—Dr. Emmett Brown, Back to The Future

Why Merlin?

At the end of the 1985 classic sci-fi comedy Back to the Future, the eccentric but brilliant scientist Emmett “Doc” Brown utters the famous quote on the cover page of this report as his DeLorean lifts into the sky: “Roads? Where we’re going, we don’t need roads.” In aviation, Merlin Labs (MRLN) is making a similar conceptual leap—away from the traditional limitations of runways and human pilot constraints, and toward a world where autonomy radically expands the capabilities of legacy airframes.

Merlin is building one of the world’s first autonomous digital pilots—not an incremental improvement to legacy autopilot systems, but a fundamental reimagining of how autonomy integrates with human‑crewed aircraft. Traditional autopilot handles steady‑state cruise; Merlin’s aircraft‑agnostic AI listens to live air‑traffic control radio, interprets complex human instructions in real time, and executes entire missions from taxi to landing. Unlike traditional autopilot, its AI “flight OS” is designed to make real‑time decisions, operate in GPS‑denied environments, and replace the scarcest, most expensive input in aviation: skilled pilots on critical missions.

On the defense side alone, Merlin already has over 800 aircraft under contract across platforms like the C‑130J and KC‑135, implying roughly $3 million per tail in upfront integration and $2 million in annual recurring software revenue once fully ramped—a $1.6-billion ARR line of sight within the next several years on just these two aircraft alone. At our roughly $6.80 per‑share economic cost basis via rights (BACQR), we believe the current valuation reflects SPAC stigma and general investor ignorance more than business quality, creating a rare case where a frontier defense‑grade autonomy asset trades at a deep discount to normalized earnings a few years from today.

Our variant view is simple: the market sees a quirky SPAC and a hard‑to‑model autonomy story without much disclosure; we see the leading candidate to become the operating system of record for defense‑grade autonomous flight, backed by tier‑one partners (GE Aerospace, Northrop Grumman, Honeywell), Baillie Gifford and other high‑signal PIPE investors, and an installed‑base licensing model with clear unit economics. If Merlin merely executes on existing defense programs, we see multi‑bagger potential; if it successfully extends into broader U.S. and allied defense fleets and selected civil use cases over time, the upside is an order of magnitude higher.

Why Now?

Merlin’s first day of trading was March 17, 2026, after going public via a business combination with Inflection Point Asset Management (more on them later). We believe the company sits ahead of the competition to establish itself as a category-defining AI-driven defense and autonomy platform—a market niche that commands among the highest multiples within the broader software market. In our view, Merlin is the rarest kind of IPO: one where the technology is already flying, the contracts are already signed, and the insiders who know the story best used the quiet period before public price discovery to increase their positions rather than cash out.

We think now is the inflection point because three structural pressures are converging. First, the U.S. Air Force has been roughly 2,000 pilots short of its 21,000‑person requirement for over a decade, with shortages projected to worsen as pilots age and demand rises. Second, pilot expense accounts for roughly 11–25% of total operating costs for commercial cargo operators, making any credible single‑pilot solution immediately interesting to both defense and civil customers. Third, GPS‑denied navigation has shifted from theoretical edge case to operational requirement in modern electronic warfare environments, elevating the value of Merlin’s ability to operate independently of GPS or continuous ground links.

We believe Merlin’s shrewd decision to focus near‑ and medium‑term on semi‑autonomous, single‑pilot operations—rather than going straight for fully autonomous flight—is a key part of the story and couldn’t have come at a more opportune time. In practical terms, taking DoD aircraft from two pilots to one with Merlin installed represents around $7 million of annual savings per aircraft and hundreds of millions in aggregate on a $7–10 billion annual aircraft and pilot operations budget. Regulatory progress is tracking that pragmatism: Merlin is the only peer to have secured U.S. FAA approval for a key avionics’ module, a roughly five‑year process that confers a meaningful first‑mover advantage and has already achieved SOI‑2 regulatory milestones with New Zealand’s aviation authority under a framework that can accelerate reciprocal FAA approval.

Naturally we believe retrofitting existing aircraft is the near-term commercial beachhead. Merlin’s platform‑agnostic, backwards‑compatible system allows customers to upgrade in‑service military and commercial fleets rather than rip‑and‑replace for new-built hardware, converting tens of thousands of already‑owned aircraft into a future recurring‑software revenue base. That retrofit‑first strategy, combined with cost‑plus to fixed‑fee contract structures and IDIQ ceilings that can be raised without re‑bids, creates a capital‑efficient path from initial engineering programs to high‑margin software annuities as fleets are converted over time. Together, these forces don’t just create a market opportunity—they create an urgency that rewards whichever platform establishes fleet-wide lock-in first, making the architecture and contract structure of Merlin’s business a central question.

In our view, Merlin’s architecture and contract structure matter because they are what turn a one‑off autonomy demo into a durable, high‑margin software annuity: a retrofit‑first, aircraft‑agnostic “flight OS” installed via cost‑plus IDIQ contracts that then convert into $2 million per‑tail annual licenses across an 800‑aircraft (and growing) defense fleet.

Business Overview

Merlin first appeared on our radar somewhat by chance. As a concentrated fund with large investments in AST SpaceMobile (“ASTS”) and FTAI Aviation (“FTAI”), we spend a disproportionate amount of time studying adjacent space‑technology and aerospace/defense themes, and Merlin emerged from that work as an unexpected potential category leader. Discovering a company with a plausible pole position at the vanguard of a paradigm shift in aviation was not on our bingo card, to put it lightly.

As noted above, Merlin is developing “aircraft‑agnostic” AI software known as the Merlin Pilot, with the long‑term goal of giving every plane the power to fly itself from takeoff to touchdown. What stands out is not just the ambition, but the sequencing: management has taken an astute, pragmatic path, moving in lockstep with customers, partners, and regulators with a near‑ and medium‑term focus on semi‑autonomous, single‑pilot operations rather than leaping straight to full autonomy.

Recall, Pilot is a platform‑agnostic, integrated system that is backwards‑compatible with older and in‑service aircraft. This matters because retrofitting existing aircraft is by far the most relevant near‑term use case, as customers can meaningfully reduce human‑pilot hours and mitigate structural pilot shortages without buying a single new airframe.

By focusing on semi‑autonomous retrofit, Merlin has aligned itself with the current appetite of regulators and defense customers, establishing real product‑market fit instead of building science‑project technology years ahead of demand. In our experience aviation software is crowded with moonshot R&D programs that promise the world but require heavy maintenance overhauls and/or full fleet rip‑and‑replace approach. Merlin’s backwards compatibility, by contrast, unlocks massive capital efficiency and rapid market penetration by upgrading existing military and commercial fleets rather than waiting for new‑build aircraft. In plain English, Merlin is turning tens of thousands of already‑owned planes into a future high margin recurring revenue base, with far lower upfront cost and fewer regulatory and operational hurdles than alternative paths.

Regulatory progress is tracking this strategy. Merlin is the only peer to have secured U.S. FAA approval for a key avionics module, a roughly five‑year process that confers a meaningful first‑mover advantage. Outside the U.S., the company has obtained a flight‑testing certificate and Stage of Involvement 2 (SOI‑2) clearance from New Zealand’s aviation authority for its software review process—a milestone that confirms a significant portion of Merlin’s Flight Control Computer data and testing has been reviewed and accepted. Bilateral arrangements between New Zealand and the FAA for reciprocal recognition of certain airworthiness approvals should, in our view, accelerate progress toward full U.S. certification.

On the commercial side, Merlin Pilot targets cargo and regional operators seeking autonomy without buying new airframes. Early work with Ameriflight already points to strong retrofit demand and compelling fleet economics. That said, we expect the near‑ and medium‑term story to be dominated by military and defense applications, where Merlin appears almost unnaturally well suited to the moment.

All of which is to say that the operating momentum building beneath the surface is real. Merlin has successfully leveraged deep industry relationships to secure tier‑one partnerships across the U.S. military and defense ecosystem. USSOCOM has awarded a $105 million production contract to automate the C‑130J, and the U.S. Air Force has signed an additional agreement to test Merlin’s AI‑enabled software on the KC‑135. These programs create a visible pathway from prototypes to fleet‑wide adoption. Put differently, Merlin is not just another autonomy vendor bidding for grants; we believe it is on track to become the first true defense‑grade autonomy prime contractor in aviation—a substantial feat, and one that should be well rewarded in public markets if the team simply continues to execute on existing contracts.

Pivotal Players

Merlin is led by founder and CEO Matt George, who previously served in the Executive Office of the President of the United States, where he supported presidential initiatives with a focus on healthcare and data analytics, and who subsequently founded and led venture-backed transportation startup Bridj. George conceived Merlin after a near-miss with a JetBlue aircraft while learning to fly in Vermont—an experience that crystallized the case for aviation based autonomous systems that could eliminate the most common sources of human error. He has been building Merlin ever since (November 2018), deliberately sitting out the SPAC frenzy of 2020–2022 to focus on product development and contract execution before bringing the company public.

George’s public statements reveal a founder who speaks with the clarity and conviction of someone who knows exactly where the company needs to go. At the BCA signing, he declared: “We’re taking Merlin public to deliver the world’s first defense-grade autonomy stack and advance towards delivering the operating system of record for aircraft big and small. Our national security represents the highest stakes proving ground. Defense airframes log over four million flight-hours per year; AI that has earned trust there earns it anywhere.” And when the PIPE was upsized, the message carried the same frequency: “This additional capital reflects the strong momentum we’ve built since announcing our SPAC transaction and the confidence investors have in our revenue growth, scalability, and path toward becoming a public company.”

We believe George has the disciplined urgency of a pioneering founder who has spent seven years building Merlin in the shadows before inviting in the spotlights of public markets. We believe Merlin is a long-term story, one measured in fleet penetration and software annuity revenue, not quarterly earnings beats, as the technology seeks to become an operating system of record offering defense-grade autonomy. For a better sense of why we think Mr. George is the right kind of crazy for this mission, read his first letter to shareholders released in the days leading up to this week’s IPO.

