processing, ACH, wires, and card acquiring, they currently lack a compliant mechanism for tokenized real-time deposits that can move across blockchain rails. VersaBank’s infrastructure would let it offer bank-grade digital receipts (CADV/USDV) to thousands of mid-tier banks, enabling instant B2B payments, FX, and programmable treasury tools. This expands its platform defensibility and opens new revenue streams via transaction fees, API access, and yield-sharing on deposit float.

Competitive Dynamics: The Only Institutionally Ready Multi-Party Solution

The concept of tokenized bank deposits is new, but interest is growing in the financial industry. A few large banks have experimented internally (JPMorgan’s JPM Coin for institutional clients), and consortia have discussed interoperable deposit tokens.

However, VersaBank is one of the first to publicly pilot a retail/business-facing deposit token on public blockchains, and importantly, to offer it as a service to other firms. We believe numerous FX trading firms and North American corporations have already signaled their interest in VersaBank’s solution for FX and day-to-day treasury management.

Major stablecoin issuers like Circle (USDC) and Tether could be seen as indirect competitors, but if regulations require stablecoins to be bank-issued, those companies might instead become partners or clients (by partnering with banks for issuance). The GENIUS Act already prohibits stablecoin issuers from paying interest directly, and the OCC's February 2026 proposed rules go further by targeting third-party workarounds like the Circle-Coinbase arrangement. RBTDs, as bank deposits, face no such restriction, and therefore can legally pay interest under existing banking law.

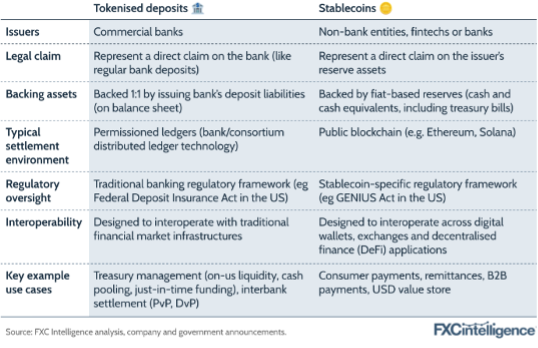

A comparison of tokenized deposits versus stablecoins is shown below.

Source: FXCintelligence.

Along the lines of the comparison above, Visa and Stripe are piloting stablecoins largely aimed at consumer-facing use cases such as retail checkouts, gig economy payouts, and card-like settlement flows where ease of acceptance matters more than yield or balance sheet treatment. In contrast, tokenized deposits like RBTDs are built for institutional money movement: interbank transfers, corporate treasury, and cross-border FX where settlement risk, deposit insurance, and the ability to earn interest on idle balances matter. It may be that stablecoins dominate where commerce meets the consumer, while RBTDs are better suited to the plumbing of wholesale payments and liquidity management.

For now, VersaBank’s first-mover advantage and proprietary IP should give it a head start. Even if that head start translates into only a few percentage points of total market share, the sheer scale of trillions in capital flows could grow the RBTD business exponentially, leading to earnings potential up to 100x its current RPP franchise.

Market Trends: Huge Transaction Volume and Regulatory Tailwinds

The total addressable market for RBTDs is vast, especially when you consider opportunities outside of FX. Extension into interbank treasury liquidity ($500+ billion), institutional cash management ($100+ billion), merchant settlement rails ($10+ billion), and programmable payouts for embedded finance systems ($10+ billion) for Versa’s RBTDs should be considered live options. The stablecoin market itself provides a useful proxy: issuance has already more than doubled to ~$300 billion, and forecasts suggest it could reach $2 trillion by 2028 as tokenized cash becomes a backbone of payment infrastructure, and a possible demand source for U.S. treasuries.

The regulatory background includes two pieces of legislation which both benefit RBTD adoption. The GENIUS and Clarity Act, besides acting as a tailwind for VersaBank’s RBTD offering, indicate that the banking lobby has made sure that the playing field tilts its way. If the rules come out as expected (benefitting FDIC-insured issuers and restricting non-bank stablecoins), VersaBank will have a green light to commercialize RBTDs with far less uncertainty. That could spur rapid growth in deposits and trigger partnerships with fintechs or even bigger banks that prefer not to build their own tech.

Our conversations with regulators suggest there is little concern about the rapid growth of this type of deposit base, given that it is expected to be backed by Treasuries.

iii) DRT Cyber (~C$10M in Revenue, Regulatory Sale by mid-2026)

VersaBank also owns a small U.S.-based cybersecurity consulting subsidiary (DRT Cyber), which performs services like penetration testing for financial institutions and police departments. While a solid business with ~400 clients, it’s non-core. Under U.S. bank regulations, VersaBank is required to divest DRT Cyber by 2026, and as discussed earlier, the likely sale of this unit is a catalyst to simplify the story and return focus to the high-margin banking segments. DRT Cyber is expected to be sold for C$30-$50 million later this year.

iv) Management: “Outsider” Founder-CEO with Impressive 30-Year Track Record

VersaBank is led by David Taylor, a career banker and technologist who has built the institution from the ground up. In 1993, he acquired a small trust company with just C$20 million in assets and used proprietary software to transform it into one of the world’s first fully digital, branchless banks, today exceeding C$6 billion in assets.

