Mispricings

As Crossroads hits a decade of searching for value in public markets, we thought it worthwhile to continue the conversation we began last summer when we discussed our understanding of value (linked here). In brief, our view is that value is dynamic, perhaps better described as organic, and is continuously developing inside the evolving complex markets that remain our hunting ground. In that earlier note, we focused on the directional orientation of valuation. There is backward-looking valuation, driven by metrics and Fama-French categories that characterize the stereotypical “value” investor, and then there is forward-looking valuation, in which businesses are evaluated relative to their normalized earnings power a few years out. Typically the latter is where the real money is made, because the gap between what a business looks like today and what it will look like at a normalized run rate is precisely where the market’s pricing machinery breaks down.

On that note, we’ve often placed our positions into one of two categories: emerging compounders and special situations. But ultimately, value is found in market mispricings, not in the categorical groupings themselves. Recall that the goal of fundamental investing is to pay a price for a stake in a business that is less than its true value in the expectation that price and value will converge, earning an excess return as the gap closes. For that reason, understanding why mispricings emerge and when they can be taken advantage of is the foundation of our ongoing search for value.

There are three general types of mispricings, and in each one human psychology does most of the heavy lifting. Below, we look at each type in turn.

The Three Types of Mispricing

Duration Mispricing

The first type is what we'll call duration mispricing. It’s created by the short-term incentive structures that govern institutional capital: Performance is measured in months, fees are paid against benchmarks reset annually, and careers are made and lost on the next print. The result is a profession whose participants cannot afford to be early even when they’re right. Blaise Pascal wrote in 1670 that “all of humanity's problems stem from man's inability to sit quietly in a room alone.” That line describes the modern institutional investor with uncomfortable precision: all portfolio managers’ miseries derive from their being unable to leave their best positions alone. The asset management profession is structurally designed to prevent exactly the behavior most likely to produce strong returns.

Warren Buffett described the flip side of Pascal’s idea at the 1998 Berkshire annual meeting: “We don't get paid for activity, just for being right. As to how long we’ll wait, we’ll wait indefinitely.” Clearly, Buffett had no problem sitting quietly and letting his investment theses play out. Indeed, Buffett noted in a 1999 BusinessWeek interview that investing success does not correlate with raw intelligence above a modest baseline; instead, it correlates to temperament, specifically the capacity to resist the urges that get other people into trouble.

Buffett’s distinction reframes the entire investing skill set. The binding constraint on returns is not analytical horsepower, but behavioral discipline under conditions that punish that very same discipline in the short run. The investors who blow up are very rarely the dumb ones. Instead, they’re often the bright ones who could not “sit quietly in a room alone” and felt compelled to “improve” a system that did not need improving. Long-Term Capital Management later that decade provide two well-documented case studies of exactly that pathology: extraordinary intellectual firepower, working machines that produced spectacular risk-adjusted returns on autopilot, and then a fatal urge to extract more by fiddling with the very mechanisms that were already working.

In the fight between waiting and wanting, wanting almost always prevails. Incentives form desires, and short-term reward structures hijack the nervous system, producing the stress, anxiety, and emotional irritability that drive bad decisions. Our perception of time also stretches when our wants are forced to wait, and in a culture engineered for instant gratification, the willingness to wait is continuously diminishing. Patience, in our experience, is less an absence of action than what one surgeon described as “staying focused on what matters, even when it takes time.” It can be incredibly difficult to follow the advice of the famous old quip, “Don't just do something—stand there!”

That is duration mispricing in one sentence. Pod shops and benchmark-tethered allocators cannot stand there, so they trade. We can stand there, so we upgrade while we wait. Our patience has been well rewarded since we started Crossroads in 2016, and we believe it will continue to be.

With that in mind, we have continued to see a duration mispricing play out with Nintendo, as pod shops, representing the bulk of institutional capital in the market today, have been unable to look through the perceived near-term headwinds surrounding rising memory input prices, despite it being negligible to both COGS and margins. We think the ongoing structural change in the memory complex is actually a tailwind to Nintendo’s business. We’ll leave the details for a standalone piece, but with Switch 2 competitors substantially more exposed and large quantities of inventory already on hand at Nintendo, these investors simply don’t have the luxury of time to wait for this incorrect view to reverse course. Given that we first invested in the company in 2018, we remain patiently waiting for the market to recognize Nintendo as an economic juggernaut that continues to upgrade its revenue base and increase its incremental margins. And even better, it gives us a high degree of optionality and downside protection while we wait.