We’ve also been impressed with the team George has assembled around him, a necessary ingredient for any scale up operating in a frontier industry. CTO Tim Burns brings deep aerospace engineering credibility: Chief Engineer positions at Honda Aircraft Company and L3Harris Technologies, and Vice President of Engineering at Thales Aerospace. Chief Program Officer Krishnan Anand, who oversees management and strategic execution of Merlin’s autonomy programs, brings prior experience at Supernal, Wisk, and Lockheed Martin. In advance of the public listing, Merlin further expanded its leadership bench with new CLO Leslie Ravestein, CPO David Lasater, and CFO Ryan Carrithers—signaling a deliberate build-out of institutional-grade corporate infrastructure, exactly as we’d expect to see at this critical juncture.

Most importantly, this is a team that has prioritized execution over promotion. Merlin did not pursue a traditional roadshow ahead of its listing. Management stayed quiet during the SPAC process—an approach we read as intentional and revealing. When insiders have conviction in a story that the market has not yet priced, the rational move is to accumulate before public price discovery, not to generate attention that competes with their own buying. That is precisely what happened here.

Michael Blitzer and Kingstown Capital

Then there is Michael Blitzer—the man behind the SPAC itself. Blitzer is the founder and co-CEO of Kingstown Capital Management, which he launched in 2006 and grew into a multi-billion-dollar asset manager serving some of the world’s largest endowments and foundations. After starting his career at J.P. Morgan Securities—Blitzer joined Gotham Asset Management (later Gotham Capital), the investment fund founded by the legendary Joel Greenblatt. Greenblatt, for those unfamiliar, is the architect of the “Magic Formula” and one of the most respected value investors of his generation. To us, working under Greenblatt means learning one thing above all else: how to identify situations where the market is profoundly wrong and bet accordingly.

As Chairman and CEO of Inflection Point Acquisition Corp., Blitzer is the architect of the Merlin SPAC. This is not his first rodeo. Previous SPAC deals include Intuitive Machines (LUNR, +65% from trust), USA Rare Earth (USAR, +41%), with another, Air Water Ventures, coming soon. Blitzer’s 19-year investment track record suggests he knows how to identify asymmetric opportunities but also, the ability to bring to market companies in the defense and strategic-tech niche.

Blitzer’s own words paint the picture beautifully: “We believe that Merlin is primed to become a national asset that will play a critical role in the future of aerospace and defense for both military and commercial applications.” And on the PIPE upsizing: “Merlin’s expanded PIPE is a validation of its continued execution on its business plan and the critical role it holds in the nation’s aerospace and defense industries. The company’s AI powered software is quickly becoming a strategically important technology asset that has been adopted by leading companies such as GE Aerospace and Northrop Grumman.” When an investor such as Blitzer calls Merlin “a national asset,” that carries weight beyond the usual SPAC sponsor rhetoric. This is not a typical SPAC promoter looking for a fee—it’s a career special situations-centric value investor who we believe sees the same asymmetric setup we do.

Skin in the Game: The 100% Equity Rollover

Existing Merlin shareholders rolled 100% of their equity into the new public company. Not 80%. Not 90%. One hundred percent. In a typical SPAC, insiders take partial liquidity at close—a rational move that provides a personal hedge while maintaining exposure to the upside. George and his team did the opposite. They chose to convert every dollar of their private equity into New Merlin Common Stock, binding themselves with strict lock-up agreements that prohibit selling, pledging, or hedging their economic interest. This is not a well marketed IPO where previous owners cashed out through the merger. Rather, it’s a backdoor IPO done quietly, where all of the company’s pre public equity holders decided to bet everything on the public market’s ability to eventually recognize the value in what they’ve built - and continue to build.

The signal value here is mathematically profound. At the $800 million pre-money equity valuation established in the BCA, the legacy Merlin Equity Holders (excluding pre-funded convertible notes) were allocated approximately 71.39 million shares. Matt George, as founder and CEO, holds a significant portion of that equity. While exact founder ownership has not been publicly disclosed, a realistic implied range based on typical founder stakes in venture-backed companies at this stage (10%-30%) puts George’s equity value at the IPO somewhere between $80 million and $240 million.

That is not play money. At the midpoint of that range, George has roughly $160 million riding on the exact same shares trading in the open market today. He has no structured liquidity event. Every dollar of upside—and every dollar of downside—accrues to him in the same proportion as it does to Crossroads. When a founder puts $100–200+ million of personal wealth (essentially their entire net worth) into a public vehicle with no exit hatch, you do not need to read the investor deck to understand his conviction level.

And George is not alone. On the SPAC sponsor side, Blitzer’s Inflection Point entity holds a locked-up block of 8.80 million shares. This consists of 8.33 million Founder Shares acquired at a nominal cost (approximately $0.003 per share) following a partial forfeiture plus 467,500 shares from private placement units. Blitzer’s economics are tied directly to the stock’s long-term performance—his promote is only meaningful if the deal works.

The Denominator Effect: Super-Concentration by Redemption

What makes this setup entirely unique based on our memory of recent de-SPACs is how the public market’s skepticism actually fortified insider control. At the merger vote, 90.3% of public shareholders redeemed, draining 22.55 million shares from the public float, an outcome we believe was engineered by design, but more on that at another time.

For now, consider how Merlin’s 90.3% redemption ratio created a massive "denominator effect." Because the 71.39 million legacy shares and the 8.80 million sponsor shares were fixed and non-redeemable, the elimination of the public float mechanically concentrated their power. The remaining shareholder base is now overwhelmingly composed of the Merlin founding team, the SPAC sponsor, strategic PIPE investors, and long-duration institutional capital like Crossroads.

In our experience, the single best predictor of long-term equity returns is insider alignment. When the founder rolls 100% of his equity and the anchor PIPE investors commit over $200 million above trust value to ensure the deal will close under all scenarios—going as far as to fund nearly $80 million of the business combination in cash at the deals announcement (rather than at close![1])—that is a setup that immediately raised an eyebrow and set this investment team to work.

[1] A first forany SPAC as far as we’re aware. Common sense told us we should look deeperbased on this data point alone.

In fact, several aspects of this transaction struck us as specifically designed to enable knowledgeable insiders to obtain additional shares while simultaneously discouraging outside investors from participation. But wait, why would they want to discourage participation prior to close you ask. Isn’t that effectively the same as wanting a low price for their IPO?

Yes, that’s exactly what we are saying. Paraphrasing the great Peter Lynch, what happens when the founder, directors, early marquee investors, and the SPAC sponsor who put the deal together and who hope to buy more shares, are all on the same side of the table - especially when the insiders themselves aren’t legally required by fiduciary duty to price a stock that they themselves are going to buy? Well, wouldn’t you want the same thing if you wanted to buy more of something?

Although we typically steer clear of investments that are hard to grasp, this situation warranted an exception. Once we realized that insiders were essentially hoping SPAC IPO investors would pass on the new issues post IPO equity, that became all the motivation needed to dig in and figure out exactly what was going on here.

Follow the Money

“Value investing…as in, buy something when all is quiet…when the company is trying to keep things quiet and insiders are accumulating…when the silence is designed to shake you out of your position.” – Michael Burry

We think insider behavior around the Merlin Labs transaction tells a clearer story than any investor deck. The headline 90.3% redemption rate looks like a red flag if you pattern‑match to the average de‑SPAC, but in this case it neither impaired Merlin’s balance sheet nor meaningfully threatened deal closure. Instead, insiders and long‑duration capital engineered a non‑redeemable backstop that effectively used the SPAC structure to concentrate control in the hands of the people who know the asset best should it’s public offering be ignored.

As the Business Combination Agreement (BCA) progressed, that “smart money” doubled down. By November 17, 2025, the Closing PIPE investor increased its commitment to 100 million dollars of Series A preferred at $10.20 per share, supplemented by an additional $20 million tranche at $12 per share from other accredited investors. Pre‑funded convertible note holders injected roughly 78 million dollars at signing and later added $9.3 million more, bringing total pre‑funded capital north of $87 million. Net of transaction costs, Merlin emerged with approximately $146 million in cash—enough to fund three to four years of burn at current run‑rates and likely engineered to support an accelerated R&D and production ramp plus selective M&A over the next couple of years.

While we’d never rule out additional capital raises or debt down the line if revenue doesn’t ramp as quickly as expected, the more consequential points revolve around the pivotal players involved. In other words, we’d propose the real signal sits in who wrote those checks. Baillie Gifford—whose early, high‑conviction bets on Tesla, SpaceX, and Amazon are institutional lore—was already on the cap table and then chose to participate again in the PIPE and again when it was upsized from $125 million to more than $200 million. Michael Blitzer and Inflection Point committed heavily on the sponsor side, aligning their promote economics with long‑term stock performance rather than a quick flip. To protect this $200 million+ capital injection, the consortium secured meaningful warrant coverage, including downside protection that can reset exercise prices to a $5.00 floor if the stock underperforms.

While the warrant structure represents a theoretical dilution overhang, we believe the signal is unambiguous: the investors closest to the technology and the contracts—those with the deepest diligence—wanted more. Which makes all the sense in the world, if only because all of this unfolded against a backdrop of steadily improving fundamentals. Since the deal was announced, Merlin secured a $105 million C‑130J IDIQ with USSOCOM, airworthiness approval on the KC‑135, Stage of Involvement‑2 certification from New Zealand’s Civil Aviation Authority, and a GE Aerospace “Program of Record” designation for integration into its Flight Management System. Each of these milestones should, in a normally marketed pre-IPO roadshow, have driven meaningful appreciation in the stock ahead of listing; instead, Merlin stayed almost entirely silent while insiders and anchor investors increased their stakes, stabilized the balance sheet, and let redemptions wash short‑term capital out of the float. In our experience, that pattern—quiet fundamentals up and quiet insider buying—is rarely random.

PIPE Investor Analysis: Baillie Gifford and the Conviction Signal

When Baillie Gifford writes a check, the smart money pays attention. Indeed, over the last decade Baillie backed several notable multi-baggers including NVIDIA, Tesla, Netflix, Amazon, and Spotify, all multiplying in value by a factor of 10x or more.

We mention it up top because this is not an index hugging generalist allocator chasing deal flow—this is the Edinburgh-based firm that backed Tesla at $6 per share (pre-split), held Amazon through a 30x run, was an early investor in SpaceX, and provided critical growth capital to Illumina, Shopify, and Moderna before the market understood what any of them were building. Their investment philosophy—identify transformational companies at key operational and cash flow inflection points, take concentrated positions, and hold through volatility—is among the most successful long-duration strategies in institutional asset management. This also describes what we aim to do at Crossroads in finding emerging compounders, the next cohort of unknown, exemplary businesses of today likely to become household names tomorrow.