Over three decades, his model has delivered virtually zero loan losses, even through multiple credit cycles, underscoring a disciplined approach to risk management. Taylor is known for being ahead of the regulatory curve—sometimes to the bank’s short-term detriment, but consistently validating his vision over time. Taylor retains a ~5% ownership stake, ensuring alignment with shareholders, and his reputation and credibility with regulators have greatly aided VersaBank’s ongoing transformation. Going forward, we believe he has effectively created a regulatory moat, positioning the bank to scale faster and with fewer compliance hurdles than peers.

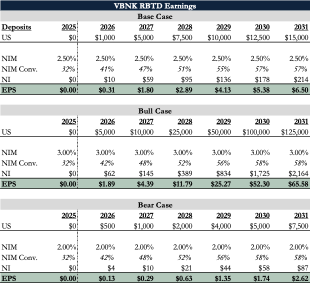

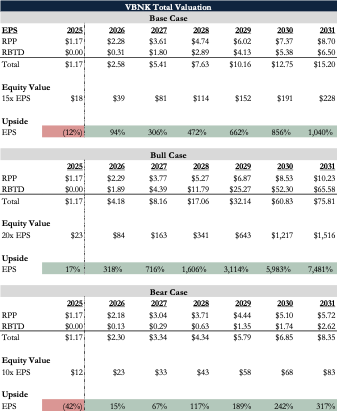

III) Valuation Analysis

VersaBank is rapidly scaling its RPP product in the U.S. while continuing to grow strongly in Canada. We assume RPP assets expand into the tens of billions, maintaining historical economics, even though early signs suggest the U.S. rollout could prove more profitable.

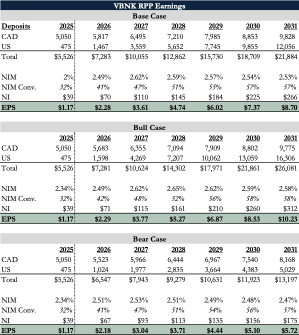

To frame the opportunity, we present three scenarios in which RPP earning assets reach approximately C$13 billion, C$20 billion, and C$25 billion by 2031. In each case, we adjust net interest margins accordingly, while keeping NIM conversion fixed, as the model’s operating leverage should materialize with any level of asset growth. All figures are shown in Canadian dollars.

At a share price of C$20/share, our RPP scenario above implies an earnings yield ranging from 30% to 60%. With future growth, VersaBank trades at 2x to 3.5x P/E depending on the scenario. Through a cycle, considering the bank is highly unlikely to take credit losses and therefore incur book value impairments, we see the bull forecast as an “when, not if” scenario.

Turning to RBTDs, we model three scenarios where treasury-backed earning assets scale to C$7.5 billion, C$15 billion, and C$100+ billion by 2031. We assume a net interest margin of 2% to 3%, though the spread could be higher if RBTDs pay under 1% interest while treasuries yield around 4%.

With earnings yield scenarios ranging from a 15% increase to our bull scenario where EPS is three times the current share price, these projections remain surprisingly conservative on total amount, NIM, and NIM conversion.

As stated before, we believe that the existing customers in discussion with VersaBank already amount to $100 billion in possible RBTD assets set to come on stream in the next few years.

In the case of NIM, this analysis assumes that VersaBank cannot apply some of the capital deposited for RBTDs towards RPP. And with NIM conversion, while we apply VersaBank’s strong operating leverage from RPP to the RBTD analysis, most scaling costs for the RBTD business are already in the past. This means the assumed NIM conversion understates the true profitability since these assets convert nearly 99% of earnings directly to the bottom line, with taxes as the main expense (NIM conversion should be 75%).

Lastly, we don’t include potential earnings from transaction fees, as the upside here is already impressive, though we described them in the RBTD section above.

Bringing everything together, below is our combined valuation of RPP and RBTD for each of the scenarios.

The upside distribution here is uniquely asymmetric, and in the case of RBTD, mostly “free”. Even in the worst case, there’s a 15% gain in 2026 (with 2025 behind us, though shown for completeness). But if RBTD assets scale to $100+ billion in earning assets, the return generated explodes to an astonishing 75x by 2031. This rare risk-reward profile highlights the transformative potential in RBTDs.

Again, we haven’t included license fees that could come from the likes of Fiserv and others. The opportunity set presented above is plenty bullish for now.

IV) Why Now?

VersaBank has spent the last two years laying the groundwork for its U.S. expansion, and that heavy lifting is finally behind it. The upfront costs associated with the acquisition of a U.S. bank charter, and the one-time costs tied to regulatory approvals and operational systems are near completion. The sale of DRT Cyber should free up capital to fund new RPP assets. Against this backdrop, the business is poised to begin scaling RPP in the U.S. at structurally higher margins. And as we hope we’ve made clear, the Real Bank Tokenized Deposits (RBTD) business is primed for a zero-to-one inflection in the next 6-12 months, an option completely free to investors today.

V) Downside Protection

VersaBank is trading around book value and has unique downside protection as a bank that has reported nearly zero credit losses over 30 years. Its RPP contract structure forces partners to repurchase loans that go 90 days delinquent, shielding it from consumer credit risk. Additionally, the sale of DRT Cyber for C$1-$1.60 per share (~10%) further protects VBNK investors’ downside.