Diagnosing a duration mispricing is the easy part. Exploiting one requires a deliberate operating architecture, because the same human wiring that leads other market participants to produce the mispricing also tempts us to accept it as legitimate. Buffett and Munger spent six decades engineering around this problem, and three habits from their record stand out. We’ve tried to implement versions of all three at Crossroads:

The first is timing the search to the cycle. Buffett did not run his idea-screening process continuously at the same intensity. He ran it cold during expensive markets and hot during cheap ones. He terminated his partnership in 1970 and made effectively no public-market investments until 1974, by which point the S&P 500 P/E had compressed from 20 to 7 and he was selling stocks bought recently at three times earnings to buy stocks selling at two times earnings. He repeated the pattern from 1984 to 1987: not a single new equity position added to the Berkshire portfolio across that stretch, sitting on a mountain of cash, doing nothing. Then in the second half of 1987 he deployed over a billion dollars (roughly 25% of Berkshire's book value) into a single non-controlled position in Coca-Cola. The biggest bets came out of the longest waits. The pairing is not coincidental. Waiting is what made the size of the eventual bet defensible.

The second is redirecting intellectual energy into channels where the activity cannot damage the main book. Buffett did not suppress his analytical hunger during the dry stretches. Instead, he transferred that focus and energy into a variety of separate but adjacent interests: Smaller special situations in his personal account that were too small to matter at Berkshire scale. Buying distressed corporate bonds when equities ran rich (over a billion dollars of Finova bonds at deep discounts in 2001). Dabbling in REITs, silver, or asset classes entirely outside the space in which impatience could hurt his partners. Combined with hobbies that absorb intellectual energy outside of markets entirely (bridge for Buffett, omnivorous cross-disciplinary reading for Munger), this architecture is one of deliberately constructed sandboxes for the restlessness that investors can’t will away. The right question is not how to be less curious, but rather where can curiosity be expressed without compromising the discipline that matters?

The third is building an adversarial second filter into the process. Buffett would screen an idea, get past his own evaluation, and then run it past Munger, whose job was specifically to find the flaw and shoot the idea down. Most ideas died there. The ones that survived both filters were, by construction, the no-brainers: what Buffett called “waiting for the phone to ring.” The architecture is adversarial on purpose. It’s much easier for two independent thinkers operating in sequence to kill a bad idea than for one thinker to talk himself out of an idea he’s already partway sold on. We’ve worked to build the same internal dynamic at Crossroads in a way that matches our scale, because the alternative (a single decision-maker increasingly persuaded by his own analysis) is the most expensive failure mode in this business. As PM, the buck stops with yours truly, but letting a devil’s advocate put up roadblocks to prevent mistakes is always a good way of preventing poor judgment in a business where judgment is everything.

Taken together, those three habits point to something beyond Pascal’s maxim: Sitting quietly in a room alone is not a passive state. It’s an actively maintained one, supported by deliberate structure. The investors who succeed at doing nothing for years at a time are not the ones with the least intellectual energy, but rather the ones who have engineered the most disciplined places for its use.

Framework Mispricing

The second type of mispricing is framework mispricing. Market participants are trained to process new information; they are not trained to question whether the framework through which they’re processing it is appropriate. The result is that genuinely new business architectures get evaluated against templates that don’t fit them, and the gap between what the business has become and what the market is willing to call it can persist for years.

While Nintendo fits this category in its own way, our investment in AST SpaceMobile very much remains a framework mispricing in our view: Investors continue to project an outdated and generic mental model onto the space sector, considering it to be an uninvestable wasteland. Layer on the SPAC element, the direct competition with Elon, and the fact that ASTS has been pre-revenue with active ATM programs for much of its public history, and you have ample ingredients for a setup where investors will take years to overcome their cognitive biases. Underneath that framework is a business and management team we believe will ultimately prove the company to be worth many multiples of where it is valued today. In other words, we see ample evidence that AST will emerge as a business of unquestionable quality, backed by numerous moats and a visionary management team, and that it remains grotesquely mispriced by any reasonable measure of its future earnings capacity. In short, the mispricing is due to the framework, not the facts.