At any rate, it’s important to know that Baillie Gifford was already a Merlin investor before the SPAC. They also participated in the PIPE and yet again when the PIPE was upsized from $125 million to over $200 million. At every turn they were among the existing investors who increased their commitment. A series of moves we see as signal more than noise. After all, the firm built its reputation on early-stage conviction in generational companies—and whose track record at doing so is essentially without peer. Ballie Gifford has looked at Merlin’s technology, contracts, and management team and decided to buy more. Not once or twice but many times over the years.

The PIPE structure itself tells us something important. At $12.00 per share for the additional commitment, these investors were paying a meaningful premium to the $10.39 trust redemption price—a price that implies they see substantial upside from here. This is not the behavior of investors looking for a quick flip. Rather, it’s what you’d expect of a firm that believes Merlin’s autonomous aviation platform might represent the same kind of category-defining opportunity they identified in Tesla’s autonomous driving ambitions or SpaceX’s reusable launch economics.

To be clear, we do not invoke Baillie Gifford’s presence as any type of authoritative proof Merlin will be a winner. Their involvement is hardly a guarantee of success and no investor is infallible, especially on a name where the range of outcomes is this wide. But their track record of identifying transformational technology companies at inflection points, combined with the fact that they increased their position during the PIPE upsizing rather than holding steady or trimming, is precisely the kind of institutional validation from smart money that should make serious investors take a harder look at what’s happening here. To say the same thing in a slightly different way, when the firm that saw Tesla, SpaceX, and Amazon before the market did decides to double down on an autonomous aviation play, it’s worth asking: what do they see that the rest of the market doesn’t?

Economic Logic and Installed‑Base Math

Merlin’s emerging moat is economic as much as it is technical. The company has over 800 military aircraft under contract across platforms like the C-130J and KC-135, embedding a path to roughly $1.6 billion of high-margin recurring AI-software revenue once integrations scale. Per management, each tail carries a $3 million one-time integration fee and $2 million in annual recurring licensing—implying $25-$35 million in lifetime value per airframe (10-15 years minimum life post integration) and an annuity flywheel that strengthens as the installed base ramps, and not to mention a nonexistent CAC thanks to the cost-plus integrations. An LTV/CAC ratio that would make any software company green with envy.

The retrofit model is central to this. Rather than selling new airframes, Merlin upgrades existing fleets, turning sunk capital in legacy aircraft into a software-monetized asset. For U.S. DoD customers, the economics are straightforward: if Merlin’s autonomy reliably replaces a second pilot or enables contested-environment capabilities that would otherwise be impossible, price sensitivity is low and the $2 million annual license is a rounding error relative to mission value. For civil cargo operators, where pilot costs run 11–25% of total opex, a credible single-pilot solution that delivers hard, auditable savings can support similar pricing.

What makes this flywheel credible is who has chosen to validate it. Honeywell, Northrop Grumman, and GE Aerospace have each entered formal partnership agreements with Merlin—not as passive observers, but as active integration partners embedding Merlin’s autonomy into their own flagship platforms. Honeywell’s October 2024 MOU integrates Merlin’s solutions with its Aerospace Technologies division for military aircraft retrofit. Northrop’s June 2025 agreement pilots Merlin as the platform to validate mission-autonomy software for future defense programs via Beacon, its flight operating system. Most significantly, GE Aerospace’s September 2025 integration links Merlin directly to its Flight Management System—the operating system of record for over 14,000 aircraft globally—beginning with replacement of obsolete cockpit components. These aren’t endorsements as much as hyper capital efficient distribution channels characterized by demand side network effects and increasing returns to scale.

Merlin’s contract structures amplify this leverage further. Initial programs are cost-plus, de-risking engineering spend during integration. As fleets transition to steady-state operations, those same contracts convert to fixed-fee licenses with attractive incremental margins as upfront R&D is leveraged across an expanding fleet. IDIQ language allows contract ceilings to be raised via administrative amendment rather than full re-bid, turning successful pilots into multi‑year revenue streams without repeated competitive knife fights. Layer on a regulatory moat—FAA module approval, SOI-2 certification in New Zealand, bilateral FAA/NZ arrangements—and Merlin’s combination of installed-base retrofit flywheel, Tier-1 partnerships, and a commanding lead on certification pathways begins to look more like structural advantage than transient edge.

Competitive Landscape

No competitor that we know of occupies the same position as Merlin. Shield AI ($6 billion private valuation, currently raising at $11–12 billion) builds AI-powered autonomy for drones via its Hivemind software—a complementary but fundamentally different product focused on small UAS and swarm operations, not manned/large-frame aircraft retrofit. Reliable Robotics is pursuing FAA-certifiable autonomy for commercial cargo aircraft (recently selected for the FAA’s eIPP program in Albuquerque and deploying a Cessna 208B for the Air Force in Guam) but operates at a fraction of Merlin’s scale and lacks the defense contract base. L3Harris has autonomous systems capabilities concentrated in maritime and flight termination, not full-spectrum manned aircraft autonomy. In our view, none of these competitors can replicate Merlin’s combination of: (1) a live, flying autonomy stack proven across five aircraft platforms, (2) $105M+ in prime defense contracts, (3) dual civil-defense certification in progress, and (4) partnerships with GE Aerospace and Northrop Grumman. The competitive moat is not one barrier but the compounding of all four.

Autonomous Flight vs. Driving: First Principles Differences and Why Merlin is Likely to Succeed

The difficulty of autonomy scales with the number of independent variables the system must handle simultaneously, and critically, with how those variables interact. In driving, that variable universe is enormous. There are dozens of uncoordinated actors with unknown intent. Road geometry changes with every construction zone. Localized surface hazards can be invisible to sensors until you're on top of them. Decision windows at two-meter separation distances are sub-second. And these variables are multiplicative. A pedestrian stepping off a curb during rain while an ambulance approaches from behind isn't three problems. It's one compound scenario drawn from a space of roughly 10^8 to 10^10 distinct edge cases. This is why full self-driving remains unsolved after two decades and tens of billions of dollars of R&D. The combinatorial explosion of the driving environment is, for all practical purposes, infinite.

Aviation is a structurally different problem, and the distinction is not one of degree but of kind. Every actor in the airspace is identified, transponding, and following published procedures under positive control. The geometry is fixed and three-dimensional with separation buffers measured in miles, not meters. Weather is volumetric and forecast hours in advance; you route around it rather than react to it at close range. Most importantly, altitude buys time. A system failure in cruise gives you minutes to diagnose and respond. The equivalent failure in urban driving gives you milliseconds. The result is an edge-case space roughly four orders of magnitude smaller than driving. To put that in perspective, the gap between these two problem spaces is roughly the same as the gap between the number of people in a small town and the population of the planet.

This is the structural insight the market is missing with Merlin. Investors pattern-match "autonomous aviation" to the Waymo and Cruise difficulty curve and assume a similarly long, capital-intensive slog to certification. But the problem Merlin is solving is categorically more tractable. The environment is cooperative by design. The failure modes are well-enumerated with published procedures. The physics give any autonomous system time to think. Aviation as it is structured and regulated in the modern era, was built for humans to follow rules in a structured, procedurally controlled airspace. That's precisely the kind of domain where autonomy excels. It’s why we’ve had autopilot solutions for decades while self-driving is still in its infancy. Merlin isn't trying to solve a harder version of self-driving. It's solving an easier problem in a domain whose engineering constraints were designed from the start to make automation possible, albeit with more rigorous qualification via the FAA et al. The market hasn't figured this out yet, and that's our opportunity.

Management Guidance: Is 2027 the Inflection to Escape Velocity?

We believe the revenue build management presents was purposefully non-promotional and stopped at 2026, the reasons for which are detailed above, ensure an informational asymmetry so as to own as much as Merlin as possible post de-SPAC.

Even still, Matt George has been explicit: Merlin’s near-term revenue trajectory is anchored to the C-130J and KC-135 programs, with 2025E revenue of ~$8.5 million and 2026E of ~$32 million—a 276% year-over-year growth rate driven by initial integration deliveries and early license payments. And beyond 2026, the company has guided to an identified pipeline of $3 billion, but management has declined to provide detailed year-by-year projections, again we point to the incentives above. Excluding that dynamic, the reasoning is sound: at this stage, the variables that drive 2027–2030+ revenue—the pace of fleet integration, the timing of civil certification, the conversion rate on pipeline opportunities—are dependent on execution and we believe the company wants to set good expectations to beat, rather than over-promise.

We respect that discipline. In our experience, founders who resist the temptation to project hockey-stick revenue five years out tend to be the ones who actually deliver it.

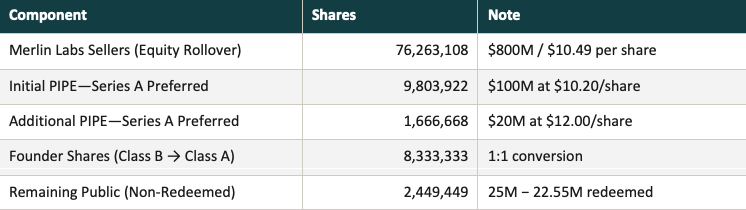

Post-Redemption Transaction Summary

Before wading into the scenario work, the post-redemption capital structure is critical context. Redemptions came in at 90.3%—an outcome that was better for all the pivotal players and clarifying for equity investors now that the business combination is behind them.

The resulting pro forma structure is lean, concentrated, and favorable to long-duration holders:

A few points worth emphasizing. First, the $146M in pro forma net cash provides meaningful runway and eliminates near-term dilution risk—Merlin doesn’t need to tap the market to fund operations through the critical 2026–2027 contract ramp. Second, the ~5M-share public float creates a supply/demand dynamic that, while volatile in the near term, should amplify any positive catalysts—contract wins, certification milestones, or institutional discovery—into disproportionate price action. Third, and most importantly for our purposes, Crossroads’ entry at $6.80 via the rights structure provides a structurally advantaged cost basis that offers meaningful downside cushion even in our Bear Case.

Pro Forma Share Count Breakdown

Warrant Overhang: ~11.05M total PIPE warrants at $12.00 exercise (with $5.00 floor reset provision). Fully diluted share count including warrants: ~112.1M shares.