VI) Conclusion

Mispriced as a sleepy Canadian bank, VersaBank is a founder-led technology platform with proven credit discipline, downside protection, and a clear runway for asymmetric growth. With U.S. RPPs now scaling, one-time costs rolling off, and index inclusion likely, the stock offers investors a rare chance to buy a compounding bank franchise at around book value. Even with simple improvement in the base business, we believe VBNK can conservatively return 5x over the next five years, a 35%+ IRR per annum.

If RBTDs scale as our research suggests, VersaBank could evolve from a niche bank valued near book into a core infrastructure provider for the next generation of digital payments, commanding fintech-style multiples. Even a modest $10 billion in RBTD deposits could drive an almost 10x return, while $100 billion, already within line of sight from our exhaustive research, could imply over 50x upside.

Disclaimers

+ No guarantee of investment performance

Past performance of the financial instruments mentioned in this report should not be taken as an indication or guarantee of future results. The price, value of, and income from, any of the financial instruments mentioned in this report can rise as well as fall and may be affected by changes in economic, financial and political factors. Any projections, market outlooks or estimates in this presentation are forward looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect their returns or performance. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. Future returns are not guaranteed. If a financial instrument is denominated in a currency other than the investor's home currency, a change in exchange rates may adversely affect the price of, value of, or income derived from that financial instrument. In addition, investors in securities such as ADRs, whose values are affected by the currency of the underlying security, effectively assume currency risk.

+ No guarantee of accuracy

While the information prepared in this document is believed to be accurate, Crossroads Capital, LLC (the “Investment Manager”) makes no representation or warranty as to the completeness, accuracy or timeliness of such information. The Fund and the Investment Manager expressly disclaim all liability for errors or omissions in, or the misuse or misinterpretation of, any information contained herein.

+ No obligation to update or act on information

The Investment Manager has no obligation to update any information contained herein and may make investment decisions that are inconsistent with the views expressed herein. Any holdings of securities discussed herein are under periodic review and are subject to change at any time, without notice.

+ Not a recommendation to buy or sell any security

This report does not provide investment recommendations specific to individual investors. As such, the financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisions based upon their specific objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider this report as only a single factor in making an investment decision. All information provided is for informational purposes only and should not be deemed as investment or other professional advice or a recommendation to purchase or sell any specific security.

+ Not an offer to invest in our Fund

This report, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy limited partnership interests of Crossroads Capital Investment Partners, LP (the “Fund”) which may only be made at the time a qualified offeree receives a confidential private offering memorandum (“CPOM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the CPOM, the CPOM shall control. The interests shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution.

+ Other disclaimers

All trade names, trademarks, and service marks herein are the property of their respective owners, who retain all proprietary rights over their use. This document is confidential and may not be disseminated or reproduced without the prior written consent of the Investment Manager.

"Roads? Where we're going, we don't need roads." —Dr. Emmett Brown, Back to The Future

Why Merlin?

At the end of the 1985 classic sci-fi comedy Back to the Future, the eccentric but brilliant scientist Emmett “Doc” Brown utters the famous quote on the cover page of this report as his DeLorean lifts into the sky: “Roads? Where we’re going, we don’t need roads.” In aviation, Merlin Labs (MRLN) is making a similar conceptual leap—away from the traditional limitations of runways and human pilot constraints, and toward a world where autonomy radically expands the capabilities of legacy airframes.