Business Transformation Mispricing

A third form of mispricing comes from business transformations. These are situations in which value-unlocking change, driven by structural factors, is overlooked by the market. Markets are pricing engines built for continuity. They extrapolate what a business is worth today into what it will be worth tomorrow. Naturally, when a company transforms internally or its industry restructures around it, the financial data lag reality: earnings reflect the old model, analyst frameworks anchor to historical relationships, and the shareholder base was selected for a company that no longer exists. The bigger the change, the wider the gap—and the longer the gap persists, because the investors who own the stock are often the last ones to recognize what the company is becoming. Crossroads targets this window explicitly, whether the discontinuity originates inside the company or is imposed from outside, and uses the change itself as the resolution mechanism.

Our investment in FTAI aims to exploit that company’s ongoing business transformation: FTAI originally spun out from a conglomerate of industrial transportation assets before evolving into a pure-play aviation platform in 2022. Having started as a conventional jet engine lessor, it continues to advance its vertically integrated economic model with an overlooked pricing engine (bad pun intended), which allowed it to create a novel, nimble, and flexible approach to creating value in an industry predisposed to inertia. More recently, FTAI has begun to replace its invested capital with third-party partners, advancing the business into an asset-light, fee-bearing model. For its next act, FTAI plans to leverage its existing competitive advantages to convert end-of-life engines into 25MW turbines, a material opportunity not reflected in present financial performance. The structural change is real, and the financial disclosures have begun to reflect it—but the market is still processing the company through the template that fit it five years ago.

Why Mispricings Happen

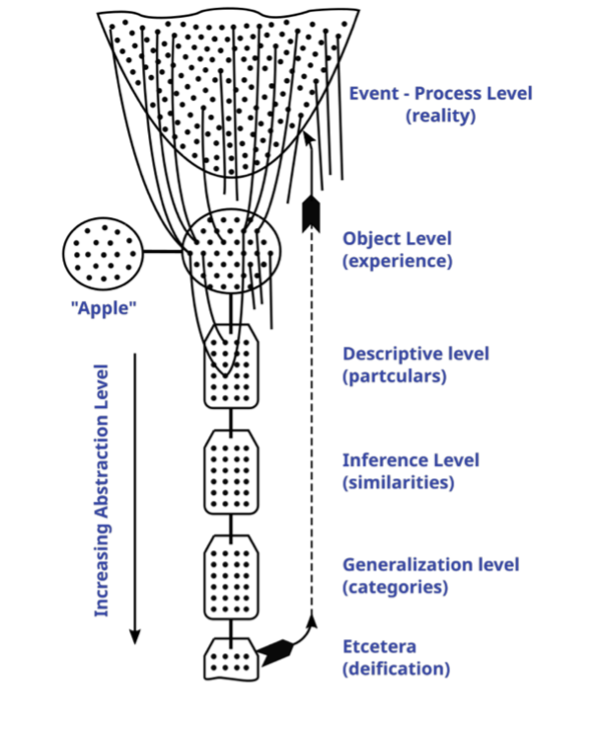

The phenomenon of persistent mispricings across public markets can be linked to the essential nature of the human brain and how we understand reality. We perceive reality through our senses, and we immediately attempt to categorize, name, and assign descriptors to it. The closer, more frequent, and more complete experience we have with an object, the more likely we are to comprehend it. Thomas Aquinas described this concept as the agreement of thought and thing, meaning we are right when the idea we have of something corresponds to the thing itself. A helpful visual for the way in which we come to know things comes from Alfred Korzybski, a philosopher in the realm of semantics. In 1925, he created a training device called the Structural Differential, a model and tool for understanding human knowledge:

As reality presents us with, say, an apple, we experience that reality through our senses and immediately abstract the experience to higher and higher levels of categories, applying tags or labels such as color, shape, form, species, flavor, and so on. Given this process of moving from the particular to the universal, the categories and values we assign to an object are more likely to be correct when we’ve had frequent complete views of, and encounters with, that object. Conversely the farther we are from an object, and the less exposure we have to it, the less likely we are to properly comprehend it. At its core (no apple pun intended), this is a concept everyone intuitively understands. When we tell two people, “Get to know each other”, we obviously don’t mean they should think about the other person, abstracting generalizations about each other from across the room. No, of course we mean they should spend time together, speak to each other, observe each other, and so forth. In short, knowledge is tied to experience.