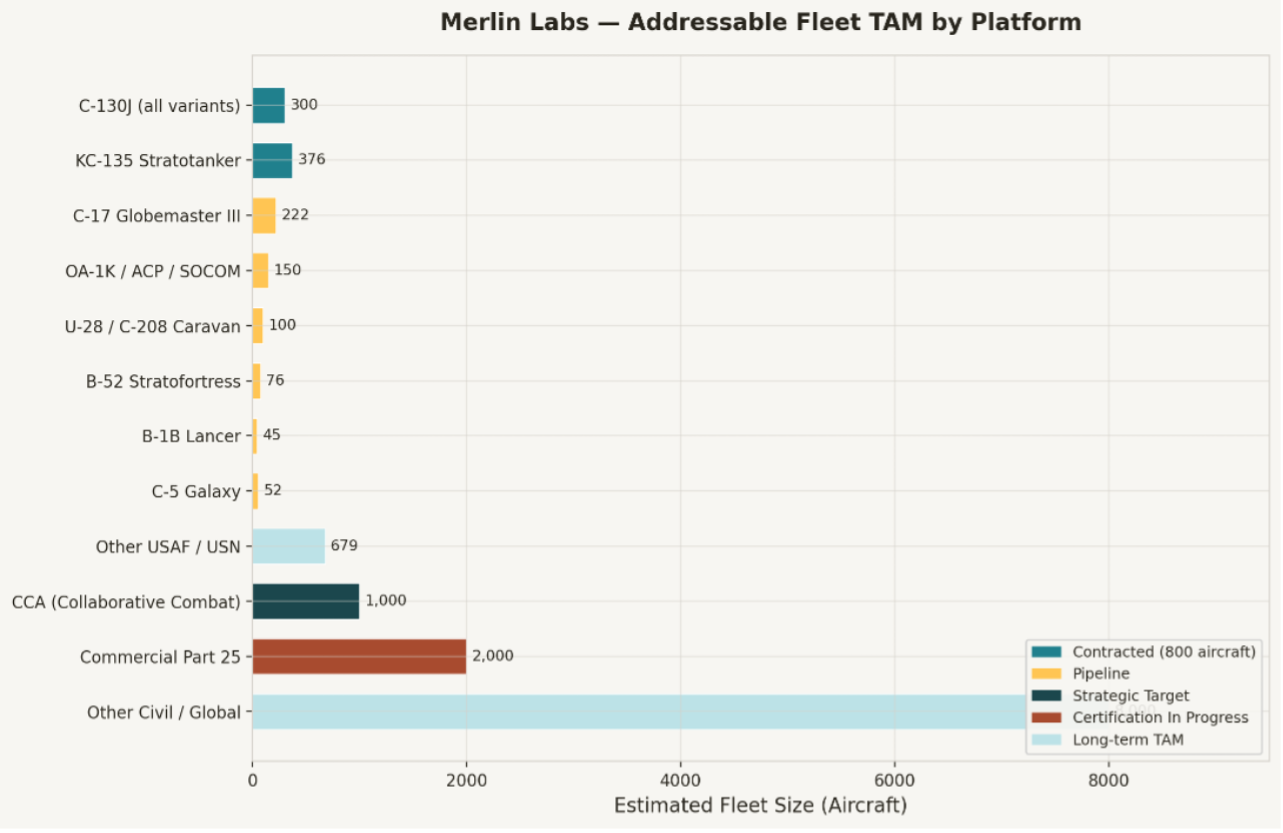

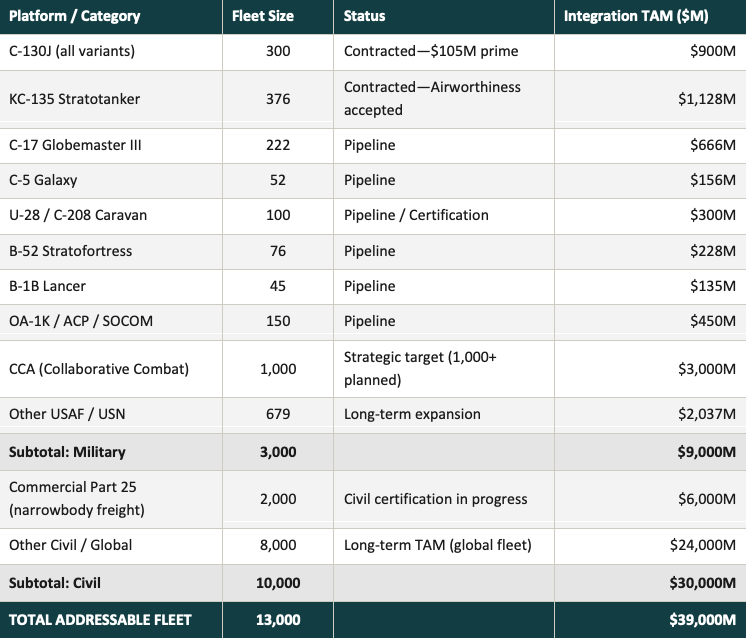

Addressable Fleet and Total Addressable Market

The breadth of Merlin’s addressable fleet is one of the most misunderstood aspects of the story. Most investors, to the extent they’ve ever heard of the company or done any work at all at this point, focus narrowly on the C-130J contract—the $105M sole-source prime that put Merlin on the map. But the installed-base opportunity extends far beyond a single airframe. As the chart below illustrates, Merlin’s TAM spans 13,000+ aircraft across military, strategic, and civil categories—a number that dwarfs the 800 tails currently under contract, underscoring the magnitude of the optionality embedded in this platform.

Fleet TAM Detail

The takeaway is straightforward: the ~800 aircraft currently under contract represent just 6% of the addressable military fleet and barely a rounding error on the total global opportunity. Every platform Merlin integrates with from here—the C-17, the B-52, the CCA program—is additive to the annuity base, and every civil certification milestone unlocks a market that is an order of magnitude larger than the defense beachhead that started it all. The $39 billion integration TAM figure above doesn’t even capture the annual recurring license revenue that follows—at $2M per tail per year, full penetration of the military fleet alone implies $6 billion in recurring annual revenue. Add civil, and you’re modeling a $26 billion annual revenue opportunity at maturity. These are not speculative numbers; they are the arithmetic consequence of known fleet sizes and Merlin’s stated pricing.

And here’s the thing about that $2M per tail per year: it’s an absolute bargain relative to the cost savings it delivers. Per management a single plane flying for the US military requires 14 pilots annually (7 per seat) at an approximate all in cost of $7mn per seat given the use of expensive third party contractors in lieu of the ongoing pilot shortage—meaning Merlin’s $3mn install fee and $2M license pays for itself in under a year on labor savings alone as the aircraft goes from two human pilots to one. This is before accounting for the operational value of GPS-denied capability, reduced mission-readiness bottlenecks from the labor shortage, and the ability to fly higher-tempo sortie schedules. For commercial cargo operators, where pilot costs run 11–25% of total opex, the math is even more compelling: SPO adoption on a fleet of 300+ mainline freighters translates to $2+ billion in aggregate savings against a Merlin licensing bill of $600M—a 3–4x return on spend, every year, in perpetuity after accounting for one-time hardware installation costs.

We repeat this is not a cost line-item customers will fight over; it’s a win-win of the first order—the kind of value proposition that we believe ensures not just rapid adoption, but tremendous pricing power for Merlin over the life of these contracts. A natural result when your product saves customers multiples of what you charge them.

Valuation

Merlin’s installed-base opportunity is vast and, in our view, profoundly underappreciated by a market that still reflexively applies the SPAC discount to everything that emerged through that channel. The company’s global TAM across USAF and Part 25 cargo fleets exceeds 13,000 aircraft—roughly 16x larger than the ~800-unit serviceable addressable market already locked in under existing DoD contracts. Per management guidance, each aircraft generates a $3M one-time integration fee (hardware and software installation) plus a $2M annual recurring license—if the average aircraft lives another 10 to 15 years, that’s a $25M to $35M lifetime value per tail and a clear path to $1.6 billion in annual recurring revenue at contracted-fleet maturity for just the C-130J and KC-135 programs already awarded.

Apply what we believe is a conservative 12.5x SaaS/defense EV multiple to that recurring stream alone and you arrive at a $20 billion+ terminal enterprise value—roughly 25x the $800M pre-money ascribed in the SPAC combination, and approximately 50x our rights-adjusted cost basis of $6.80 per share.