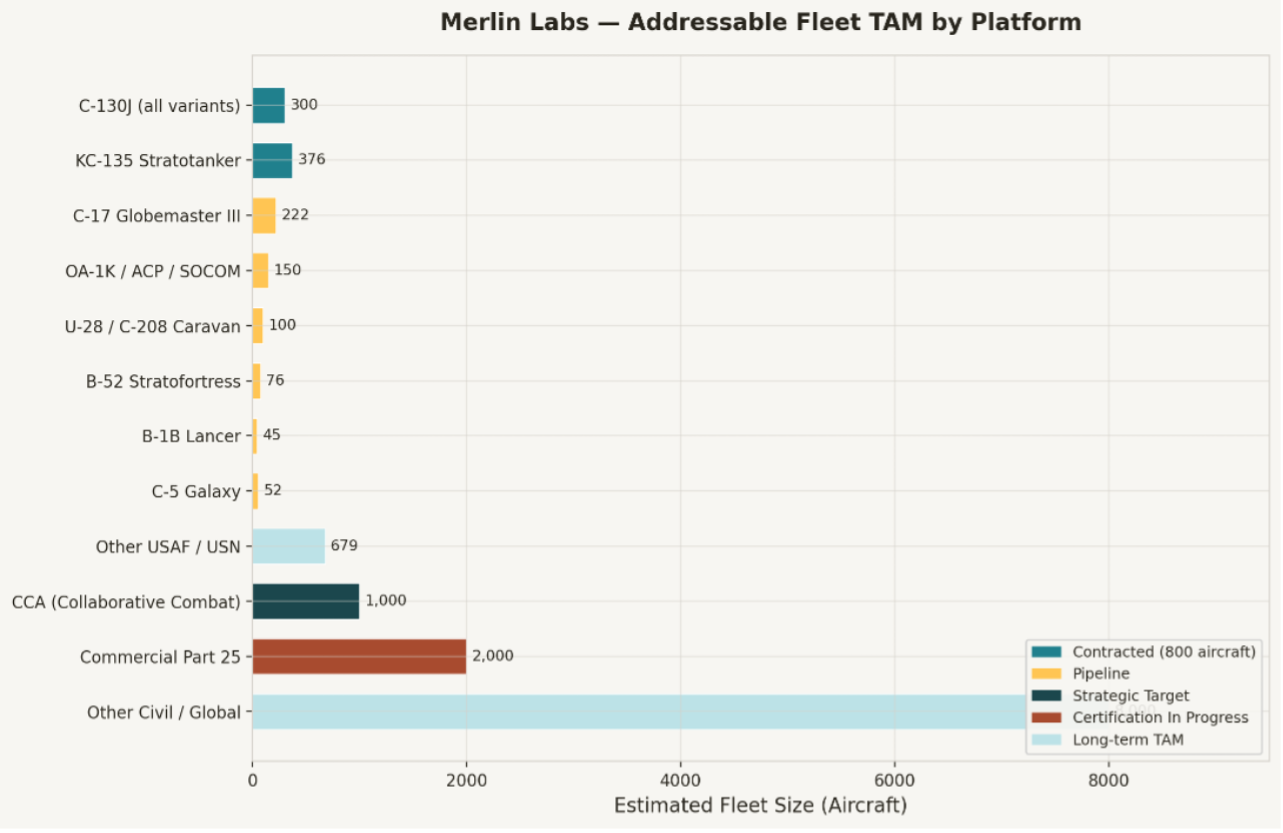

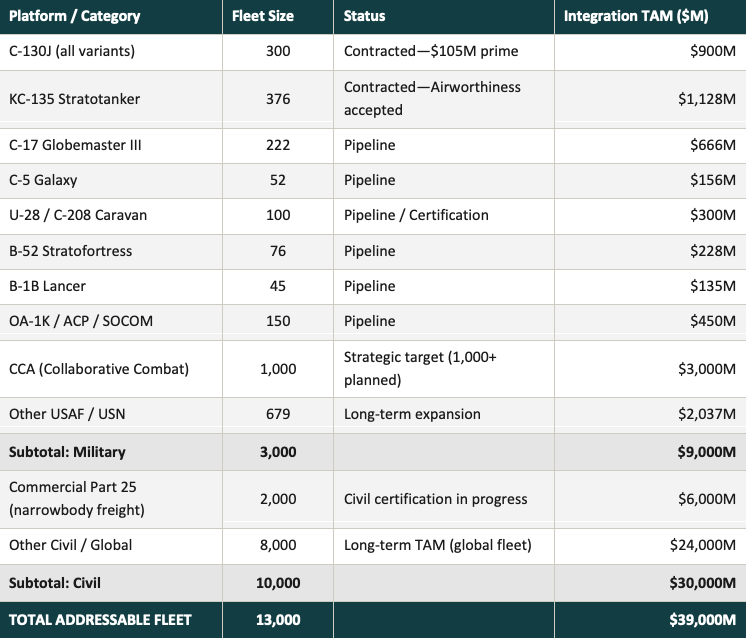

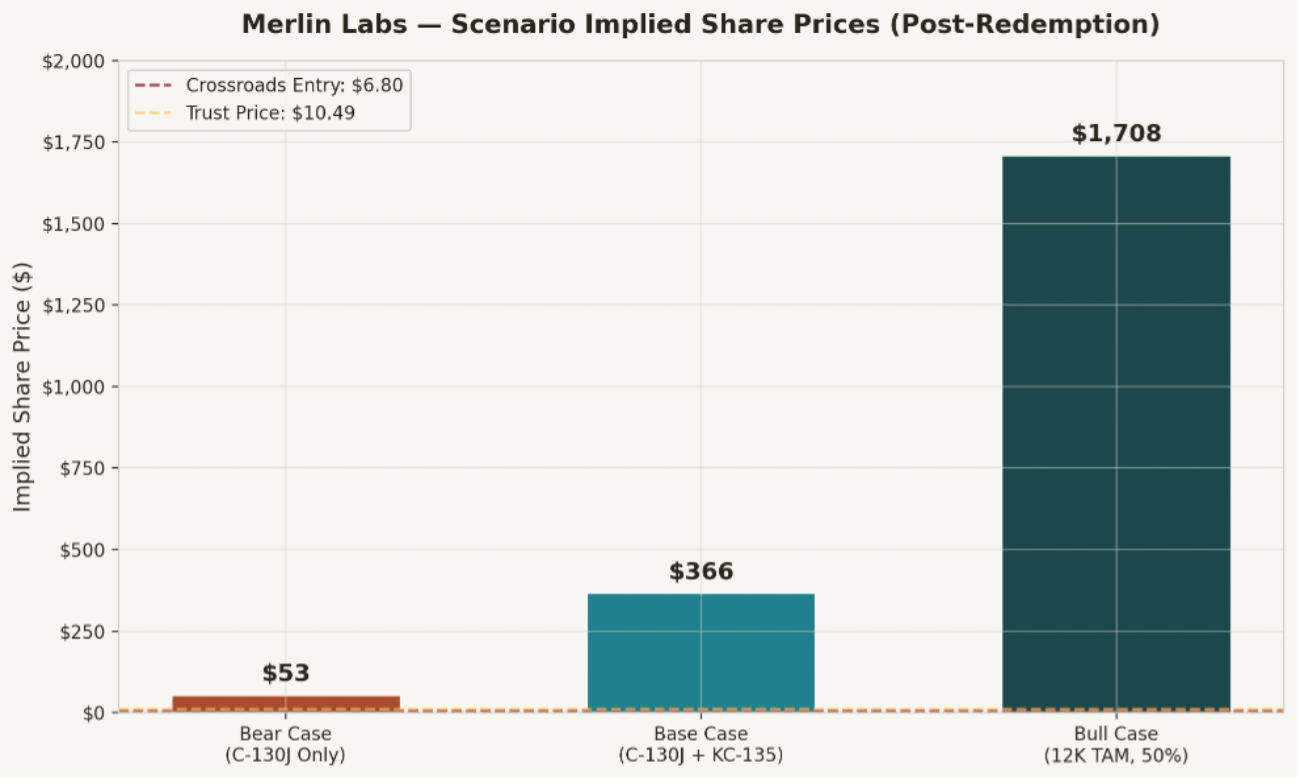

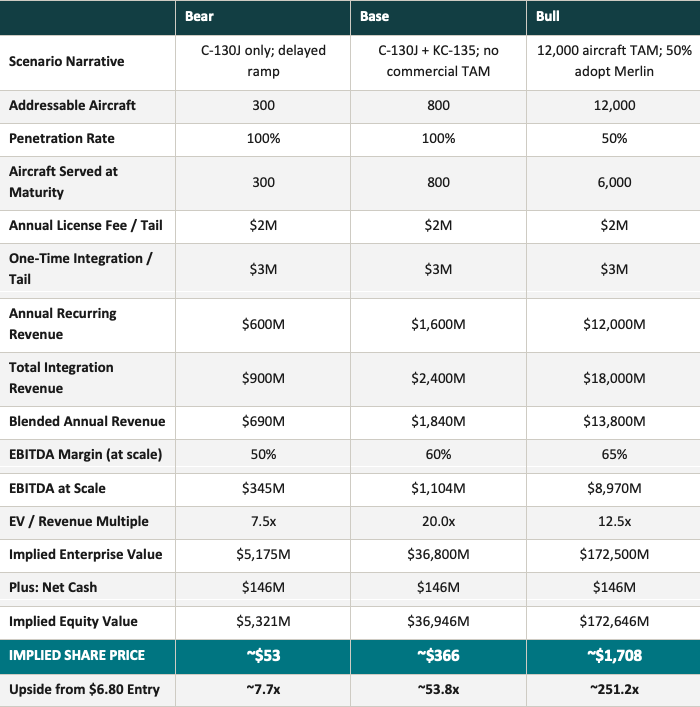

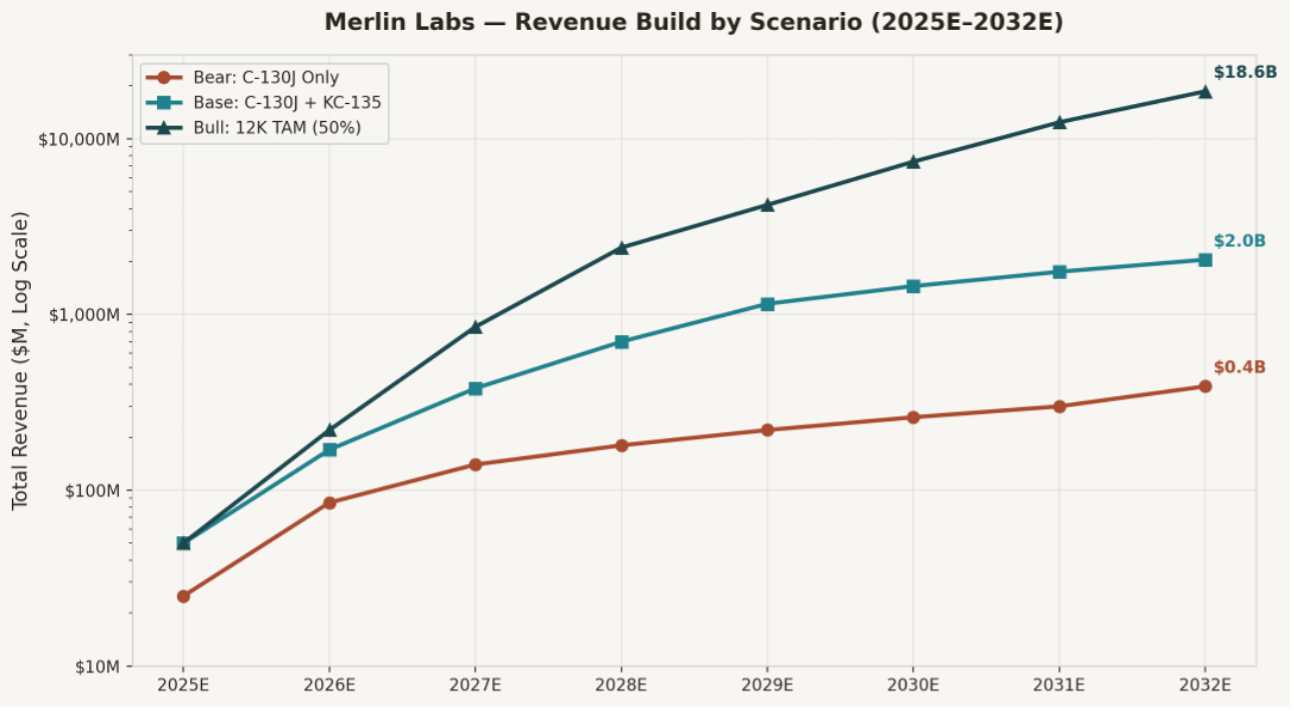

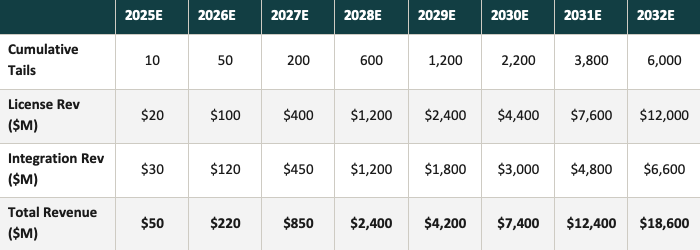

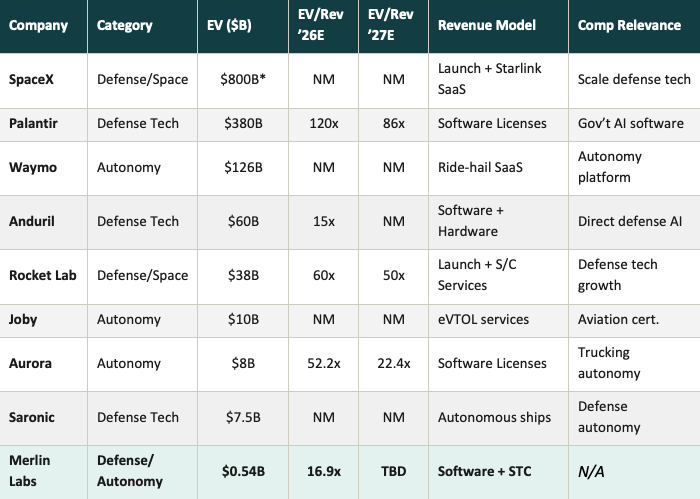

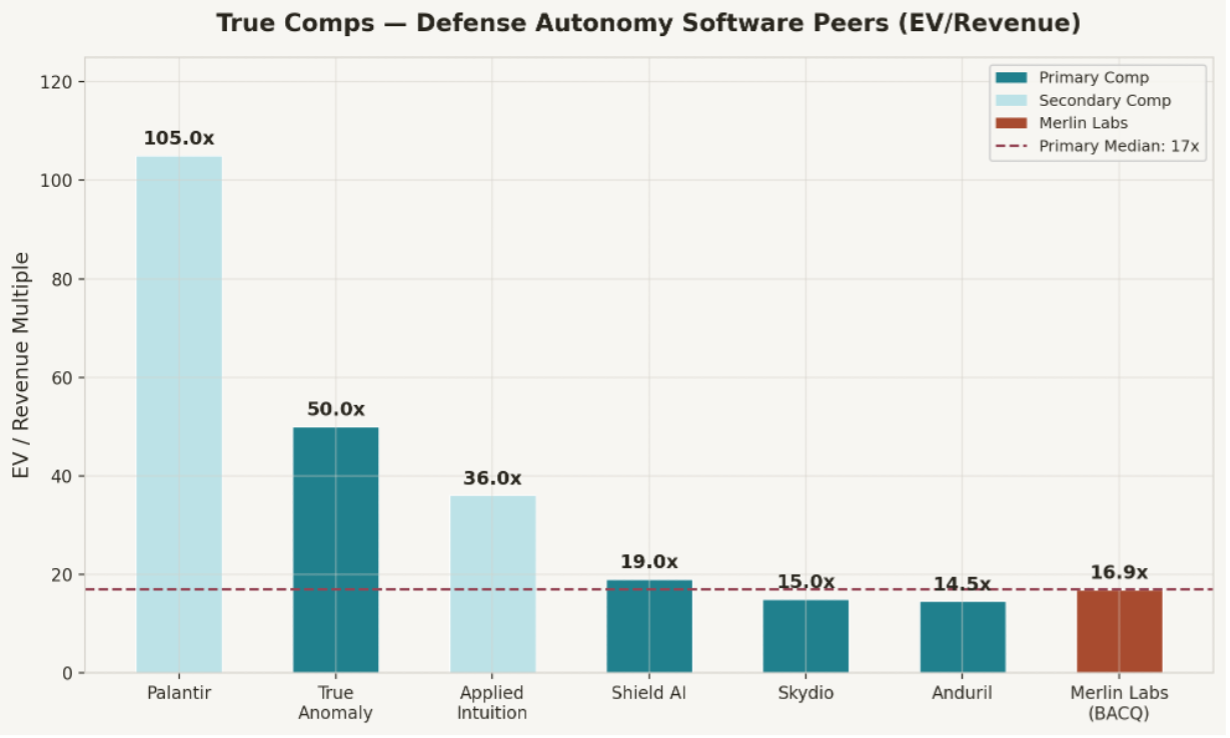

Merlin is building one of the world’s first autonomous digital pilots—not an incremental improvement to legacy autopilot systems, but a fundamental reimagining of how autonomy integrates with human‑crewed aircraft. Traditional autopilot handles steady‑state cruise; Merlin’s aircraft‑agnostic AI listens to live air‑traffic control radio, interprets complex human instructions in real time, and executes entire missions from taxi to landing. Unlike traditional autopilot, its AI “flight OS” is designed to make real‑time decisions, operate in GPS‑denied environments, and replace the scarcest, most expensive