This is all well and good, but what does it have to do with investing? The willingness to “get to know” a business determines the accuracy of our understanding of that business. Mispricings are really instances in which the market’s “thought” about a business does not match the “thing” itself, as investors attempt to categorize and understand something they have not taken the time to truly experience. A business undergoing a transformation, or whose thesis takes longer to play out than institutional capital is willing to wait, is like a speck on the desert horizon. That speck could be an oasis or a mirage. The heat haze obscures your vision. Ultimately, we don’t know what it is until we get close enough to see it clearly. But markets move fast. They see the speck of dust, and given incentive structures, timelines, and capacity for patience, categorize it. They’ve seen specks of dust like it before and apply that same thinking to this new spot on the horizon. By working to truly know the true nature of that spot on the horizon, by trudging along until we can get close enough to see it clearly, we are, on occasion, rewarded with an oasis—an investment opportunity that rewards our effort even though (or arguably precisely because) the market overlooked it.

Indeed, a willingness to pay close attention can yield surprisingly powerful results. Vincent Van Gogh was an almost obsessive observer of nature, spending much of his time outdoors. It might seem odd, then that his famous work "Starry Night" (shown below) is quite abstract. It doesn’t seem to be the work of someone who paid close attention to the details of the night sky.

In fact, critics initially deemed “Starry Night” too stylized, abstract, and unrealistic. However, it has since been commended by physicists and fluid dynamicists who found that it accurately depicts the mathematical theory of turbulence (the dynamism of energy through air in patterns that resemble eddies or waves) with near-perfect precision in at least fourteen different instances.

Coincidence? Perhaps. But Van Gogh’s willingness to stop and stare, to “get to know” his subject matter, may have helped him to create something almost miraculous. His painting may be quite abstract, but his abstractions are rooted in a deep, intimate understanding of his subject. "Starry Night” demonstrates the revelations that close attention to a subject matter can produce. At Crossroads, we take the time to immerse ourselves in the details of the companies we research, with the goal of being able to see things others can’t, like the swirls Van Gogh saw in an empty night sky.

To summarize, humans have a better chance of correctly understanding reality when they experience it directly and closely, instead of perceiving it through abstractions made at a distance. Fortunately for us, markets are constantly moving, with many investors glancing at events and announcements made by businesses and quickly assigning categories and values to them. These investors therefore often misunderstand or completely fail to recognize the true nature of these events. Mr. Market looks at reality from thirty thousand feet (or, if you prefer, a corner office on the fiftieth floor), so mispricings inevitably occur. Those who get as close as possible to the facts, and who can recognize patterns the abstracting machine has skipped over, are the ones best positioned to exploit value gaps before they close.

Our Edge

We believe our durable edge is thanks to the wealth of information we obtain through deep, close study of our companies and their industries. We try to get as close to events as possible, increasing the likelihood that we’ll understand the reality of the situation. As the spy novelist John le Carré said, “a desk is a dangerous place from which to view the world.”

That proximity is only half of our edge. The other half is the operating architecture described above, and the two halves are inseparable. Close study without behavioral discipline produces conviction at the wrong moments. Behavioral discipline without close study produces patience without a reason to act on it. The combination of deep, detailed work on a small number of businesses, and an operating structure that allows us to wait as long as the gap takes to close, is the edge we believe we possess.

In practice, that means three things. First, we calibrate the intensity of our search to the opportunity set rather than to the calendar. When public equities are richly priced and the obvious work has already been done by everyone else, we slow our equity position decision-making and broaden our aperture to adjacent corners of the capital structure and to special situations where size is not an advantage. We don’t feel the need to fill our portfolio for the sake of filling it, and our partners should not expect us to. Second, we route our analytical restlessness into channels that do not contaminate the core book. The personal-account special situations, the deep dives into industries we do not yet have positions in, the eclectic reading habits that run across disciplines are not hobbies but sandboxes we can play in while sitting still on the names that matter. Third, we have built an internal process in which ideas are stress-tested adversarially before they become positions. Once an analyst has invested time in a thesis, his natural tendency is to find reasons why it’s right. That’s why we construct an environment in which the reasons it might be wrong are surfaced by someone whose job in that conversation is specifically to look for them.

Of course, we still get things wrong. But with a willingness to go one step further than the herd, the patience to wait for a gap to close on a timeline dictated by the business itself (and not by the calendar), and an operating structure that converts intellectual energy into discipline rather than into trades, we believe we can continue to find great businesses at attractive prices. That is the work. That is what we are paid for.