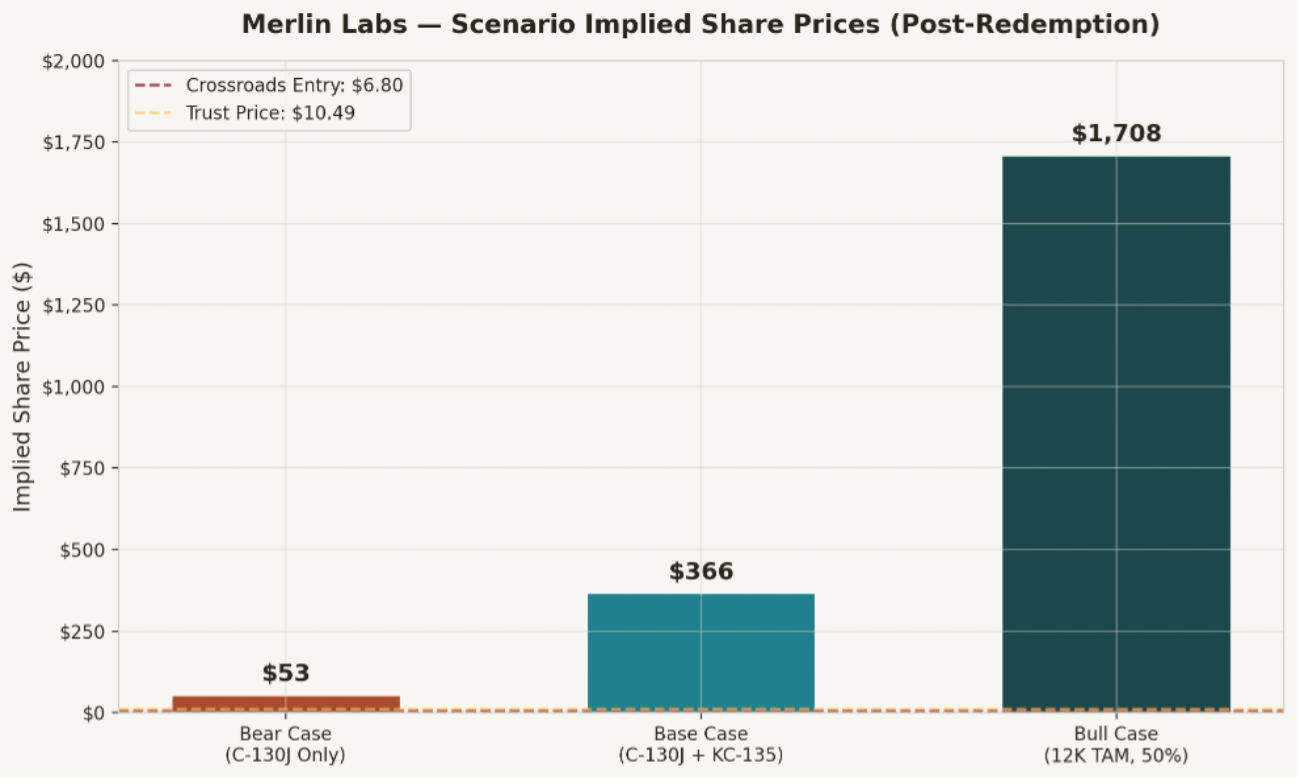

Putting this in context with our scenario framework: in a Bull Case where 12,000 aircraft at 50% adoption are served at a 12.5x sales multiple, you’re looking at over $1,000 per share. The Base Case—Merlin ramps on the existing 800 contracted aircraft (C-130J + KC-135), with no commercial TAM expansion—yields $350+ per share. Even the Bear Case—just the C-130J, taking longer than expected—puts you at $30–50 per share. Relative to our rights adjusted $6.80 entry, every scenario delivers meaningful upside. While we’ve yet to have a discussion with our Scottish peer, we believe Baillie sees the exact same math we do.

What follows is the full scenario framework, revenue build, sensitivity analysis, and peer comparables that underpin our conviction. We present this work not as a prediction of any single outcome, but as a disciplined attempt to bound the range of possibilities—and to quantify why we believe the current valuation gap constitutes a genuine margin of safety, despite what admittedly looks like expensive trailing-twelve-month math.

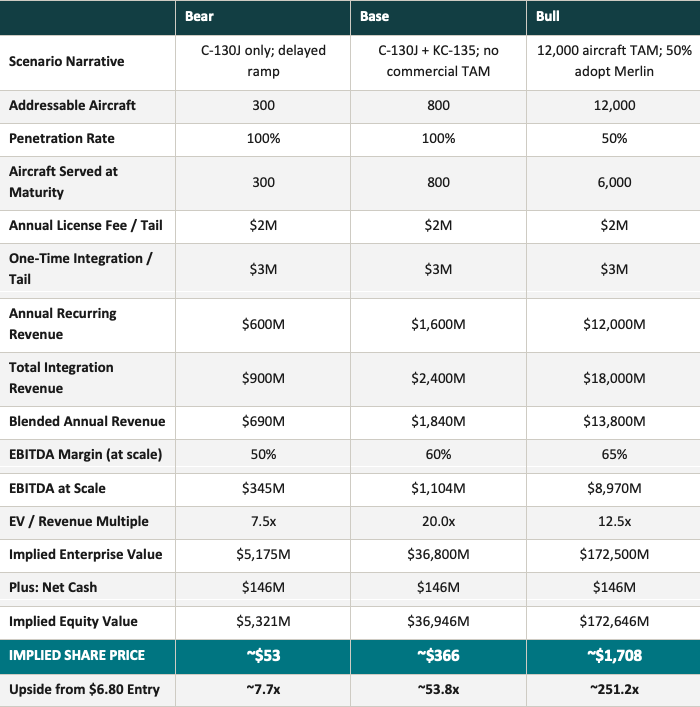

Scenario Valuation Framework

We model three scenarios to bound the range of outcomes, calibrated to different assumptions about fleet penetration, timeline, and the appropriate valuation multiple. Each scenario holds constant Merlin’s unit economics ($2M annual license + $3M one-time integration per tail) and the post-redemption capital structure (101.06M pro forma shares, $146M net cash). The only variables are how many aircraft, at what pace, and at what multiple the market capitalizes the resulting revenue stream.

Bear Case: C-130J Only, Delayed Ramp (~$53/share)

The Bear Case assumes Merlin executes on the existing C-130J contract (~300 aircraft) but fails to expand beyond that single platform—no KC-135 follow-on, no commercial certification, no pipeline conversion. The ramp is slower than management’s guidance, and the market assigns a compressed 7.5x EV/Revenue multiple reflecting execution skepticism. Even in this deliberately punitive scenario, the implied share price of ~$53 represents roughly 7.7x our $6.80 entry—a return profile that would be enviable for most investments, let alone a downside case. The key insight: the C-130J contract alone, at Merlin’s stated unit economics, generates $600M in annual recurring revenue at maturity. That’s real money, on a single platform, under a contract that already exists, with a single customer (Uncle Sam) with literally zero credit risk!

Base Case: C-130J + KC-135 Fleet (~$366/share)

Our Base Case assumes Merlin scales across both currently contracted platforms—the ~300 C-130Js and ~376 KC-135 Stratotankers, plus ~124 aircraft from the near-term pipeline (because we like big round numbers and precision is hardly necessary in an exercise like this one)—totaling 800 aircraft served at maturity with no commercial TAM expansion. We apply a 20x EV/Revenue multiple, reflecting Merlin’s SaaS-like margin profile, defense-anchored revenue visibility, a near endless high return reinvestment runway, and the scarcity premium the market has historically awarded to category-defining defense software. At $1.6 billion in annual recurring revenue and 60% EBITDA margins, this implies an enterprise value of ~$37 billion and a share price of ~$366—a 54x return from rights adjusted entry. We consider this the most probable outcome conditional on competent execution.

Bull Case: Full TAM Penetration (~$1,708/share)

The Bull Case models what happens if Merlin’s technology proves as transformative as we believe the early evidence suggests. We assume 12,000 aircraft across military and civil fleets, with 50% Merlin adoption—6,000 tails generating $12 billion in annual licensing revenue. Even at a relatively modest 12.5x EV/Revenue multiple (well below where Palantir, Aurora, or True Anomaly trade today), this implies a $172+ billion enterprise value and a share price exceeding $1,700—a 251x return from our cost basis. Is this aggressive? In absolute terms, certainly. But consider: Palantir trades at 105x revenue today; SpaceX conducted its most recent tender at $800 billion and is reportedly filing for an IPO targeting $1.75 trillion+; Waymo just raised $16 billion at a $126 billion valuation. If Merlin genuinely becomes the operating system for autonomous aviation—and the evidence increasingly suggests it could—the Bull Case may prove conservative in hindsight. And yes, that sentence was hard to write but we wrote it anyway as that’s where we believe the evidence points too.

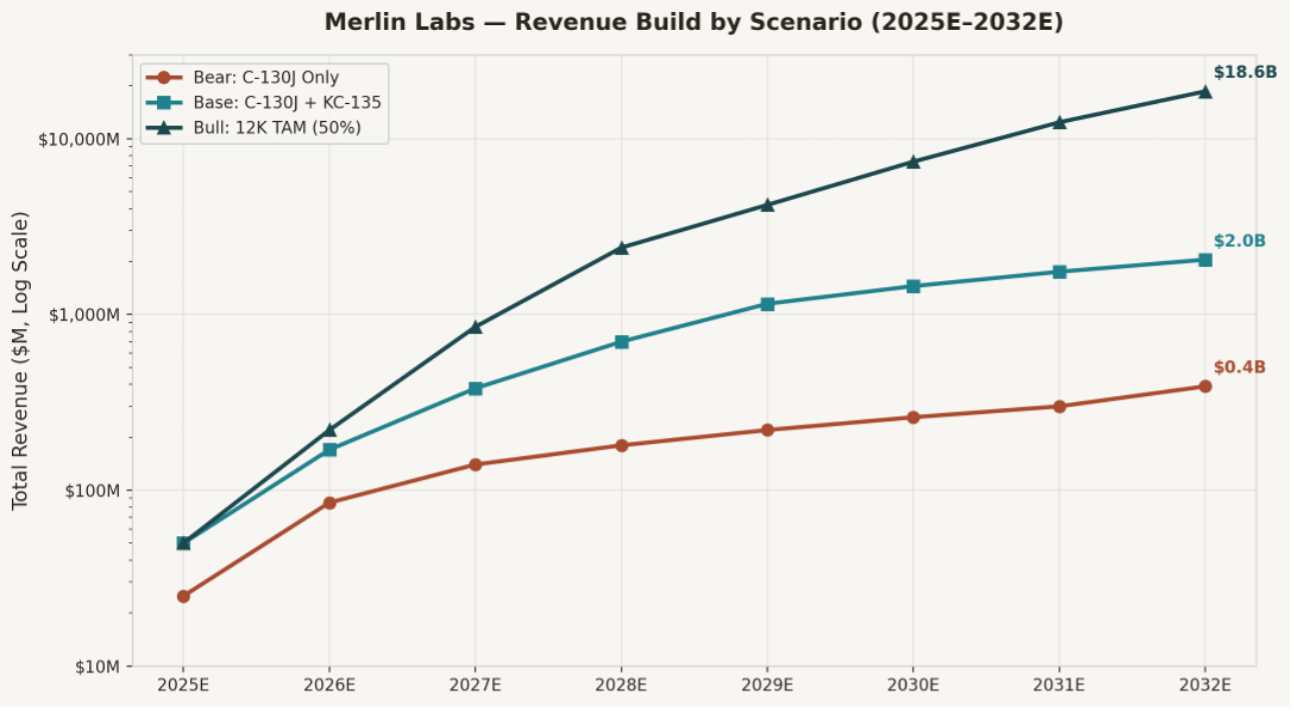

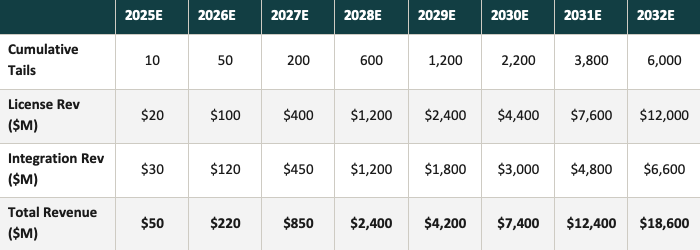

Revenue Build: 2025E–2032E

The estimated revenue ramp below traces the trajectory from Merlin’s current ~$8.5M revenue base to maturity-state revenue across all three scenarios. Note the logarithmic scale—the visual distance between scenarios understates the arithmetic divergence, which is the point. The difference between the Bear and Bull cases by 2032 is not 2x or 5x; it’s nearly 50x, driven entirely by fleet penetration. The unit economics are identical across all three.