input in aviation: skilled pilots on critical missions. On the defense side alone, Merlin already has over 800 aircraft under contract across platforms like the C‑130J and KC‑135, implying roughly $3 million per tail in upfront integration and $2 million in annual recurring software revenue once fully ramped—a $1.6-billion ARR line of sight within the next several years on just these two aircraft alone. At our roughly $6.80 per‑share economic cost basis via rights (BACQR), we believe the current valuation reflects SPAC stigma and general investor ignorance more than business quality, creating a rare case where a frontier defense‑grade autonomy asset trades at a deep discount to normalized earnings a few years from today.

Our variant view is simple: the market sees a quirky SPAC and a hard‑to‑model autonomy story without much disclosure; we see the leading candidate to become the operating system of record for defense‑grade autonomous flight, backed by tier‑one partners (GE Aerospace, Northrop Grumman, Honeywell), Baillie Gifford and other high‑signal PIPE investors, and an installed‑base licensing model with clear unit economics. If Merlin merely executes on existing defense programs, we see multi‑bagger potential; if it successfully extends into broader U.S. and allied defense fleets and selected civil use cases over time, the upside is an order of magnitude higher.

Why Now?

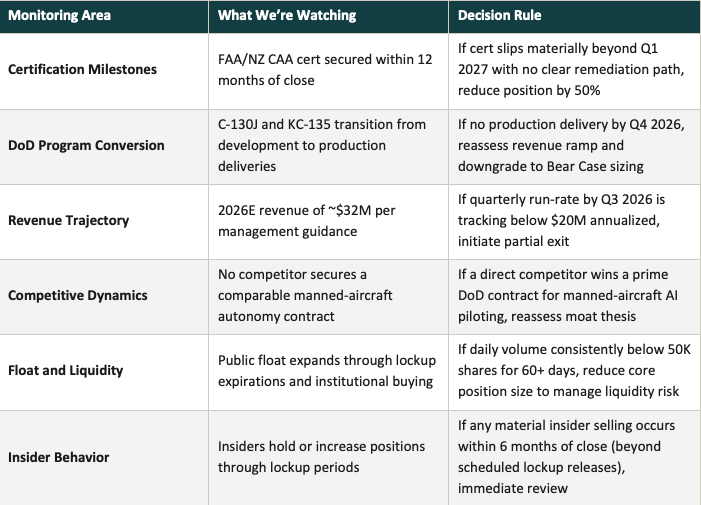

Merlin’s first day of trading was March 17, 2026, after going public via a business combination with Inflection Point Asset Management (more on them later). We believe the company sits ahead of the competition to establish itself as a category-defining AI-driven defense and autonomy platform—a market niche that commands among the highest multiples within the broader software market. In our view, Merlin is the rarest kind of IPO: one where the technology is already flying, the contracts are already signed, and the insiders who know the story best used the quiet period before public price discovery to increase their positions rather than cash out. We think now is the inflection point because three structural pressures are converging. First, the U.S. Air Force has been roughly 2,000 pilots short of its 21,000‑person requirement for over a decade, with shortages projected to worsen as pilots age and demand rises. Second, pilot expense accounts for roughly 11–25% of total operating costs for commercial cargo operators, making any credible single‑pilot solution immediately interesting to both defense and civil customers. Third, GPS‑denied navigation has shifted from theoretical edge case to operational requirement in modern electronic warfare environments, elevating the value of Merlin’s ability to operate independently of GPS or continuous ground links.