Bear Case Revenue Build

Base Case Revenue Build

Bull Case Revenue Build

The revenue build underscores a critical feature of Merlin’s model: the compounding effect of the annuity. In the Base Case, integration revenue peaks around 2029E as the existing fleet is fully outfitted, but license revenue continues to climb as every installed tail pays $2M per year in perpetuity. By 2032E, licensing constitutes 78% of total revenue—a mix shift that drives margin expansion from the cost-plus early phase toward the 60%+ EBITDA margins we model at scale. This is the transition from “defense contractor” to the winner take most “defense autonomy platform” that the market is not yet pricing in.

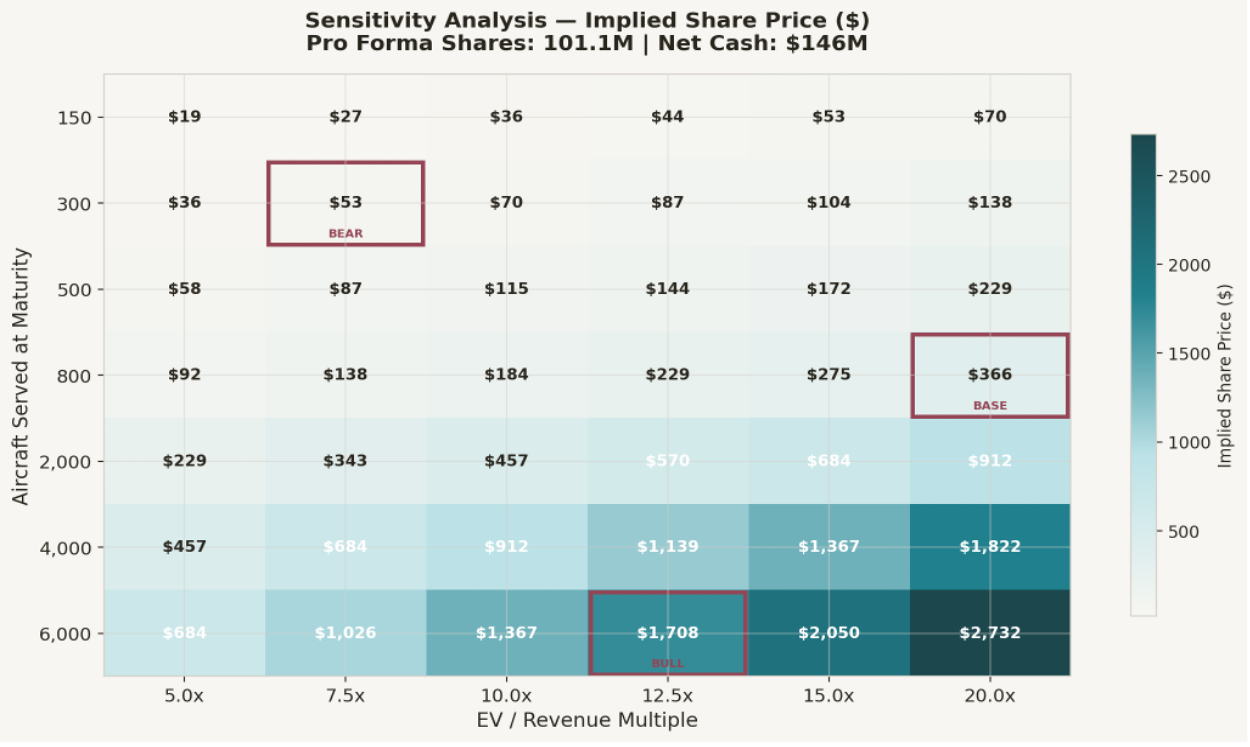

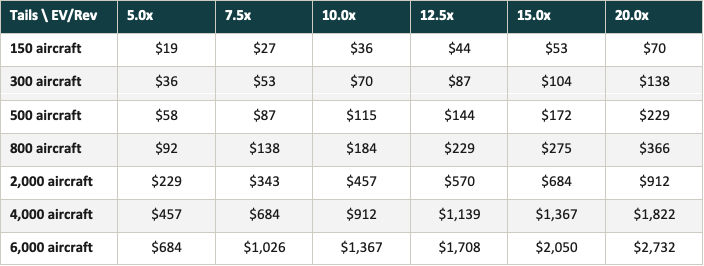

Sensitivity Analysis

The sensitivity matrix below maps implied share price across the two variables that matter most: the number of aircraft Merlin ultimately serves, and the EV/Revenue multiple the market assigns at maturity. Our three scenarios are highlighted. The takeaway is clear: at virtually any reasonable combination of fleet penetration and multiple, the implied value is a substantial premium to today’s price. The only path to a loss that we see from our $6.80 entry requires Merlin to serve fewer than 150 aircraft at a sub-5x multiple—a scenario that implies the complete failure of the C-130J program, the loss of the KC-135 contract, and a market valuation below distressed hardware companies. We do not consider this a realistic outcome.

ReferencePoints: Crossroads entry at $6.80 | Trust redemption at $10.49 | BearCase: 300 tails @ 7.5x = ~$53 | Base Case: 800 tails @ 20x = ~$366 | Bull Case:6,000 tails @ 12.5x = ~$1,708

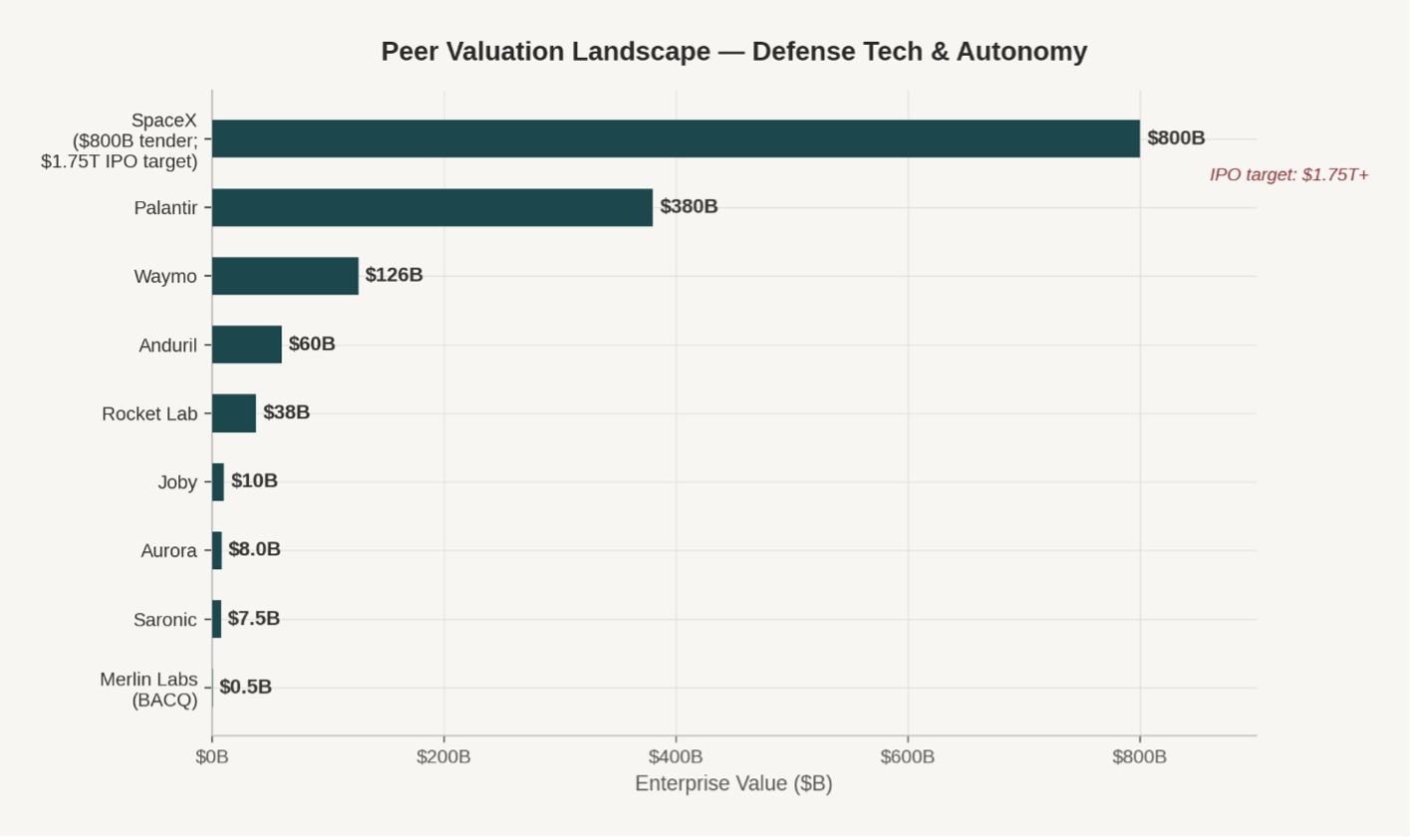

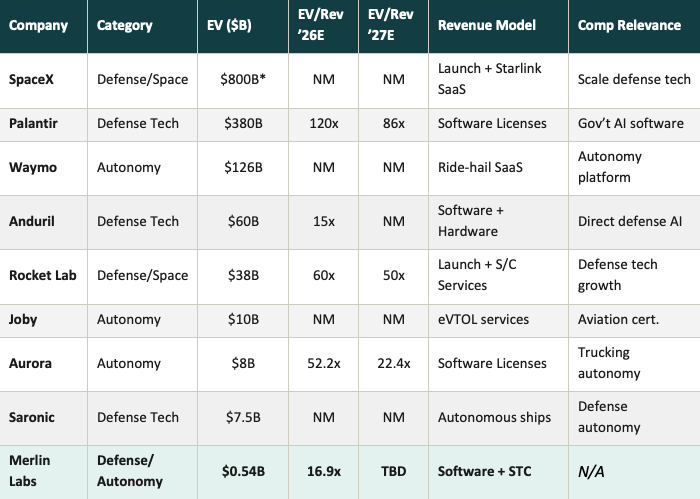

Peer Valuation Comparables

Merlin’s valuation cannot be understood in isolation—it must be contextualized and sense checked against the broader defense tech and autonomy universe. The chart and table below position Merlin against public and private peers across these categories. The contrast is stark: at $541M implied EV (our rights adjusted cost basis), Merlin trades at roughly 1/111th the valuation of Anduril, 1/700th of Palantir, and 1/3,000th of SpaceX’s reported IPO target—despite operating in the same defense AI ecosystem, serving many of the same DoD customers, and targeting a TAM that is arguably larger than any of them on a per-unit economic basis. Even Waymo, a pure autonomy play with no defense revenue and no recurring software licenses, just raised at $126 billion—roughly 230x Merlin’s current implied EV.

* SpaceX: $800B December 2025 tender offer; IPO filing reportedly targeting $1.75T+ (Bloomberg, Feb 2026). Waymo: $126B post-money per $16B raise led by Dragoneer/DST Global/Sequoia (Feb 2026). NM = Not Meaningful (pre-revenue or EV/Rev > 90x). Source: S&P Capital IQ, AlphaSense SEC filings, Merlin Public Presentation Nov 2025. Updated March 2026.

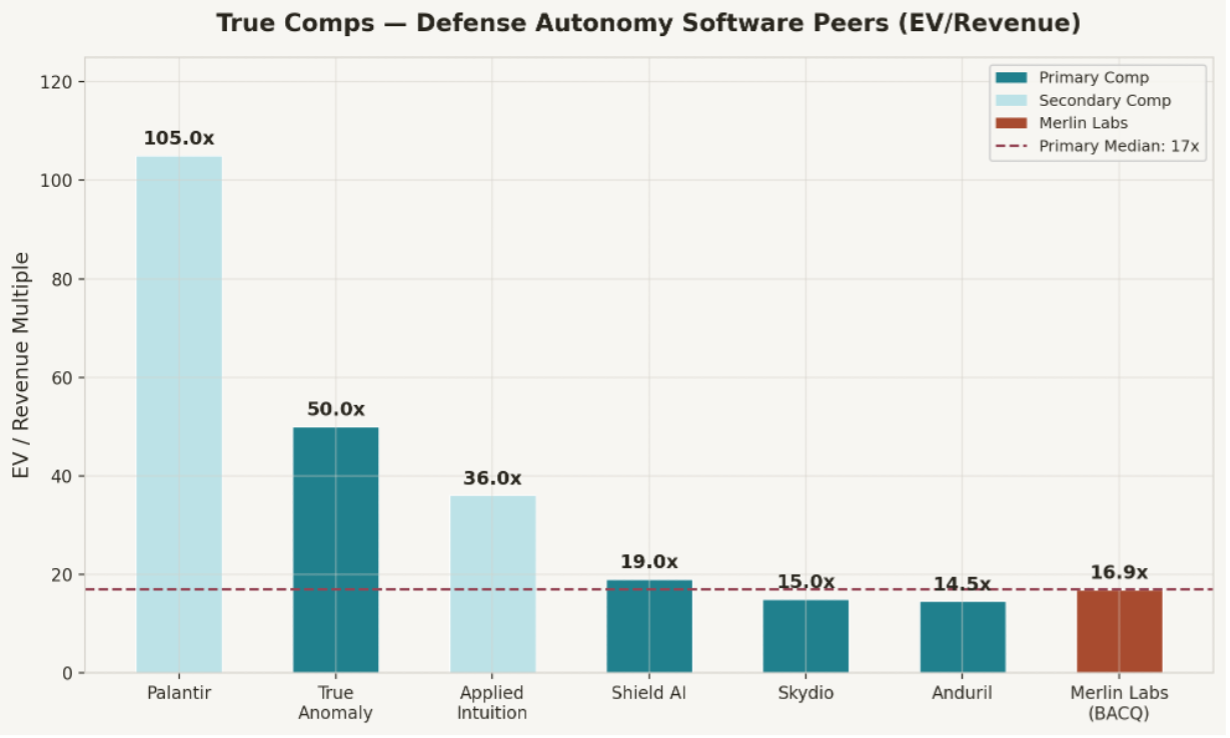

True Comps: Defense Autonomy Software Peers

The broad peer set above, while useful for context, conflates hardware-intensive businesses with pure-play autonomy software. To isolate the most relevant comparisons—companies that match Merlin on core product (autonomy/AI pilots), customer base (DoD), and growth stage—we constructed the “True Comps” set below. These are the companies building AI-driven autonomous systems for military platforms, the cohort against which Merlin’s valuation should ultimately be benchmarked.

Comp Multiple Summary

At 16.9x EV/Revenue, Merlin trades roughly in line with the primary comp median of ~17x—a positioning that appears reasonable at first glance until you consider what it implies. Anduril at 14.5x is a $30.5 billion business generating $2.1 billion in revenue at 40–45% gross margins on a capital-intensive hardware model. Merlin at 16.9x is a $541 million business generating $32 million in revenue this year—but with a path to $1.6 billion in software-only recurring revenue at SaaS-like margins, on contracts that already exist. So while the multiple is similar; the growth trajectory and margin profile are categorically different. SpaceX is targeting a $1.75 trillion IPO on the back of Starlink’s recurring revenue model; Waymo just raised at $126 billion without a single dollar of recurring software licensing. In a market where private SaaS companies with strong retention command median EBITDA multiples north of 22x, and infrastructure software reaches 24–36x, Merlin’s current valuation is not just cheap—it may be the cheapest equity relative to its normalized earnings capacity we’ve ever seen. If management can deliver on basic blocking and tackling, today’s equity valuation will appear downright crazy in hindsight. That’s a big if, but it’s worth highlighting.

Implied Merlin Share Price at Comp Multiples

Note: The above table uses 2026E revenue of $32M and current implied EV of $541M. As Merlin executes through 2026–2027 and revenue scales toward $170M+ (Base Case), the relevant comparison shifts from current-year multiples to forward revenue, at which point the discount to peers becomes even more pronounced.

Key Assumptions and Sources:

• Fleet sizes from WDMMA and Merlin Investor Presentation (Nov 2025)

• $2M/year license + $3M one-time integration per tail (Merlin deck, p.20)

• Bull case: 12,000 aircraft = ~5,000 USAF + ~2,000 commercial Part 25 + ~5,000 global fleet expansion

• Base case: 800 aircraft = ~300 C-130J + ~376 KC-135 + ~124 near-term pipeline

• Bear case: C-130J fleet only (~300 aircraft), 100% penetration, delayed timeline

• EV/Revenue multiples: Peer comps—Rocket Lab 11.2x, Palantir 33.7x, Aurora 52.2x, Joby 71.2x

• Pro forma net cash of ~$146M post-90.3% redemptions

• Integration revenue amortized over 10-year useful life for blended annual revenue

• Crossroads entry at $6.80/share via BACQR ($0.68/right, 10:1 ratio)

• SpaceX: $800B tender offer (Dec 2025, Bloomberg/WSJ); IPO confidential filing targeting $1.75T+ (Bloomberg, Feb 27, 2026)

• Waymo: $126B post-money valuation per $16B raise led by Dragoneer, DST Global, Sequoia Capital (Waymo blog, Feb 2, 2026; Reuters, CNBC)

• True Comps sources: Shield AI ($5.6B Series F-1, Bloomberg Feb 2026); Anduril ($30.5B Series G, Reuters Mar 2026); Skydio ($4.2–4.5B Series F, Feb 2026); True Anomaly (~$1.5B Series C, Apr 2025); Applied Intuition ($15B Series F, Jun 2025); Palantir (EV ~$325B, public market, Mar 2026)

• Source: AlphaSense SEC Filings, S&P Capital IQ, Merlin Public Presentation, filed March 12, 2026

Variant Perception: What the Market Gets Wrong

Every asymmetric investment begins with a divergence between consensus and reality. It follows that if the market correctly priced Merlin, there would be no opportunity. The edge here is not so much informational, as every data point in this thesis is publicly available. The edge is interpretation.

Keep in mind SPACs represent one of the many unloved and underfollowed pockets of the market, a pocket that has been a source of profit for Crossroads since the inception of the fund.

Joel Greenblatt, Micheal Blizter’s mentor and one of our investing heroes, describes four key traits for an attractive “special situation” investment, and we think Merlin, via its upcoming transaction with BACQ checks every box. A defined catalyst is required (a Q1/2026 merger in the case of Merlin). Layer in complexity or neglect, management incentives that are aligned with value creation for shareholders, and last but certainly not least, limited downside, and we were able to get there pretty quick.

Regardless, offering a faster (and less stringent) go-public process, SPACs lend themselves to speculative business models, promotional management teams, and sponsors looking to make a quick buck. SPACs also tend to largely surface in boom times, creating a high degree of sensitivity to market timing and sentiment.

So, for all the reasons listed above, combined with nuanced deal structures and merger subtleties, SPACs are neglected by the majority of investors and remain an asset class predisposed to the ‘baby being thrown out with the bathwater’. This creates a perpetual series of opportunities for those willing to turn over a lot of rocks as even the vast majority of shareholders view SPACs as nothing more than an enhanced cash proxy to hold until it’s time to redeem once the merger in question comes up for a vote. The reality is fundamental-oriented investors committing capital ahead of the completed merger as a precursor to the underlying business being acquired are increasingly rare.

Switching gears back to our edge being interpretation…

Consensus says: BACQR is another high-redemption de-SPAC with speculative, pre-revenue exposure to an autonomous drone/defense story. The playbook is familiar—apply the SPAC discount, assume execution risk is unhedgeable, and move on. The rights are option-like instruments that will trade around trust value with binary outcomes tied to deal close – and like we mentioned earlier on, ~90% of SPACs in recent years don’t ultimately reach the finish line.

We say: Merlin is not a drone company, and this is not a speculative pre-revenue bet. It is a first-principles digital pilot platform with a retrofit-driven, defense-anchored annuity model—one that is already flying on five aircraft platforms with $105M+ in prime defense contracts, a live GE Aerospace Program of Record, and a regulatory pathway that is years ahead of any competitor. In this case, the rights structure, pre-funded capital stack, and sponsor alignment created unusually strong closing odds—odds that have now been realized. As far as the unhedged position we continue to hold, at our entry economics, we are paying a fraction of where clearly inferior autonomy stories already trade on EV/Revenue.