We believe Merlin’s shrewd decision to focus near‑ and medium‑term on semi‑autonomous, single‑pilot operations—rather than going straight for fully autonomous flight—is a key part of the story and couldn’t have come at a more opportune time. In practical terms, taking DoD aircraft from two pilots to one with Merlin installed represents around $7 million of annual savings per aircraft and hundreds of millions in aggregate on a $7–10 billion annual aircraft and pilot operations budget. Regulatory progress is tracking that pragmatism: Merlin is the only peer to have secured U.S. FAA approval for a key avionics’ module, a roughly five‑year process that confers a meaningful first‑mover advantage and has already achieved SOI‑2 regulatory milestones with New Zealand’s aviation authority under a framework that can accelerate reciprocal FAA approval. Naturally we believe retrofitting existing aircraft is the near-term commercial beachhead. Merlin’s platform‑agnostic, backwards‑compatible system allows customers to upgrade in‑service military and commercial fleets rather than rip‑and‑replace for new-built hardware, converting tens of thousands of already‑owned aircraft into a future recurring‑software revenue base. That retrofit‑first strategy, combined with cost‑plus to fixed‑fee contract structures and IDIQ ceilings that can be raised without re‑bids, creates a capital‑efficient path from initial engineering programs to high‑margin software annuities as fleets are converted over time. Together, these forces don’t just create a market opportunity—they create an urgency that rewards whichever platform establishes fleet-wide lock-in first, making the architecture and contract structure of Merlin’s business a central question. In our view, Merlin’s architecture and contract structure matter because they are what turn a one‑off autonomy demo into a durable, high‑margin software annuity: a retrofit‑first, aircraft‑agnostic “flight OS” installed via cost‑plus IDIQ contracts that then convert into $2 million per‑tail annual licenses across an 800‑aircraft (and growing) defense fleet. Business Overview

Merlin first appeared on our radar somewhat by chance. As a concentrated fund with large investments in AST SpaceMobile (“ASTS”) and FTAI Aviation (“FTAI”), we spend a disproportionate amount of time studying adjacent space‑technology and aerospace/defense themes, and Merlin emerged from that work as an unexpected potential category leader. Discovering a company with a plausible pole position at the vanguard of a paradigm shift in aviation was not on our bingo card, to put it lightly.

As noted above, Merlin is developing “aircraft‑agnostic” AI software known as the Merlin Pilot, with the long‑term goal of giving every plane the power to fly itself from takeoff to touchdown. What stands out is not just the ambition, but the sequencing: management has taken an astute, pragmatic path, moving in lockstep with customers, partners, and regulators with a near‑ and medium‑term focus on semi‑autonomous, single‑pilot operations rather than leaping straight to full autonomy.

Recall, Pilot is a platform‑agnostic, integrated system that is backwards‑compatible with older and in‑service aircraft. This matters because retrofitting existing aircraft is by far the most relevant near‑term use case, as customers can meaningfully reduce human‑pilot hours and mitigate structural pilot shortages without buying a single new airframe.

By focusing on semi‑autonomous retrofit, Merlin has aligned itself with the current appetite of regulators and defense customers, establishing real product‑market fit instead of building science‑project technology years ahead of demand. In our experience aviation software is crowded with moonshot R&D programs that promise the world but require heavy maintenance overhauls and/or full fleet rip‑and‑replace approach. Merlin’s backwards compatibility, by contrast, unlocks massive capital efficiency and rapid market penetration by upgrading existing military and commercial fleets rather than waiting for new‑build aircraft. In plain English, Merlin is turning tens of thousands of already‑owned planes into a future high margin recurring revenue base, with far lower upfront cost and fewer regulatory and operational hurdles than alternative paths.

Regulatory progress is tracking this strategy. Merlin is the only peer to have secured U.S. FAA approval for a key avionics module, a roughly five‑year process that confers a meaningful first‑mover advantage. Outside the U.S., the company has obtained a flight‑testing certificate and Stage of Involvement 2 (SOI‑2) clearance from New Zealand’s aviation authority for its software review process—a milestone that confirms a significant portion of Merlin’s Flight Control Computer data and testing has been reviewed and accepted. Bilateral arrangements between New Zealand and the FAA for reciprocal recognition of certain airworthiness approvals should, in our view, accelerate progress toward full U.S. certification.

On the commercial side, Merlin Pilot targets cargo and regional operators seeking autonomy without buying new airframes. Early work with Ameriflight already points to strong retrofit demand and compelling fleet economics. That said, we expect the near‑ and medium‑term story to be dominated by military and defense applications, where Merlin appears almost unnaturally well suited to the moment.

All of which is to say that the operating momentum building beneath the surface is real. Merlin has successfully leveraged deep industry relationships to secure tier‑one partnerships across the U.S. military and defense ecosystem. USSOCOM has awarded a $105 million production contract to automate the C‑130J, and the U.S. Air Force has signed an additional agreement to test Merlin’s AI‑enabled software on the KC‑135. These programs create a visible pathway from prototypes to fleet‑wide adoption. Put differently, Merlin is not just another autonomy vendor bidding for grants; we believe it is on track to become the first true defense‑grade autonomy prime contractor in aviation—a substantial feat, and one that should be well rewarded in public markets if the team simply continues to execute on existing contracts. Pivotal Players Merlin is led by founder and CEO Matt George, who previously served in the Executive Office of the President of the United States, where he supported presidential initiatives with a focus on healthcare and data analytics, and who subsequently founded and led venture-backed transportation startup Bridj. George conceived Merlin after a near-miss with a JetBlue aircraft while learning to fly in Vermont—an experience that crystallized the case for aviation based autonomous systems that could eliminate the most common sources of human error. He has been building Merlin ever since (November 2018), deliberately sitting out the SPAC frenzy of 2020–2022 to focus on product development and contract execution before bringing the company public.