The mispricing persists because the market barely even knows it exists and investors that are aware are likely applying a categorical heuristic—“SPAC = junk”—to a company that was specifically engineered to be the exception to the rule. Matt George waited seven years to bring this public. Baillie Gifford increased their position through the PIPE. Blitzer committed $100M of his own fund’s capital. The 90.3% redemption rate, which consensus reads as a red flag, is actually the mechanism that concentrated the cap table into the hands of the most informed, longest-duration holders, ensuring they would walk away from the IPO with more ownership, not less. From what we’ve been able to gather, the market sees the SPAC wrapper and pattern-matches to the last hundred de-SPACs that cratered. We see a founder-led, defense-anchored software platform entering the public market at 16.9x 2026E revenue—a trough-year on a business with a line of sight to growing revenue 50-fold over the next three to five years.

Peter Lynch once advised investors to “search for promising stocks that are overlooked by most fund managers, where their market cap is too low to qualify for their funds—once these stocks rise in price, so does their market cap, and only then do bigger funds invest in them.” Merlin is precisely that situation. That divergence between what the market sees and what actually exists is the entire thesis. When the market re-rates Merlin from “another SPAC” to “leading defense autonomy platform with contracted recurring revenue and a right-to-win,” the repricing will not be incremental. With ~5 million shares of public float and a cap table dominated by locked-up insiders, even modest institutional discovery will produce outsized price action.

Risk Management and Position Monitoring

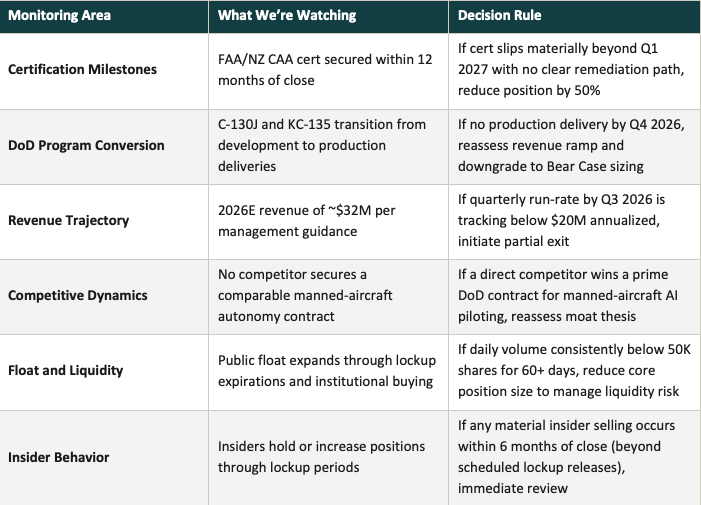

Conviction without discipline is speculation. We sized this position with high confidence in the thesis, but we also pre-committed to a set of decision rules that govern how we manage it from here as is par for the course at Crossroads. The framework below defines our key risks, the specific triggers we are monitoring, and the actions we will likely take if the thesis breaks.

Certification and Execution Risk. Merlin’s revenue trajectory is gated by FAA/NZ CAA certification milestones and the conversion of DoD programs from development to production. If the FAA dual-track pathway stalls, or if the C-130J and KC-135 integrations encounter material technical delays, the 2026–2027 revenue ramp could compress significantly. We believe this is the single most consequential risk to the thesis today.

Competition. Shield AI ($5.6B), Anduril ($30.5B), Skydio ($4.3B), and Reliable Robotics are all well-funded and technically capable. While none currently replicates Merlin’s combination of manned-aircraft autonomy, defense-grade certification, and retrofit economics, the defense AI landscape is moving fast. A competitor securing a major manned-aircraft autonomy contract would erode Merlin’s first-mover advantage and force a reassessment of the Base Case multiple and the position more generally.

Market Structure and Liquidity. The ~5 million share public float is a double-edged sword. On the upside, it amplifies positive catalysts into disproportionate price action. On the downside, it creates vulnerability to forced selling, short squeezes, and dislocations that have nothing to do with fundamentals. Post-de-SPAC trading dynamics can be erratic, and we must be prepared for downside volatility that comes with that should management get put in the dreaded deSPAC penalty box.

Customer Concentration. At present, Merlin’s revenue is concentrated in a single customer: the U.S. Department of Defense. While DoD credit risk is effectively zero, programmatic risk is not—budget reprioritizations, sequestration, or a shift in autonomy doctrine could delay or reduce contract execution. Diversification into civil cargo (via FAA certification) is the natural hedge, but that remains ahead, not behind.

Monitoring Plan and Decision Rules

We have defined a set of specific, observable triggers that will help us govern position management. We will use this as a guide; these are not hard rules:

The framework above is designed to keep us honest. The thesis is high-conviction, but conviction must be earned continuously—not assumed in perpetuity. If the milestones hit, we expect to be adding to the position, not managing it down. But if they don’t, the decision rules will help us to act on evidence rather than hope.

Conclusion

This is not a SPAC trade or a momentum play. This is a thesis built on structural mispricing—the kind that emerges when a category-defining technology company enters the public market through a channel the market has learned to reflexively dismiss.

We believe Merlin Labs is building the underlying operating system of record for autonomous aviation. Again, the technology is not theoretical—it is flying today, on five aircraft platforms, with a GE Aerospace Program of Record designation, a $105 million sole-source prime contract with USSOCOM, and a regulatory pathway (SOI-2 certification in New Zealand, bilateral FAA route) that is years ahead of any competitor. The installed base of 800+ contracted aircraft, at $3 million integration plus $2 million per year in recurring licensing, provides a clear and defensible path to billions in annual recurring revenue on existing contracts awarded from Uncle Sam.

Recent insider behavior confirms the thesis. Baillie Gifford—the firm that backed Tesla, SpaceX, and Amazon at inflection points—increased their position during the PIPE upsizing. Michael Blitzer, a Joel Greenblatt protégé who built a multi-billion-dollar firm on identifying asymmetric risk-rewards, structured the deal and called Merlin “a national asset.” Pre IPO Merlin equity holders haven’t sold a share and recently bought more ten seconds to price discovery, doubling down once more after several hugely positive incremental announcements that would have sent the equity soaring if this new issue had been properly marketed pre-IPO.

Finally, the valuation gap identified is real. At our $541 million implied enterprise value, Merlin trades at 1/56th the valuation of Anduril, 1/45th of Palantir, and 1/1,500th of SpaceX’s reported IPO target. The peer comps say the stock should re-rate meaningfully on near-term numbers alone. The terminal value—$20 billion+ at contracted-fleet maturity—says the near-term numbers barely scratch the surface of what this company will earn in the fullness of time. Do we need to say more?

From our $6.80 entry via the rights structure, the asymmetry on tap at Merlin is extraordinary. The Bear Case—C-130J only, delayed ramp, compressed multiple—delivers $30–50 per share. The Base Case—existing contracts executed—delivers $350+ per share. The Bull Case—full TAM penetration at 12,000 aircraft and 50% adoption—exceeds $1,700 per share. There is no scenario we can credibly model that produces a loss from this entry point if management executes even a fraction as well as it has thus far.

We sized this position with conviction because the setup demanded it. The arbitrage leg has now unwound, leaving us with a core position we will flex up or down based on execution. Thankfully the technology is real. The contracts are signed. The insiders are buying. The market has barely noticed. All is quiet—for now. When the cadence of promotion begins in the coming weeks, we doubt the repricing will be gradual; with a roughly 5‑million‑share public float, price discovery is likely to be sharp and one‑directional if management performs.

As James Anderson of Baillie Gifford put it on the OMD Daily Podcast from 2020:[2]

“The asymmetric payoff structure—you can make far more if you're right about a stock than you can lose if you're wrong—is the fundamental attraction of investing in equity markets.” — James Anderson, Baillie Gifford

In a world where pilot scarcity, GPS‑denied environments, and budget pressure are converging, Merlin is effectively asking investors to imagine aviation “without roads”—not by inventing new airframes, but by turning thousands of existing ones into software‑defined assets. For our money, there is no other AI or autonomy company as uniquely positioned as a business, or as asymmetric as an investment, as Merlin is today.

Best,

Ryan O’Connor

Crossroads Capital, LLC

Disclaimers

+ No guarantee of investment performance

Past performance of the financial instruments mentioned in this report should not be taken as an indication or guarantee of future results. The price, value of, and income from, any of the financial instruments mentioned in this report can rise as well as fall and may be affected by changes in economic, financial and political factors. Any projections, market outlooks or estimates in this presentation are forward looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect their returns or performance. Any projections, outlooks, or assumptions should not be construed to be indicative of the actual events that will occur. Future returns are not guaranteed. If a financial instrument is denominated in a currency other than the investor's home currency, a change in exchange rates may adversely affect the price of, value of, or income derived from that financial instrument. In addition, investors in securities such as ADRs, whose values are affected by the currency of the underlying security, effectively assume currency risk.

+ No guarantee of accuracy

While the information prepared in this document is believed to be accurate, Crossroads Capital, LLC (the “Investment Manager”) makes no representation or warranty as to the completeness, accuracy or timeliness of such information. The Fund and the Investment Manager expressly disclaim all liability for errors or omissions in, or the misuse or misinterpretation of, any information contained herein.

+ No obligation to update or act on information

The Investment Manager has no obligation to update any information contained herein, and may make investment decisions that are inconsistent with the views expressed herein. Any holdings of securities discussed herein are under periodic review and are subject to change at any time, without notice.

+ Not a recommendation to buy or sell any security

This report does not provide investment recommendations specific to individual investors. As such, the financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisions based upon their specific objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider this report as only a single factor in making an investment decision. All information provided is for informational purposes only and should not be deemed as investment or other professional advice or a recommendation to purchase or sell any specific security.

+ Not an offer to invest in our Fund

This report, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy limited partnership interests of Crossroads Capital Investment Partners, LP (the “Fund”) which may only be made at the time a qualified offeree receives a confidential private offering memorandum (“CPOM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the CPOM, the CPOM shall control. The interests shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution.

+ Other disclaimers

All trade names, trademarks, and service marks herein are the property of their respective owners, who retain all proprietary rights over their use. This document is confidential and may not be disseminated or reproduced without the prior written consent of the Investment Manager.